Former St. Louis Fed President Jim Bullard, now Dean of the Mitch Daniels School of Business at Purdue University, believes the Federal Reserve is likely to resume tightening later this year despite a likely pause in July. During a July 6, 2026 appearance on CNBC’s Squawk Box, Bullard argued that inflation remains too high to ignore and said the September meeting could emerge as the next realistic opportunity for a rate hike, while expressing skepticism that artificial intelligence-driven productivity gains will arrive quickly enough to change the Fed’s near-term trajectory.

Bullard Says Inflation Is Still Too High for the Fed to Ignore

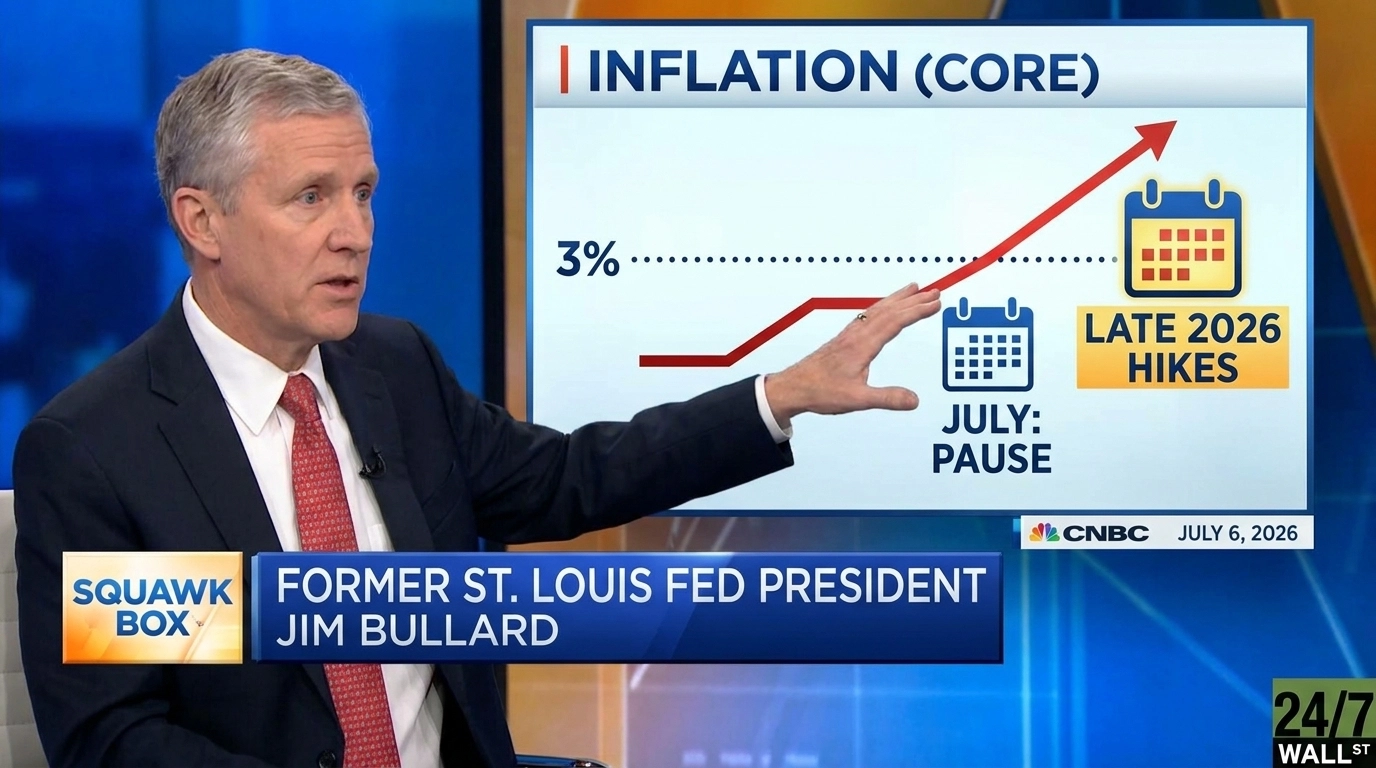

Bullard’s framing centers on one uncomfortable number. “Core inflation is too high. It’s up 6/10 from where it was over 3%. Well over 3% now. The Committee doesn’t like that. The 3% is a red line,” he told CNBC. That characterization matters because the Fed’s official target remains 2%, and a core reading drifting further above 3% puts credibility on the line.

Bullard did offer two disinflationary offsets. He noted that the bond market is signaling peak inflation has passed, and he pointed to recent oil price declines that are expected to feed through into inflation data in the coming weeks and months. Those forces could buy the Committee time. However, he believes they are unlikely to substitute for policy action.

Why September Looks Like the Fed’s Next Big Decision

On timing, Bullard was direct. “I think it’s a little soon in July here, but you could tee up September,” he said. He also characterized the June meeting as “pretty hawkish,” suggesting the Committee has already begun laying the groundwork for a move.

Bullard’s comments suggest investors should view July as a meeting where the Fed prepares markets rather than changes policy. Whether September ultimately brings another rate hike will likely depend on whether upcoming inflation reports show enough improvement to convince policymakers that price pressures are moving back toward their 2% target.

Additionally, Bullard doesn’t think the Fed will stop at just one rate hike. “A lot of people are talking about one rate increase. The Committee does not generally do that,” he said, noting that the Committee historically does not deliver single rate increases when tightening is warranted.

Bullard Isn’t Buying AI As an Inflation Cure, Yet.

Chairman Warsh has publicly leaned on the idea that artificial intelligence could boost productivity and ease inflationary pressure without aggressive rate hikes. Bullard is still skeptical about the timeline, though. “Productivity is hard to measure. It’s great technology. It will diffuse through the whole economy. But that’ll take time. You got to get it through all these business cultures that have grown up over a long period of time,” he said.

If AI-driven productivity gains take years rather than quarters to show up in the data, the Fed cannot rely on them to close the gap between 3%-plus core inflation and its 2% target. Policy has to do the work in the near term.

What to Watch Next

Bullard’s outlook is based on his belief that inflation remains too high for the Fed to simply hold rates flat indefinitely. While falling oil prices and improving inflation expectations could justify patience in July, he believes those factors are unlikely to eliminate the need for additional tightening if core inflation remains above 3%. For investors, that means expectations of a quick return to easier monetary policy could prove premature if inflation data fails to improve meaningfully over the next several months.

Contact [email protected] for any questions or corrections.