Energy

The Oil Futures Market: Prices Are High Because Nobody Wants to Play

Published:

Last Updated:

Gasoline prices in the United States have risen nearly six cents a gallon in the past month, and the spot price for a barrel of West Texas Intermediate (WTI) crude oil has risen from $97.63 at the end of December to $99.47 now, after a brief sojourn last week above $100 a barrel. We noted Monday morning that gasoline prices remain above $3 a gallon in every state, with a national average of $3.34 a gallon, and we note some of the temporal reasons for the higher prices. Source: Thinkstock

Source: Thinkstock

Pump prices are not likely to fall much in the next few months as refineries enter the turnaround period when they stop producing cheaper winter gasoline and begin making more expensive summer fuel.

There may be a more fundamental change also keeping crude oil prices high at a time when U.S. production is at its highest level in more than a dozen years: the futures market is being abandoned by non-commercial (i.e., speculative) participants. Even commercial participants are looking to get out of the trading business. Occidental Petroleum Corp. (NYSE: OXY) has said that it will “reduce” its proprietary trading business and Hess Corp. (NYSE: HES) is trying to sell its Hetco trading operation.

As these market participants leave the market, fewer buyers remain, which lowers the futures price that producers can get as a hedge for future production. The result is an increase in price spreads between current cash spot prices and futures prices — cash prices rise and futures prices fall. That leads to a market condition called backwardation.

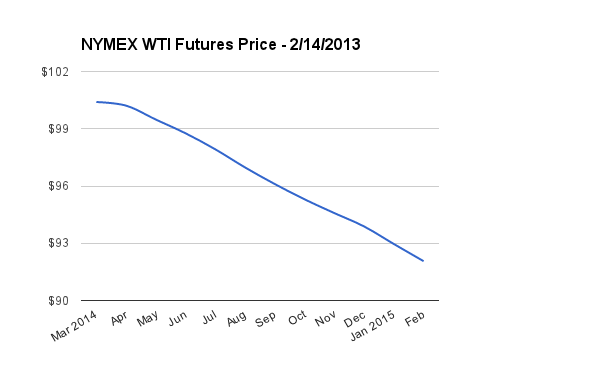

The following chart shows the difference between the current WTI price per barrel and the price 12 months out.

As more players exit the futures market, there are fewer buyers willing to take the long side of the bet on future crude prices. The result could well be lower inventories, a result already noted by the International Energy Agency (IEA) in its most recent report:

At the end of December [global] commercial inventories stood at 2,559 million barrels, their lowest absolute level since 2008. Moreover, the stock deficit to five-year average levels widened slightly to 103 million barrels, the first time the 100 million barrel level has been exceeded since mid-2004.

There is evidence that as backwardation increases, stockpiles decrease. Crude prices remain high and so do refined product prices. Energy economist Philip Verleger notes in his latest weekly newsletter:

Looking to the future, we see no reason for commercial inventories to increase. The market offers no incentive at the moment to build stocks. To the contrary, it is imposing growing punishments on those who hold oil. For this reason, we agree with the IEA that the glut will be more and more elusive.

In other words, prices will remain high and probably rise even higher as commercial inventories are drawn down. It looks like summer driving is going to be expensive.

Are you ready for retirement? Planning for retirement can be overwhelming, that’s why it could be a good idea to speak to a fiduciary financial advisor about your goals today.

Start by taking this retirement quiz right here from SmartAsset that will match you with up to 3 financial advisors that serve your area and beyond in 5 minutes. Smart Asset is now matching over 50,000 people a month.

Click here now to get started.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.