Most people believe Social Security benefits are untouchable. While creditors can’t generally garnish these payments, federal law creates important exceptions that can reduce monthly checks for millions of retirees.

Understanding which debts can reach your benefits matters because Social Security often represents the majority of retirement income. For someone relying on $2,000 monthly, losing even $300 can mean choosing between prescriptions and groceries.

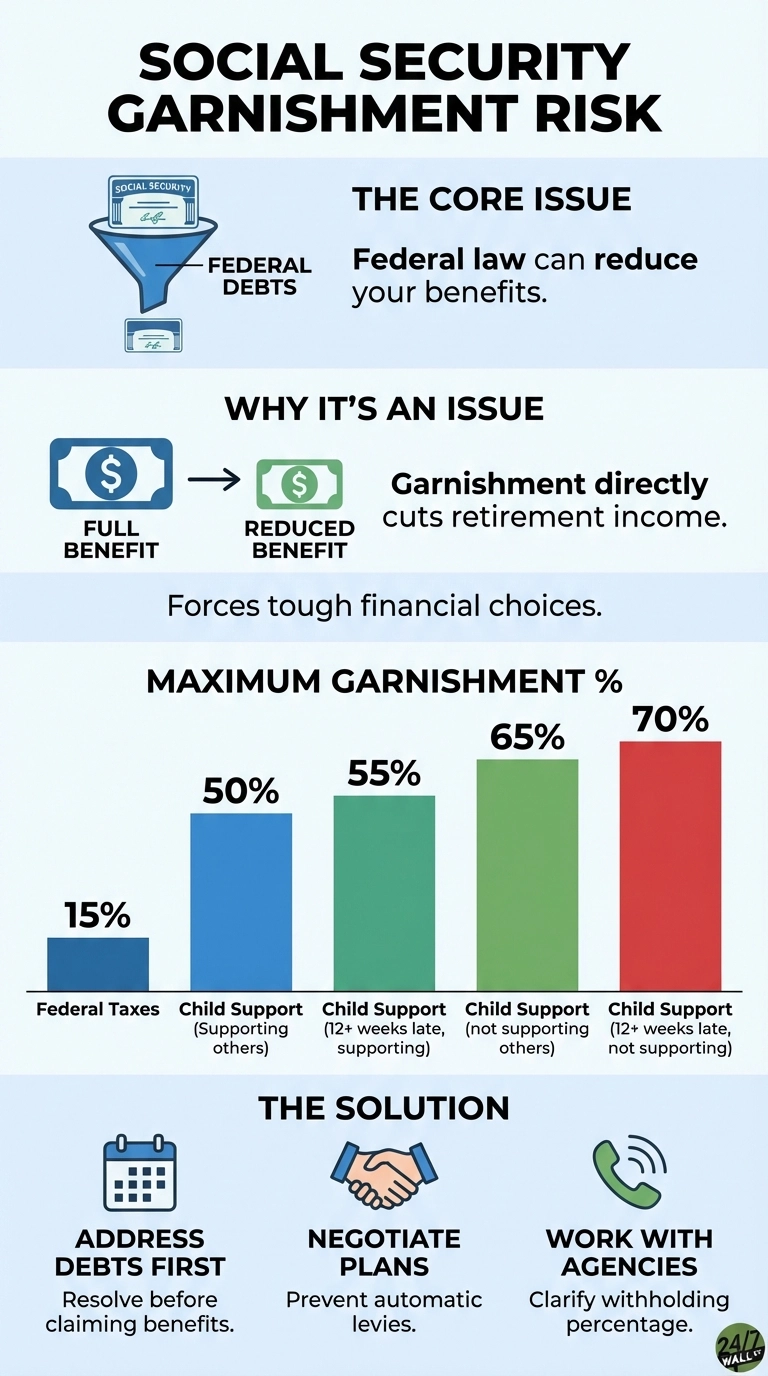

The Federal Debts That Override Protection

Four types of obligations allow the federal government to withhold Social Security benefits directly. Unpaid federal taxes top the list. Under the Taxpayer Relief Act of 1997, the IRS can levy up to 15% of each monthly payment through the Treasury Offset Program until the tax debt is satisfied.

Child support and alimony obligations carry the broadest garnishment authority of any federal debt. The law recognizes these as priority obligations because they support dependents who rely on that income. The garnishment structure reflects a careful balance between protecting your current household and ensuring support reaches those who depend on it. When payments fall significantly behind schedule, enforcement intensifies to protect children or former spouses who have gone without support for months.

The specific percentages vary based on your situation. If you’re supporting other dependents, withholding is capped at a lower rate to preserve income for your current family. Without competing obligations, more of your benefit can be redirected because no other dependents need protection.

Federal student loans in default and other debts owed to federal agencies round out the list. The Treasury Offset Program coordinates these collections across government entities, automatically deducting amounts before benefits reach your account.

How This Changes Your Retirement Math

The timing matters more than many retirees expect. A tax levy doesn’t take a flat dollar amount—it takes a percentage of whatever you receive. This means the decision about when to claim becomes intertwined with your debt situation. Someone who delays claiming to increase their benefit will see a larger absolute amount garnished, even though the percentage stays the same. The annual impact compounds over time, turning what seemed like a straightforward claiming decision into a complex calculation about debt resolution timing.

Delaying benefits past full retirement age normally provides a powerful advantage through increased monthly payments. But garnishment changes this calculation fundamentally. The percentage-based levy means your increased benefit gets partially redirected before it reaches you. This doesn’t eliminate the advantage of waiting, but it does reduce the effective gain you’ll actually receive in your account each month.

For those with other income sources like pensions or retirement account withdrawals, the interaction becomes more complex. Social Security benefits may become taxable once combined income exceeds certain thresholds, and garnishment happens before you receive the money.

What to Consider Before Benefits Begin

The hardest mistake to undo is claiming benefits without addressing federal debts first. Once garnishment begins, it continues until the obligation is satisfied. Setting up a payment plan with the IRS before claiming can sometimes prevent automatic levies.

For child support or alimony, state agencies handle enforcement, but federal law sets the limits. Working directly with the agency before retirement can clarify exactly what percentage will be withheld and whether negotiation is possible.

Individual circumstances vary widely, and small details in your situation can significantly change outcomes. The goal is understanding which decisions carry lasting financial consequences you can’t easily reverse.

Contact [email protected] for any questions or corrections.