Micron Technology (NASDAQ:MU | MU Price Prediction) shares retreated as much as 5% in early Wednesday trading, extending a brutal week that had already seen the stock fall 14% from its recent highs. The immediate catalyst is fiscal Q2 2026 earnings that, while strong on the surface, contained two specific elements rattling investors.

The headline numbers were fine. What spooked the market was a large debt repurchase tender offer and a meaningful step-up in Micron’s capital expenditure guidance. The debt tender raises questions about financial maneuvering, while higher capex puts near-term profitability under pressure even as long-term demand appears solid.

A High Bar That Got Even Higher

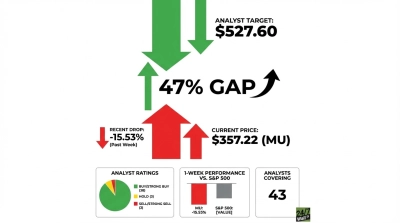

Coming into this report, Micron Technology had set an extraordinary target. Q2 FY2026 guidance called for revenue of $18.70 billion, non-GAAP EPS of $8.42, and a GAAP gross margin of 67%. That guidance followed a Q1 that already shattered records, with revenue of $13.64 billion, up 57% year over year, and non-GAAP EPS of $4.78 against estimates of $3.94.

Micron Technology CEO Sanjay Mehrotra had framed the Q2 outlook in sweeping terms, stating, “Our Q2 outlook reflects substantial records across revenue, gross margin, EPS and free cash flow, and we anticipate our business performance to continue strengthening through fiscal 2026.” When management sets a bar that high, even strong execution leaves investors asking what comes next.

The capex trajectory is the core tension. Micron’s capital expenditures reached $5.39 billion in Q1 FY2026 alone, up 68% year over year. Spending at that pace is a bet on sustained AI-driven memory demand. If that demand softens even slightly, the math gets uncomfortable; that’s exactly what the market is now stress-testing.

TurboQuant Adds a Structural Question

The sell-off is complicated by a paper published yesterday by Google Research, a division of Alphabet (NASDAQ:GOOGL). The paper introduces TurboQuant, a compression algorithm that achieves at least a 6x reduction in KV cache memory size in large language models with zero loss in model accuracy. The KV cache is the high-speed digital storage system AI models use to hold frequently accessed information during inference.

4-bit TurboQuant also achieves up to an 8x performance increase over 32-bit unquantized keys on NVIDIA‘s (NASDAQ:NVDA) H100 GPUs. If AI models can do more with less memory, long-term demand for high-bandwidth memory and DRAM faces a genuine structural question. Sophisticated investors are now debating whether this represents a real ceiling on memory demand growth or one technique among many that will be absorbed by ever-larger models.

The bull case for MU stock remains intact in the near term. Analysts were calling for Micron to keep running as recently as March 13, citing the AI memory supercycle. The analyst consensus price target sits near $515, with 38 buy ratings against just 2 sells. That gap between analyst consensus and where the stock trades today reflects a debate about timing and risk, not about whether Micron is a real business.

Community Debate Heats Up

On Reddit’s r/stocks, the reaction has been sharp and divided. One widely circulated post expressed the valuation case bluntly: “Micron Now Trading for 24X Next Quarter’s Earnings While Growing Earnings by 900%.”

The bulls see a deeply discounted entry. However, the bears are pointing to geopolitical headwinds, the capex burden, and TurboQuant as reasons to stay cautious.

At the same time, a small but vocal segment is floating deliberate market manipulation as an explanation for MU stock’s price movement. I didn’t find concrete evidence to support this claim, though.

Memory Suppliers Under the Microscope

The pressure on MU stock is rippling through the broader memory equipment ecosystem. Four major suppliers are trading lower today, though each is down modestly.

- Lam Research (NASDAQ:LRCX), a leading supplier of wafer fabrication equipment used in memory chip production, is off about 3% today, the steepest decline among the group given its heavy exposure to memory etch and deposition spending.

- Applied Materials (NASDAQ:AMAT), which provides materials engineering solutions critical to memory chip manufacturing, is down about 1%, a modest move reflecting its more diversified customer base across logic and foundry.

- Camtek (NASDAQ:CAMT), which supplies inspection and metrology equipment for advanced memory production, is off about 2%, with its concentrated memory exposure making it more sensitive to any slowdown in HBM production ramps.

- Onto Innovation (NYSE:ONTO), which provides process control and inspection solutions for semiconductor and memory manufacturing, is down about 1%, though its HBM volume purchase agreement exposure keeps it closely tied to Micron’s capex trajectory.

None of these moves are catastrophic on their own. Yet, if the TurboQuant narrative gains traction and AI developers genuinely begin reducing memory footprints, the equipment suppliers that built their growth stories on an uninterrupted memory capex cycle will face the same questions Micron is facing today.

Micron Stock Pullback in Perspective

Micron’s fundamentals aren’t broken, by any means. The company’s cloud memory business nearly doubled year over year, generating $5.28 billion in revenue at a 66% gross margin.

What the market is repricing today is the risk that the path forward gets bumpier than guidance implied. Whether TurboQuant proves to be a genuine structural shift or just another efficiency tool absorbed by growing AI workloads will likely determine whether this week’s Micron stock pullback looks like an opportunity or an early warning.

Contact [email protected] for any questions or corrections.