Retirees face a portfolio puzzle: how to generate returns without losing sleep during market turbulence. The challenge intensifies when managing multiple funds, rebalancing between stocks and bonds, and maintaining discipline through volatility. The iShares Core 60/40 Balanced Allocation ETF (NYSE:AOR) packages an entire balanced portfolio into a single ticker.

A Complete Portfolio in One Trade

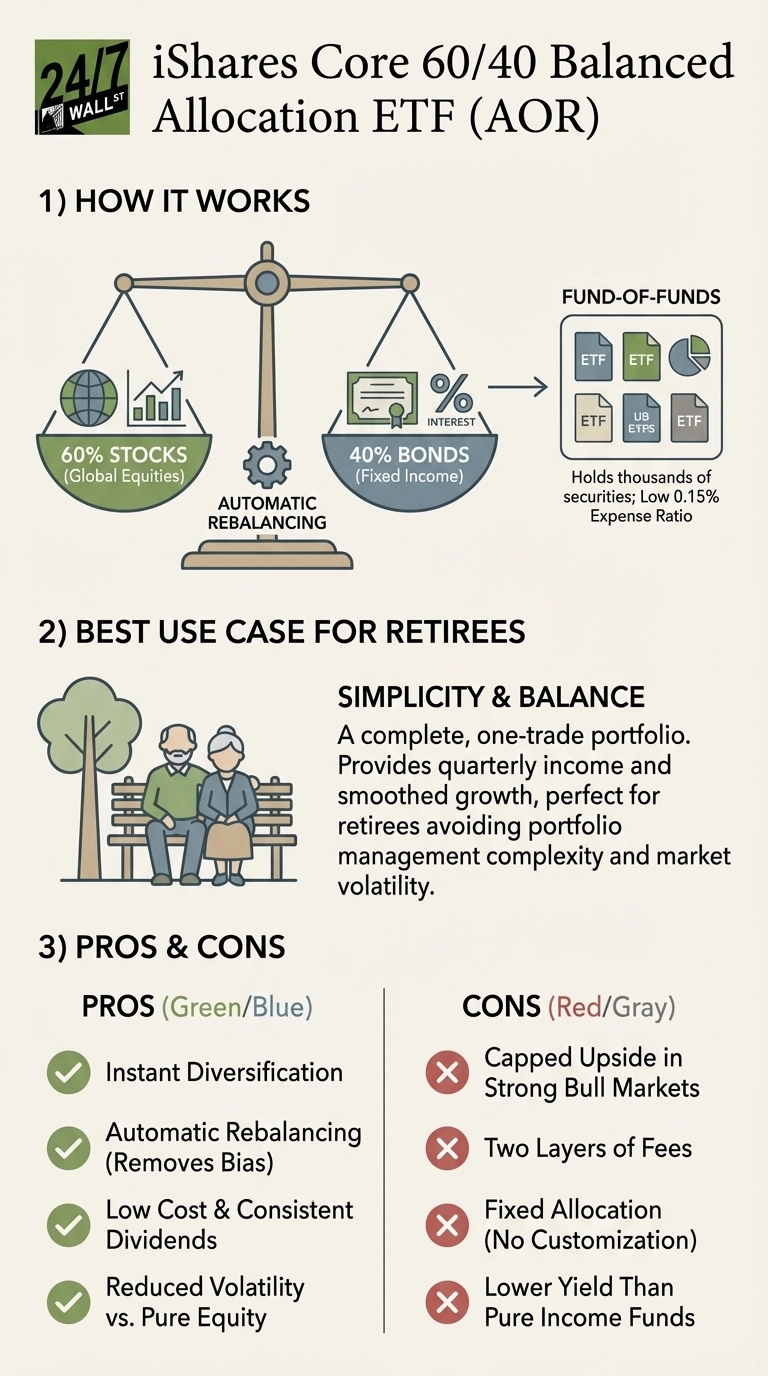

AOR operates as a fund-of-funds, holding other iShares ETFs to maintain a 60% equity and 40% fixed income allocation. This delivers instant diversification across thousands of securities spanning U.S. stocks, international equities, and investment-grade bonds. The fund automatically rebalances to maintain its target allocation, eliminating the behavioral challenge of selling winners and buying losers during market extremes.

With a 0.15% expense ratio and 5% annual portfolio turnover, AOR keeps costs low while minimizing taxable events. The fund has distributed dividends consistently since its 2008 inception, currently yielding approximately 2.5%. For retirees seeking quarterly income without managing multiple positions, this simplicity matters.

Performance Through Market Cycles

AOR returned approximately 14% in 2025 through mid-December, matching the S&P 500’s performance despite holding 40% in bonds. Over the past decade, AOR generated roughly 8% annualized returns, capturing meaningful equity upside while the bond allocation dampened volatility.

The 2022 bear market tested the 60/40 strategy when both stocks and bonds declined simultaneously. While AOR experienced drawdowns, its diversified structure limited losses compared to pure equity portfolios. The subsequent recovery demonstrates how balanced allocations can smooth the retirement journey without abandoning growth.

The Tradeoffs Retirees Accept

AOR’s balanced approach comes with predictable compromises. The 40% bond allocation caps upside potential during strong bull markets. Investors who held pure equity funds captured significantly more gains during 2023-2024’s rally. The fund-of-funds structure simplifies portfolio management, but investors pay two layers of fees: AOR’s 0.15% expense ratio plus the underlying ETF costs. Retirees cannot customize the 60/40 split based on personal risk tolerance or market conditions.

Who Should Avoid AOR

Investors with 20+ years until retirement should skip AOR. The 40% bond allocation unnecessarily limits growth potential for those with decades to ride out market volatility. Retirees who need higher current income will find AOR’s 2.5% yield insufficient. Those seeking 4-5% annual distributions should consider higher-yielding alternatives or bond-heavy allocations.

Consider AOK for More Conservative Exposure

The iShares Core Conservative Allocation ETF (NYSE:AOK) flips the script with a 30% equity and 70% bond allocation. This more defensive posture suits retirees in their late 70s or those with shorter time horizons. AOK’s higher bond weighting delivers a 3.3% dividend yield, nearly a full percentage point above AOR, while reducing equity exposure. The tradeoff: AOK’s long-term returns lag AOR’s by approximately 2-3 percentage points annually due to lower stock allocation.

For investors questioning whether 60% stocks feels too aggressive five years into retirement, AOK provides a logical step-down without abandoning equities. Both funds share the same 0.15% expense ratio and fund-of-funds structure, making the choice purely about risk tolerance rather than cost efficiency. AOK’s 3.3% yield compares favorably to AOR’s 2.5% for those prioritizing income.

AOR works best for newly retired investors seeking simplicity and balance, but its fixed 60/40 allocation means accepting both capped upside and moderate income generation.

Contact [email protected] for any questions or corrections.