The Federal Reserve Bank of Kansas City might not be the first place that oil and gas industry watchers think of for evaluating oil and gas trends in hiring and firing, capital spending and future energy trends. Still, the Tenth Federal Reserve District overlaps with some important energy development areas: Colorado, Kansas, Nebraska, Oklahoma, Wyoming, northern New Mexico and western Missouri.

The Federal Reserve Bank of Kansas City might not be the first place that oil and gas industry watchers think of for evaluating oil and gas trends in hiring and firing, capital spending and future energy trends. Still, the Tenth Federal Reserve District overlaps with some important energy development areas: Colorado, Kansas, Nebraska, Oklahoma, Wyoming, northern New Mexico and western Missouri.

It may seem expected that the first-quarter Energy Survey showed negative trends, but there are some hidden gems here that also spell out a real picture of what the oil and gas industry is facing. Some aspects may not even be as bad as some people would guess.

The Energy Survey started out with the news that energy firm activity fell sharply in the first quarter and firms on average plan to cut employment by 12% in 2015. It gave a statement as follows:

Firms have sharply cut capital expenditures and many are also reducing employment and hours. However, firms’ breakeven oil prices have also fallen considerably the past six months, to an average of $62 per barrel, down from $79 per barrel six months ago.

ALSO READ: RBC’s 4 U.S. Energy Best Idea Stocks to Buy

If $62 per barrel is the new breakeven on average, then it means that oil and gas does not have to recover as sharply for the industry to rebound. Also, expectations for future activity were also quite negative, but slightly less so than three months ago. Index readings were as follows:

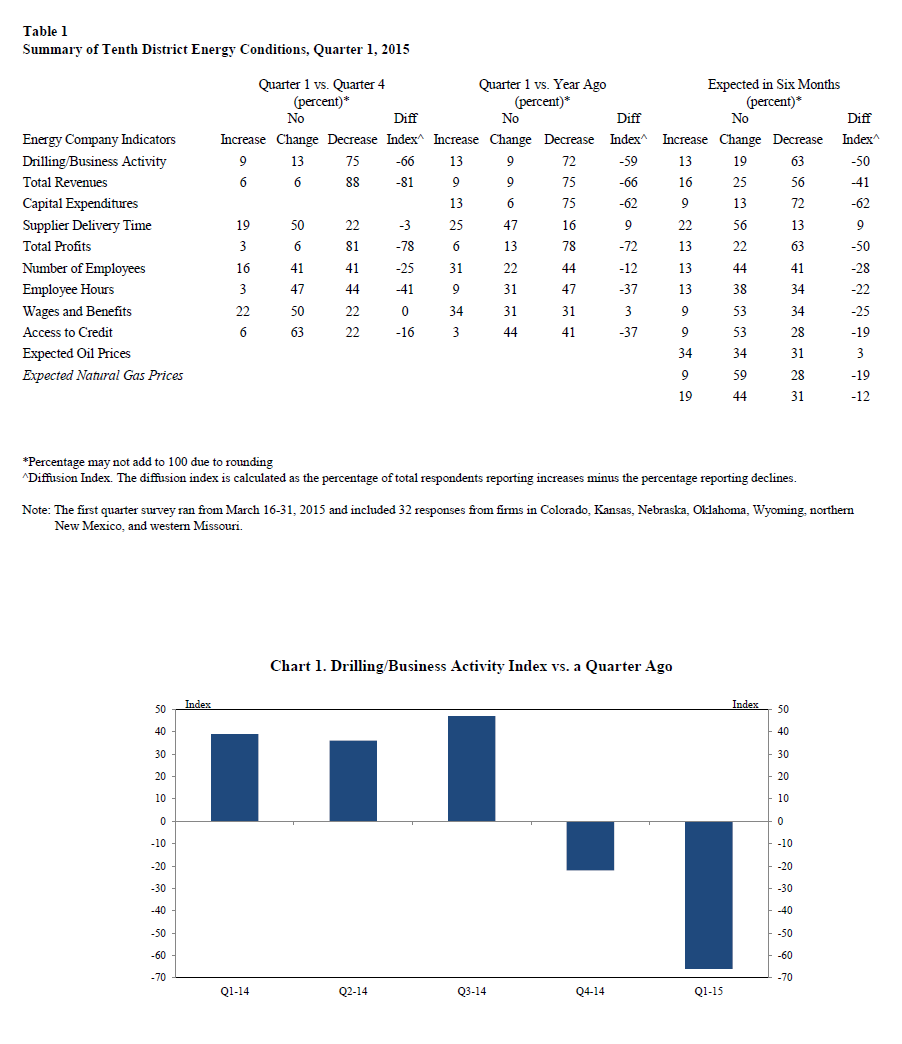

- The drilling and business activity index fell from -22 to -66, while the total revenues index sank to -81.

- The employment index moved into negative territory (see below).

- The employee hours index also dropped as many firms reduced hours and overtime. The wages and benefits index fell to 0.

Expectations were slightly less pessimistic than the previous survey, as follows:

- The future drilling and business activity expectations index rose from -70 to -50.

- The future revenues index also edged higher to -41.

- The employee hours index rose to -22.

- Expectations for employment were negative, falling to -28.

- Future wages and benefits index tumbled to -25.

- Capital spending was also projected to continue declining.

- Access to credit was expected to tighten further.

Maybe news that “less-bad” is good. The Energy Survey showed that the industry outlook for oil and gas prices over the next six months was mixed. The expected oil prices index jumped from -48 all the way up to 3, an indication that firms expect prices to be marginally higher in coming months. The expected natural gas and NGL price indexes also rose but remained below zero, indicating expected price declines over the summer. What outsiders have to consider is whether oil and gas companies are forecasting where they think price will go, or where they hope prices will go.

Compared to a year ago, the Fed survey said:

On a year-over-year basis, activity was significantly lower across the sector. The drilling and business activity index plunged from -19 to -59. Similarly, total revenues were down considerably, and employment was moderately lower than the same quarter last year. The capital expenditures index dropped from -11 to -62, as sizable year-over-year capital budget cuts took effect. Access to credit was also tighter than last year.

ALSO READ: 4 Oil Services Stocks to Buy Without Major Oil Recovery

While the “less-bad” news is better than being worse, we have just seen outside data showing that the U.S. oil rig count dropped again this week. That makes 18 weeks in a row in the red.

A table and chart combined image from the KC Fed has been provided below, showing an index breakdown by each component.

Contact [email protected] for any questions or corrections.