Banking, finance, and taxes

The World Is $199 Trillion in Debt, and Growing

Published:

Last Updated:

The world’s economies may have improved since the financial crisis, but now more than ever, the world is drowning in higher and higher debt. A new report from the McKinsey Global Institute suggests that the world has added a whopping $57 trillion in debt since the financial crisis. The firm pointed out that all major economies currently have higher levels of borrowing relative to gross domestic product (GDP) versus the year 2007, right before the Great Recession and financial crisis. The net global debt added since then is now projected as a ratio of debt to GDP to be up 17 percentage points. Source: Thinkstock

Source: Thinkstock

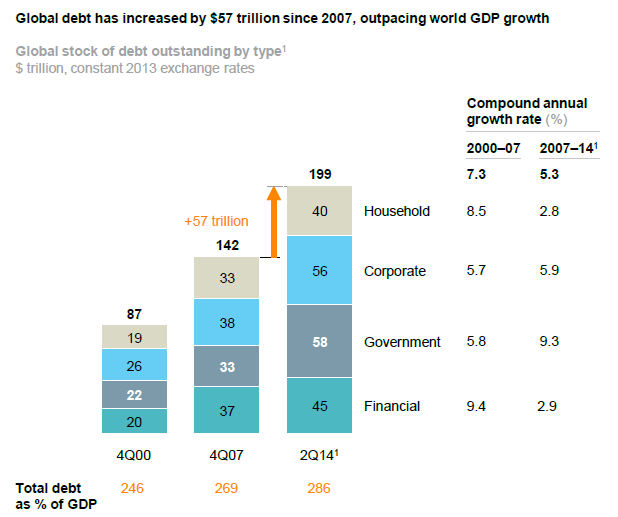

The new total of global debt, as of the end of the second quarter of 2014, is a whopping $199 trillion. This massive number compares to $142 trillion at the end of 2007, and it compares to a mere $87 trillion at the end of 2000 (see first image below).

McKinsey’s report highlighted three areas of emerging risk that all of this new debt poses. First is the rise of government debt, and second is the continued rise in household debt — and housing prices — to new peaks in Northern Europe and some Asian countries. Third is the quadrupling of China’s debt.

Before you think that this ballooning debt applies only to governments, it does not. This also applies to households, corporations and financial-related debt.

ALSO READ: U.S. Pension Assets Added 9% in 2014

McKinsey further warns that global household debt is reaching new peaks. It was only in nations like the United States, the United Kingdom, Ireland and Spain where households have actually deleveraged since the financial crisis. The total household debt in other nations, including the household debt-to-income ratios, have continued to rise. These nations with higher debt were said to include nations such as Australia, Canada, Denmark, Sweden, the Netherlands, Malaysia, South Korea and Thailand.

As the first image below shows, government debt has grown by $25 trillion in seven years. The research warns:

It (debt) will continue to rise in many countries, given current economic fundamentals. Some of this debt, incurred with the encouragement of world leaders to finance bailouts and stimulus programs, stems from the crisis. Debt also rose as a result of the recession and the weak recovery. For six of the most highly indebted countries, starting the process of deleveraging would require implausibly large increases in real-GDP growth or extremely deep fiscal adjustments. To reduce government debt, countries may need to consider new approaches, such as more extensive asset sales, one-time taxes on wealth, and more efficient debt-restructuring programs.

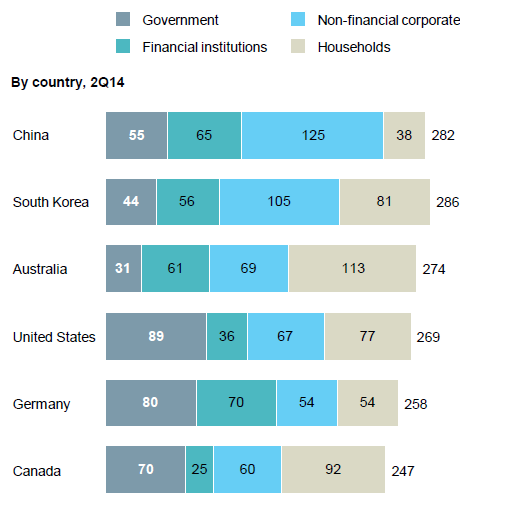

Globally, the scariest figure by far has to be that China’s debt has quadrupled since 2007. This was driven by real estate and shadow banking, up to 282% of GDP. If you want to put this in perspective, this figure is larger than the United States or Germany.

McKinsey’s three warnings on China are as follows: half of all loans are somehow linked to China’s overheated real-estate market; unregulated shadow banking accounts for nearly half of new lending; and the debt of many local governments is probably unsustainable. The only good news is that China’s government is believed to have the capacity to bail out the financial sector if a property-related debt crisis develops.

A second image highlights just how much this is in terms of total debt to GDP for some of the major nations, but that debt includes government, financial institutions, corporate (non-financial) and households.

ALSO READ: U.S. Companies Cutting the Most Jobs

Anyhow, arguments of this sort can carry on forever. It is ultimately hard to know how the unwinding of all this debt will occur. Four paths to begin government debt deleveraging were identified as follows: make fiscal adjustments to reduce or eliminate fiscal deficits, accelerate GDP growth through productivity improvements, raise inflation targets or restructure debt.

If the global debt load is still growing, and if the $199 trillion debt was as of the second quarter of 2014, then the global debt load by now is really over $200 trillion. Food for thought.

UPDATE: To put this in context, that total debt, based upon a global population of close to 7.2 billion people, would come to $27,777 per person. The World Bank’s 2014 estimate was based upon 2011 data, showing that some 17% of people in the developing world, some 1.2 billion people, lived at or below $1.25 a day.

Want retirement to come a few years earlier than you’d planned? Or are you ready to retire now, but want an extra set of eyes on your finances?

Now you can speak with up to 3 financial experts in your area for FREE. By simply clicking here you can begin to match with financial professionals who can help you build your plan to retire early. And the best part? The first conversation with them is free.

Click here to match with up to 3 financial pros who would be excited to help you make financial decisions.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.