Keryx Biopharmaceuticals Inc. (NASDAQ: KERX) has not been a household name in biotech investing, but the move on news on Monday has put the company on the map. After shares are up almost 95% at $6.70, this company still has a market capitalization rate that is about $480 million. This is on a company which many investors have written off on more than one occasion. With a history of more than 10 years as a stock this used to be $10 and higher on multiple occasions.

Keryx Biopharmaceuticals Inc. (NASDAQ: KERX) has not been a household name in biotech investing, but the move on news on Monday has put the company on the map. After shares are up almost 95% at $6.70, this company still has a market capitalization rate that is about $480 million. This is on a company which many investors have written off on more than one occasion. With a history of more than 10 years as a stock this used to be $10 and higher on multiple occasions.

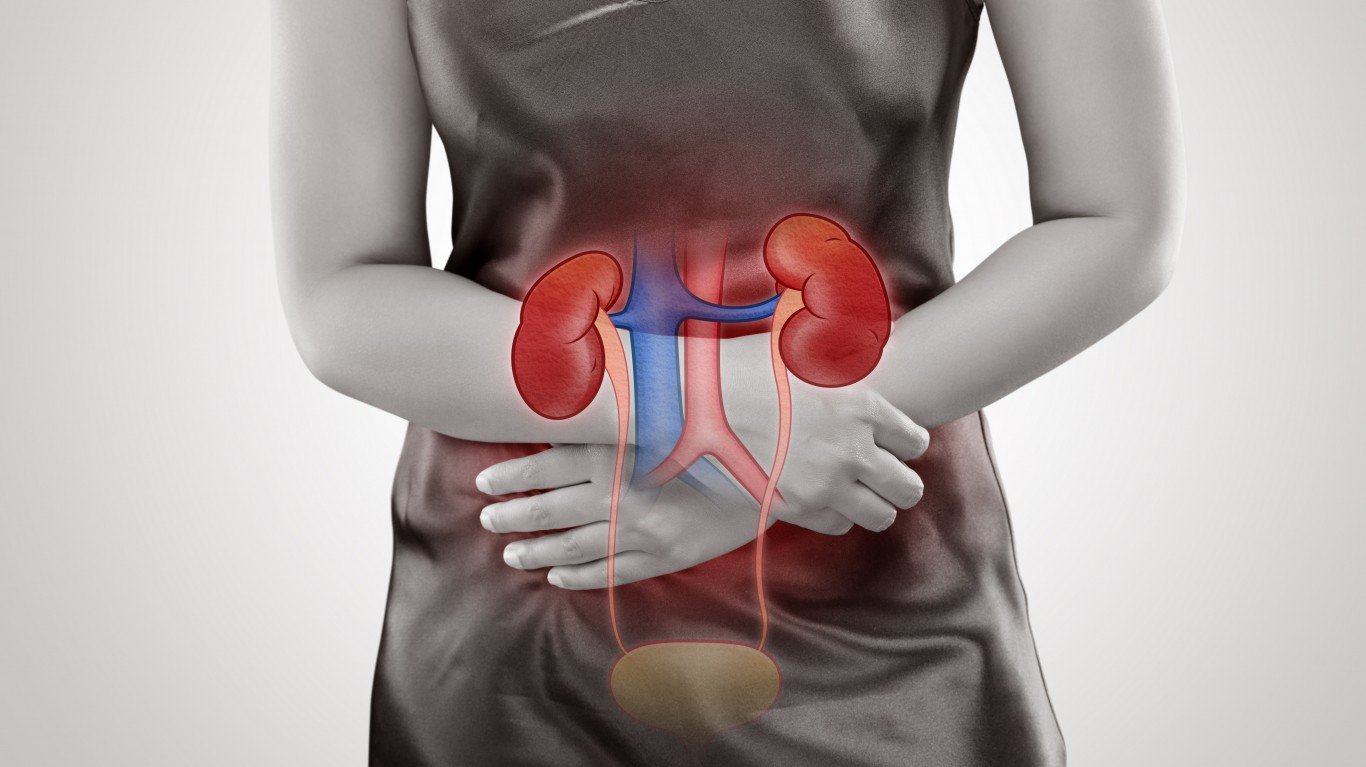

Investors have been waiting for some time on the Phase III study results of its phosphate binder Zerenex when used with positive top-line data in kidney dialysis patients. Keryx has had a serious regulatory risk and commercialization risk based on this having been a long process. Keryx has yet to generate any significant revenues to date. The company believes that Zerenex has the potential to become the market leader in the phosphate binder space, which was said to be a $2.4 billion market opportunity. Zerenex met a highly statistical significant change in serum phosphorus versus the placebo among end-stage renal disease patients on dialysis. The treatment is for hyperphosphatemia as a condition in patients with chronic kidney disease who need help flushing dangerously high levels of phosphorus.

Keryx also showed that a secondary endpoint data showed a reduced need for iron and erythropoiesis-stimulating agents. With shares ar $6.70, the prior 52-week range was $1.28 to $5.19. What is more impressive than anything is that today’s move is well above the $5.03 open and $3.43 close from the prior day, and it is on some 45 million shares versus an average daily volume of only 1.4 million shares.

Contact [email protected] for any questions or corrections.