I keep hitting the buy button on Alphabet (NASDAQ:GOOGL | GOOGL Price Prediction), and June’s volatility has only sharpened the urge. Every time the market panics that the Fed will hold rates higher for longer to fight creeping inflation, cyclical tech gets dragged down with it, and one of the cleanest compounders I own goes on sale. Macro-driven index liquidations have historically been the right backdrop to accumulate world-class monopolies, and Alphabet’s enterprise moat is insulated from central bank posturing. So I keep loading.

The thesis I cannot let go of: Google owns the digital plumbing enterprises cannot stop spending on, and AI is accelerating that dependence rather than breaking it. The bears spent a year warning that generative AI would gut Search. Then Search & other revenue grew 19% year over year to $60.40 billion in Q1 FY2026, with queries at an all-time high. The cannibalization story died on the income statement.

Three Reasons the Conviction Keeps Compounding

First, Google Cloud is the re-rating engine almost nobody is pricing correctly. Cloud revenue hit $20.03 billion, up 63% year over year, with backlog nearly doubling quarter over quarter to over $460 billion. Inside that, enterprise AI solutions became the primary growth driver for Cloud for the first time, revenue from products built on GenAI models grew nearly 800% year over year, and Gemini Enterprise paid monthly active users grew 40% quarter over quarter. Cloud operating margin expanded from 17.8% to 32.9% in a single year. That is what operating leverage on a moat looks like.

Second, the cash machine economics are absurd in the best way. Q1 delivered $109.90 billion in revenue, EPS of $5.11 versus a $2.63 consensus, and operating margin of 36.1%. Across the trailing twelve months, the business produced a 35.70% return on equity, 29.60% return on invested capital, and a 32.05% operating margin. A P/E near 16 with a 6.27% earnings yield is utility-grade pricing for a business minting these returns.

Third, the balance sheet lets management spend like a hyperscaler without breaking the dividend. Net debt to EBITDA sits at 0.19, debt-to-equity at 0.143, and interest coverage at 903.26. Management still raised the dividend 5% to $0.22 per share, payable June 15, 2026. The Gemini app crossed 350 million paid subscriptions. The compounding pieces are working.

The Risk I Am Not Hand-Waving Away

Capex is the honest risk. Capital expenditures more than doubled to $35.67 billion in Q1, and free cash flow fell 46.63% year over year to $10.12 billion. 2026 capex guidance now sits at $180 billion to $190 billion, with 2027 expected to step up further. If those dollars do not earn their cost of capital, the thesis cracks. What keeps me buying anyway is that Sundar Pichai said the company is “compute constrained in the near term” and that “Cloud revenue would have been higher if we were able to meet the demand”. Demand is outrunning what Google can supply.

What Keeps the Buy Button Active

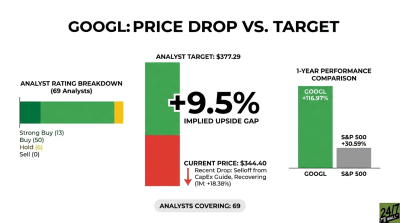

The stock is down 10.61% over the past month to $359.68 while the underlying business is running its 11th consecutive quarter of double-digit revenue growth. I will take that trade every June the market hands me.