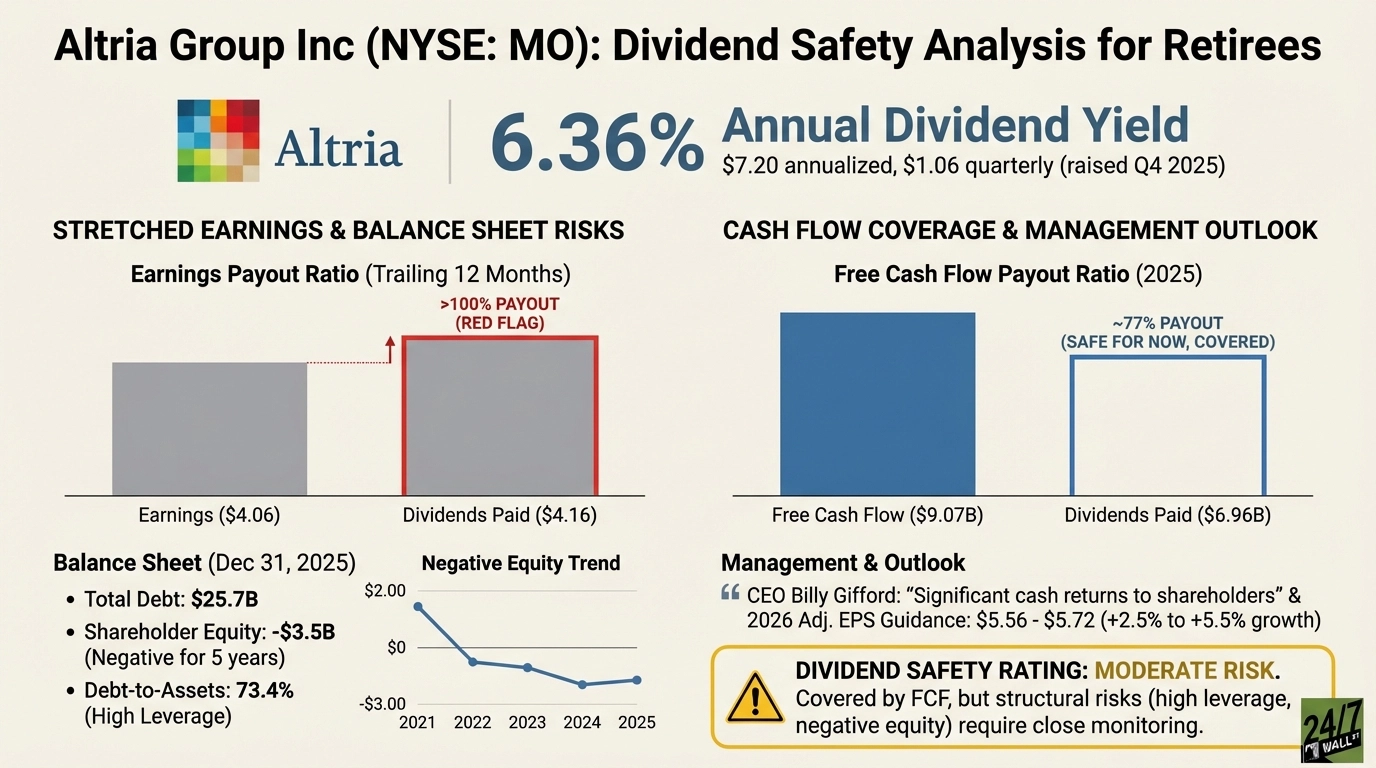

Altria Group Inc (NYSE:MO | MO Price Prediction) is the company behind Marlboro cigarettes and smokeless tobacco products. It delivers one of Wall Street’s highest dividend yields at 6.36%. For retirees hunting income, that yield is hard to ignore. The question is whether it’s built on solid foundation or borrowed time.

The company pays $1.06 per share quarterly, annualizing to $7.20. Altria has raised its dividend for over two decades without a cut. The most recent increase came in Q4 2025, when the quarterly payment jumped from $1.02 to $1.06—a 3.9% quarter-over-quarter increase.

The Payout Is Stretched Beyond Earnings

Altria’s earnings payout ratio sits above 100%. The company earned $4.06 per share over the trailing twelve months but paid out $4.16 in dividends. The dividend exceeds reported earnings – a classic red flag for income investors.

But cash flow tells a different story. In 2025, Altria generated $9.07 billion in free cash flow and paid $6.96 billion in dividends. That’s a free cash flow payout ratio of roughly 77%, leaving breathing room. Over the past five years, coverage has ranged from 1.22x to 1.34x, comfortably above the danger zone.

A Balance Sheet That Raises Eyebrows

Altria’s balance sheet is where the picture darkens. The company carries $25.7 billion in total debt and has negative shareholder equity of -$3.5 billion as of December 31, 2025. That negative equity position has persisted for five consecutive years, driven by aggressive share buybacks and declining asset values. The debt-to-assets ratio stands at 73.4%, and current liabilities exceed current assets.

Cash on hand is $4.48 billion, up from $3.13 billion a year ago. That provides a cushion, but the structural leverage is real.

What Management Says

CEO Billy Gifford has emphasized “significant cash returns to shareholders” and reaffirmed guidance for 2026 adjusted EPS of $5.56 to $5.72, representing 2.5% to 5.5% growth. The company also expanded its share buyback program to $2 billion. That commitment is reassuring, but it doesn’t erase the leverage or earnings pressure.

Safe for Now, but Watch the Cracks

Dividend Safety Rating: Moderate Risk

The dividend is covered by free cash flow, and management remains committed. But the payout ratio exceeding earnings, negative equity, and declining core business volumes create structural risk. Altria works for income if you’re willing to monitor quarterly results closely and accept minimal growth. But if you need absolute certainty, this isn’t it.

Contact [email protected] for any questions or corrections.