As of Monday night’s close, Boeing Co. (NYSE: BA) has posted a share price gain of just 6.5% for the year to date. In 2017, Boeing’s share price nearly doubled, rising by 89%. What a difference a year makes.

Raising its dividend and announcing a massive new share buyback program are unlikely to push Boeing’s share price gain for 2018 to the stratospheric levels of last year. Such moves couldn’t hurt, though, and Boeing made both late Monday, raising its annual dividend by 20% from $6.84 ($1.71 per quarter) to $8.22 ($2.055 per quarter) and its share buyback program from the $18 billion announced at the end of 2017 to $20 billion.

Is Boeing really that confident or is the company trying to paper over some of the cracks in its walls?

Boeing’s headwinds blew a bit harder in 2018, what with tariffs on steel and aluminum and trade troubles between the United States and Canada. Supply chain issues, including delays in engine deliveries for the company’s 787, were a problem earlier this year. More recently the crash of a Lion Air 737 MAX that killed 189 people has put in jeopardy the remainder of an order for 200 of the planes by the Indonesia carrier. Boeing also is answering investigators’ questions related to the deadly crash.

[nativounit]

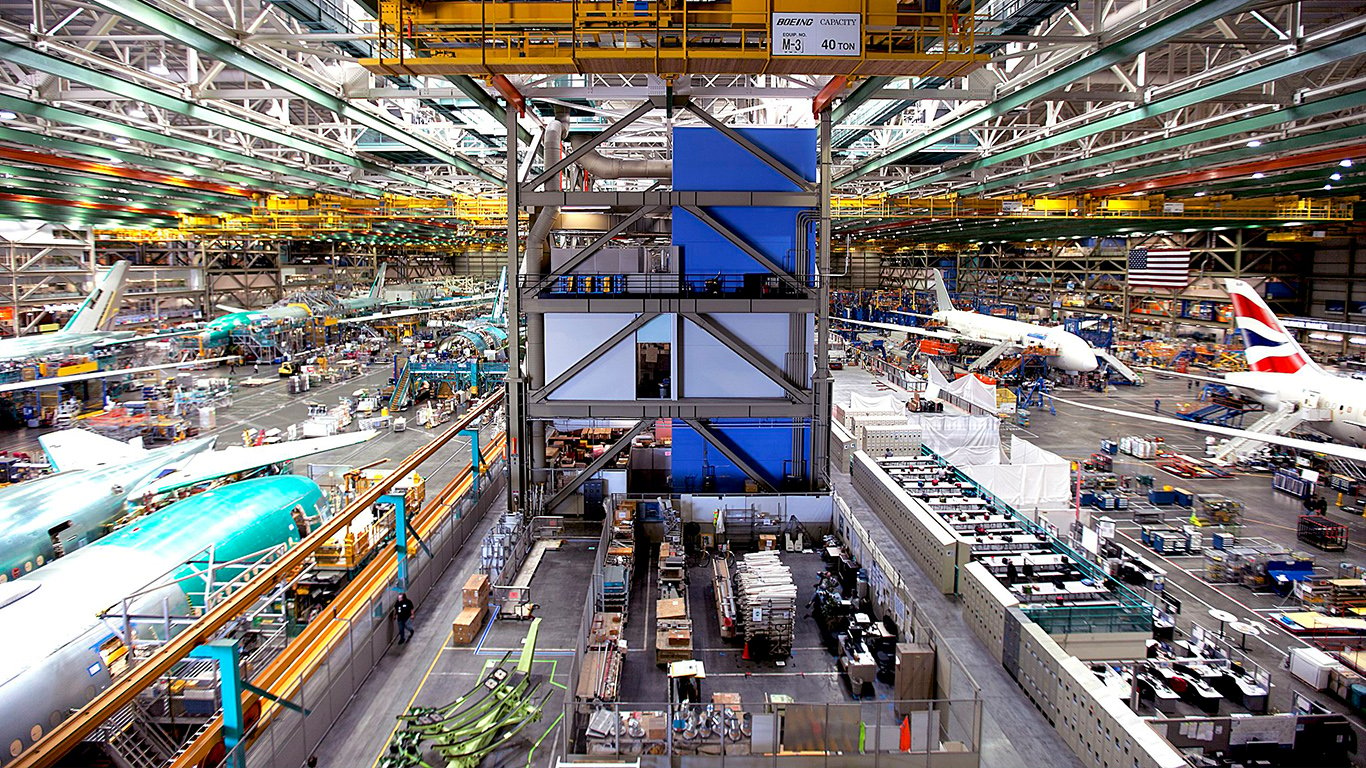

Let’s look at some numbers. Boeing has never wavered from its original target of 810 to 815 new commercial aircraft deliveries in 2018. As of the end of November, the company had delivered 704 jets, including 511 single-aisle 737s and 128 of the 787 Dreamliner. Those two families account for 91% of Boeing’s deliveries so far this year.

To reach 810 deliveries in 2018, Boeing needs to ship 106 aircraft this month. Through all of 2018 so far, Boeing’s best month for deliveries was March when the company shipped 91 new jets.

Production of the 787 is averaging 12 a month while 737 production is running at about 46.5 planes per month. Boeing had delivered nine new 787s as of Sunday and needs to deliver just seven more to maintain the 12-per-month average. That is well within reach and Boeing could even deliver a few more 787s.

To reach its stated goal of 810 deliveries for this year, Boeing needs to ship around 87 new 737s this month, according to AirInsight.com. Jefferies analyst Sheila Kahyaoglu told AirInsight that she reckons Boeing needs to deliver 79 737s this month and that she believes that is “unlikely.”

A miss on deliveries may well be offset by a substantial boost to operating cash flow. Through the first three-quarters of the year, cash flow totaled $12.38 billion, against the company’s full-year estimate of $15.5 billion. Boeing’s third-quarter cash flow totaled $4.56 billion, and there’s no reason to believe fourth-quarter cash flow will be lower than that.

On top of that huge cash performance, now Boeing adds a dividend hike and a juiced-up buyback program. Will all that, plus the recently announced deal with Embraer and the approaching delivery of new KC-46 tankers to the U.S. Air Force, be enough to make investors look past a shortfall in deliveries?

Probably not because investors are far less forgiving than they were even earlier this year. A miss on any benchmark is punished, usually severely. That’s almost entirely outside Boeing’s control.

Boeing’s stock traded up about 2.3% in Tuesday’s premarket session, at $323.50 in a 52-week range of $293.01 to $394.28. The stock’s 12-month share price target is $417.24.

[recirclink id=512008]

[wallst_email_signup]

Contact [email protected] for any questions or corrections.