A recent study published by Third Way, a national think tank that “champions modern center-left ideas,” suggests that sales of new light vehicles (passenger cars, pickups, and SUVs/crossovers) powered by internal combustion engines (ICEs) reached a peak in 2016 and “likely will never be as high” again.

The study attributes the decline to rapid growth and the “competitive viability of electric vehicles” (plug-in hybrid and all-electric vehicles). Since 2015, sales of electric vehicles have grown by a factor of four and will reach an estimated total of 433,000 in the United States this year. Total new light-vehicle sales are forecast at around 16.6 million, but growth is negative.

Third Way notes four reasons for the rise in electric vehicle sales. First, consumers will have a wider choice of models. In 2017 there were just 18 models to choose from. By 2022, Third Way projects that 81 models will be available and that will rise to 133 by 2026.

Second, battery costs are falling. Between 2010 and 2019, the cost per kilowatt-hour (kWh) has dropped from around $1,000 to $176 and battery pack costs are expected to fall below $100 per kWh over the next three to five years.

Third, home charging is more convenient than stopping at a gas station and more charging stations at work and in the community will only make electric vehicles more convenient.

Fourth, as Americans face the expected effects of climate change they will place more value on vehicles that eliminate fossil fuels from the transportation sector.

[nativounit]

Andy Hall, a long-time oil trader and hedge fund manager, took a different approach to the rise of electric vehicles in a speech to an industry conference earlier this month. Hall said, “There’s a non-zero chance that by 2030, we will see a plateauing or decline in global oil consumption. It’ll happen because of technology, electric cars, renewable energy.”

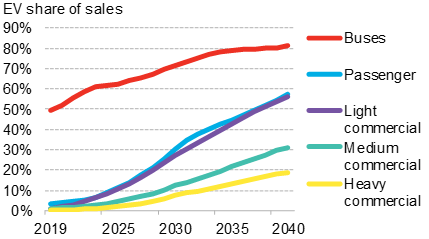

The International Energy Agency (IEA) has also forecast a plateau for oil demand beginning around 2030. The current demand growth rate of around 1% (about 1 million barrels a day) will dive to just 100,000 barrels a day in the 2030s. By 2040, the IEA expects demand to be 106.4 million barrels a day.

As Hall recalled in his presentation, former Saudi oil minister Sheikh Ahmad Zaki Yamani famously quipped that the Stone Age didn’t end because the world ran out of stones and the Oil Age will not end because the world runs out of oil.

So why are oil companies continuing to spend massive amounts of cash on developing new hydrocarbon assets? Between 2018 and 2030, demand growth for crude oil will rise from 96.9 million barrels a day to 105.4 million barrels before tapering to 100,000 barrels a day for the next decade. This could be the last hurrah for the oil companies and none wants to be left with a portfolio of assets that will be losing value. Now’s the time for new thinking.

Exxon Mobil is the fifth most innovative company out of 640 included in the 2019 rankings by the Drucker Institute, trailing only Amazon, Microsoft, Apple, and IBM and well ahead of such luminaries as Alphabet, Facebook, Cisco, and Nvidia.

Exxon is spending big, according to The Wall Street Journal, to make oil and natural gas as competitive as possible, “believing the world will need fossil fuels for the foreseeable future.” That is very likely and with demand falling, exploration will be curtailed and having a portfolio of producing assets ensures that Exxon continues to make money.

Royal Dutch Shell plc (NYSE: RDS-A) has taken a different view. In July, CEO Ben van Beurden said the Anglo-Dutch giant would get into the cleaner business of selling electricity. The company, van Beurden said, has a “preference for being asset-light and [will] balance our supply by providing electricity from other producers.” Shell is aiming at being the world’s largest electric power company by the early 2030s.

Both Exxon and Shell have reached the starting line with massive reserves of assets. Exxon, which believes in a role for fossil fuels beyond 2040, has chosen to milk the next two decades for all it can get from its fossil fuel assets. Shell, which recognizes that operating in a highly regulated business like electric power generation does not pay off as well as the less-regulated oil business, is betting that it can buy electricity from utilities that have a track record of not being very efficient sellers of their own product.

Shell has forecast that more than a quarter of global demand for energy will be fulfilled by electricity by 2030, up from around 18% currently. By 2050, the company forecasts electricity will meet as much as 50% of the world’s demand for energy.

What could derail either or both approaches? Exxon may have the more tenuous grip on the future. If global governments get serious about reducing the amount of fossil fuels used in transportation, various incentives driving consumers to turn to electric vehicles could shorten Exxon’s foreseeable horizon. Like Third Way, BloombergNEF sees sharp drops in battery costs making electric vehicles cheaper than ICE vehicles sometime between 2025 and 2030.

Shell’s biggest problem might be timing. It can’t afford to jettison its fossil fuels business too early, but neither can it afford to wait too long. And even if it succeeds in becoming the world’s largest electricity company, will it be able to maintain shareholder returns. Its current dividend yield is nearly 6.5%. NextEra Energy, one of the largest U.S. providers of renewable and natural-gas electricity pays a yield of 2.13%. France’s Electricite de France pays a yield of 3.4% and Germany’s RWE yields about 2.65%. All three would be considered asset-heavy in Shell’s view.

Regardless of which approach prevails, global carbon emissions will continue to rise after 2040, according to the IEA. Even with fossil-fuel demand growth of just 1%, the agency sees “a world in 2040 where hundreds of millions of people still go without access to electricity, where pollution-related premature deaths remain around today’s elevated levels, and where CO2 emissions would lock in severe impacts from climate change.”

[wallst_email_signup]

Contact [email protected] for any questions or corrections.