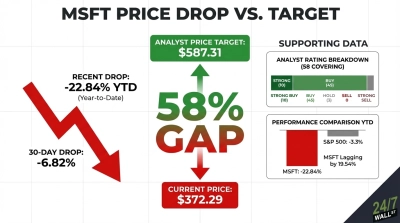

[cnxvideo id=”649847″ placement=”ros”]Microsoft Corp. (NASDAQ: MSFT) generated a total return of 15% in 2016, and it ended the year at $62.14 a share. Over half of those gains were from the fourth quarter alone, but that is generally a good calendar time for technology stocks. It should be noted that the Dow Jones Industrial Average rose 13.4%, the S&P 500 was up 9.5% and the Nasdaq rose just 7.5% in 2016. Perhaps even more notable than outperforming the three major indexes was that Microsoft managed to make its old all-time high share prices from the 1999 to 2000 tech bubble days.

Microsoft had a consensus analyst target price of $65.36 at the start of 2017. That implied simple upside projections of 4.4%, but the 2.5% dividend yield would suggest a total return opportunity of about 6.9% in 2017, if the analysts manage to get it right this year. The analysts were wrong in 2016 as they called for just over 5% in total return in Microsoft shares at the start of 2016, but that was after more than 22% gains in 2015.

24/7 Wall St. has been evaluating all of the 30 Dow stocks for a bullish-bearish analysis to see what lies ahead in 2017. Microsoft’s outlook for 2017, at least as of the start of the year, looked more positive than negative.

What is so amazing, even with the shift to the cloud and a mobile-first effort from Satya Nadella as chief executive, is that many analysts have remained behind the curve on Microsoft. Maybe they thought that Apple’s rise and the overly hyped death of the personal computer were going to make Microsoft obsolete. Regardless, it almost feels as though many of the analysts on Wall Street seem to resent the Microsoft gains that have been made.

[nativounit]

Goldman Sachs finally lost its caution in November when it upgraded Microsoft shares to Buy from Neutral and issued a new above-consensus $68 price target. Also in November, Atlantic Equities raised its Underweight (“Sell” at most firms) to Neutral.

At the start of 2017, Merrill Lynch maintained its Buy rating and raised its price objective to $75 from $68. The firm sees Microsoft being a beneficiary of multiple secular themes in software, including artificial intelligence, digitization and bi-modal IT, and they even noted that the cloud transition is in the second to third innings. Merrill Lynch also believes that both gross and operating margins finally have reversed from a declining trend.

Xbox sales were strong ahead of the holidays, and Microsoft shares were treated quite well around its most recent earnings report in 2016.

While Microsoft lags Apple in the world’s most valuable brands, the estimates from Thomson Reuters show that Microsoft is expected to grow revenues from $92 billion in 2016 to almost $100 billion in 2018 and then to grow revenues to $111 billion in 2020. Microsoft’s consensus $2.98 in earnings per share for 2017 (June year-end) is just over 20 times expected earnings.

Microsoft no longer has the monopoly for desktop operating systems, and it lags in mobile operating systems for market share. Still, Microsoft’s Azure cloud services efforts have risen with the likes of Amazon’s AWS and other rivals.

Would it surprise you to hear that PCs were making a comeback in 2016? And would it surprise you even more if PCs were going to continue making a comeback in 2017 and the years ahead? It turns out that artificial intelligence, virtual reality and machine learning can take up massive amounts of data and capacity in the processors. Some mobile and cloud use can of course overcome the need for the old desktop and laptops power for games, but much of that will lag greatly versus a robust PC.

It used to be thought that Xbox was a money-loser, but when you consider all that the Xbox platform is used for now it is no longer the case that this is just a money-losing video game effort. Cord-cutters use the Xbox platform, and it can power entire entertainment systems now.

A big unknown for 2017 to 2020 is how Microsoft will capitalize on the LinkedIn acquisition. This will tie in social media and business efforts, and it is important to remember that Nadella has more or less been able to outperform the expectations that his skeptics have voiced. Morgan Stanley voiced that Linkedin will add momentum to an earnings growth story and that aggressive share repurchases drive improving earnings per share growth. Late in December, Morgan Stanley reiterated its Overweight rating, but it raised its price target to $72 from $64 at the time.

[wallst_email_signup]

A sum of the parts analysis can always come up with numbers that seem to aggressive. Companies rarely pursue such strategies, but Oppenheimer’s analyst note in December looked to strip out the impact of earnings from Azure and in the Software as a Service (SaaS) portfolio. Using a 15-time price-to-earnings (P/E) multiple on the legacy businesses and 10 times the revenue multiple on Azure and five times revenues on the SaaS revenue would generate a $76 target, if you add in Microsoft’s net cash.

Microsoft has a 52-week trading range of $48.04 to $64.10 and a market cap of $489 billion. Its dividend yield is 2.5%, but the new administration’s cash repatriation efforts are likely to help drive dividends and share buybacks higher once it can have full access to its $140 billion or so cash trove (at least pre-LinkedIn) in the coming years.

Contact [email protected] for any questions or corrections.