The Federal Reserve Bank of Dallas has released its Texas Manufacturing Outlook Survey, showing that factory activity in the Texas region increased at a faster pace in May. Business executives are now signaling that current manufacturing activity is at the highest level in years. The state’s manufacturing economy has deep ties to the oil economy, and crude oil has spent the second half of May battling whether the price of a barrel of West Texas Intermediate crude will remain above or below $50.

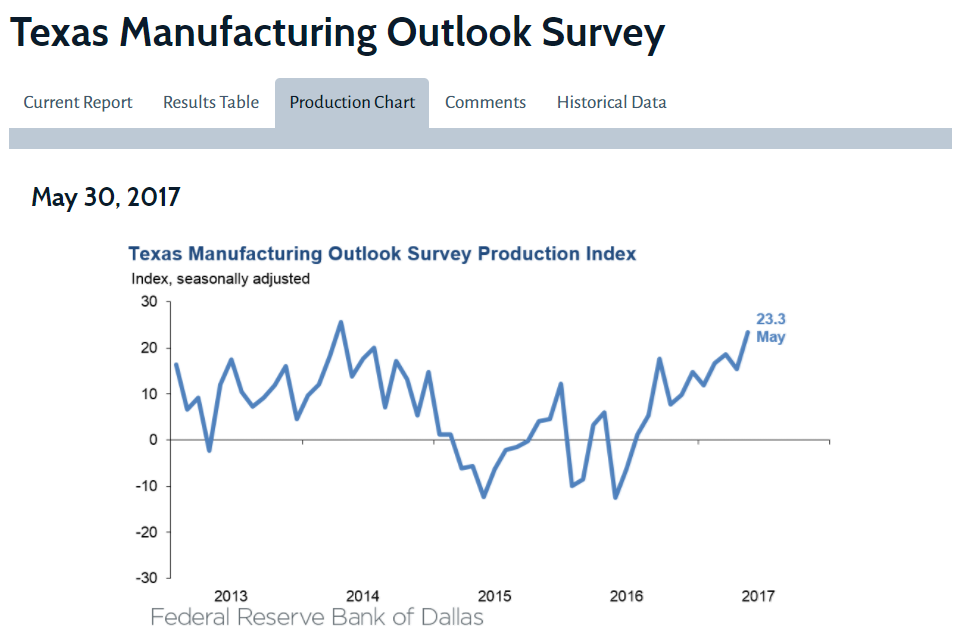

The production index rose by eight points to 23.3, its highest reading since April 2014. It is important to consider that we are now just one month shy of the index having been positive for 12 consecutive months.

Tuesday’s report was almost universally positive. Perceptions of broader business conditions improved again, labor market conditions showed continued employment gains and longer work weeks, wage pressures increased and prices in general continued to rise at a slower pace in May. Expectations of future business conditions continued to improve and other measures for future manufacturing activity pushed further into positive territory.

Data were collected from May 16 to May 24 from 113 Texas manufacturers that responded to the Federal Reserve’s regional survey. That puts the dates of the survey just days ahead of OPEC’s most recent continuation of oil production cuts.

[nativounit]

The general business activity index rose to 17.2 in May from 16.8 in April. Some 30.7% of firms showed improving activity, versus 13.5% showing lower activity. Another show of force was from the company outlook index rising 5.1 points to 20.2 in May. Of the companies showing an improving or contracting outlook, 29.4% were positive and just 9.2% of firms were negative.

Other individual index readings were shown as follows, with some commentary:

- The new orders index pushed up to 18.1, and the growth rate of orders index rose to 12.3 (its fifth consecutive positive reading).

- The capacity utilization index moved up to 19.4 (about one-third of firms noted increased utilization).

- The shipments index rose by 15 points to 24.7 (almost a 10-year high).

- The employment index came in at 8.3 (its fifth consecutive positive reading).

- Eighteen percent of firms noted net hiring.

- Ten percent of firms noted net layoffs.

- The hours worked index rose 10 points to 15.7 (the highest reading in six years).

- The raw materials prices index fell three points to 17.5.

- The finished goods prices index fell to 5.9 from 12.0.

- The wages and benefits index rose to 24.3 (larger gains in compensation costs than in April).

- The index of future general business activity rose to 31.6.

- The future company outlook rose to 30.9.

- The capital expenditures index was still strong at 24.8 in May, but down 1.2 points from the 26.0 reading in April.

The Fed’s report also showed that the only two negative readings were in measurements inventories, which may indicate that more production strength will be seen ahead, based upon stronger outlook data already noted above. The materials inventories index fell to –2.3 in May after having been at a positive 2.2 in April. The finished goods inventories fell to –1.8 in May after having been at 1.0 in April.

Texas matters when it comes to manufacturing. The Dallas Fed noted that Texas has accounted for about 9.5% of the total U.S. manufacturing output and that Texas ranks only behind California in factory production. Texas ranked first as an exporter of manufactured goods.

According to the Dallas Fed, each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. Positive readings indicate growth and negative readings generally correspond with lower levels or contraction. The Fed’s explanation notes:

When the share of firms reporting an increase exceeds the share reporting a decrease, the index will be greater than zero, suggesting the indicator has increased over the prior month. If the share of firms reporting a decrease exceeds the share reporting an increase, the index will be below zero, suggesting the indicator has decreased over the prior month. An index will be zero when the number of firms reporting an increase is equal to the number of firms reporting a decrease.

[wallst_email_signup]

Contact [email protected] for any questions or corrections.