The three major U.S. equity indexes closed lower Monday. The Dow Jones industrials closed down 0.5%, the S&P 500 dropped 1.2% and the Nasdaq shed 2.3%. Nine of the 11 S&P sectors closed lower. Only utilities (up 0.6%) and real estate (unchanged) managed to avoid losses. A strengthening dollar is raising concerns that global results from U.S. multinationals will be weaker. All three major indexes were lower in Tuesday’s premarket session.

Before markets opened on Tuesday, PepsiCo beat consensus estimates on both the top and bottom lines, reaffirmed previous fiscal year earnings per share (EPS) guidance and raised its organic sales growth estimate from 8% to 10%. Shares traded up about 1.6% early Tuesday.

The June-quarter earnings season revs up later this week when the nation’s biggest banks begin releasing their quarterly results. Added loan loss reserves are expected to hack away at profitability. Recession fears could lead the country’s top four lenders to record loss provisions of $3.5 billion, compared to a benefit of $6.2 billion in the year-ago quarter.

Before U.S. markets open on Wednesday, Delta Air Lines and Fastenal will report quarterly results.

[nativounit]

Here is a look at five companies on deck to report quarterly results before markets open Thursday morning.

Conagra

Over the past 12 months, the share price of packaged food giant Conagra Brands Inc. (NYSE: CAG | CAG Price Prediction) has increased by about 2.1%. Inflationary pressure was expected to raise costs for transportation and dairy and meat products. On the March-quarter conference call, CFO David Marberget noted that fiscal 2021 costs in Conagra’s meat business totaled $675 million, and the company is forecasting a 50% jump to about $1.2 billion for fiscal 2022.

Of 17 analysts following the stock, 13 have a Hold rating, while the rest rate the shares at Buy or Strong Buy. At a recent share price of around $35.60, the stock trades essentially at its median price target of $36.00. At the high price target of $44.050, the upside potential is 23.6%.

The consensus estimate for fiscal fourth-quarter revenue is $2.93 billion, which would be up 0.5% sequentially and by 6.9% year over year. Adjusted EPS are expected to come in at $0.63, up 9.3% sequentially and 16.7% higher year over year. The current estimates for the 2022 fiscal year that ended in May call for EPS of $2.35, down about 11.1%, on sales of $11.55 billion, up 3.3%.

[recirclink id=1151349]

The stock trades at 15.2 times expected 2022 EPS, 14.0 times estimated 2023 earnings of $2.54 and 13.1 times estimated 2024 earnings of $2.72 per share. Conagra’s 52-week trading range is $30.06 to $36.97, and the company pays an annual dividend of $1.21 (yield of 3.52%). Total shareholder return over the past 12 months is 2.12%.

Ericsson

Stockholm-based network equipment maker Telefonaktiebolaget LM Ericsson (NYSE: ERIC), once a powerhouse in the cellphone business, has seen its share price drop by 43% over the past 12 months. Shares plummeted in February when the company replied to reports of Ericsson dealings with Iraq that may have inadvertently funded the Islamic State (ISIS). Now the company is involved in a patent dispute with Apple over Ericsson 5G patents in at least six countries, including the United States and the United Kingdom.

Of 21 analysts covering the stock, 13 rate Ericsson at Buy or Strong Buy. There are six Hold ratings as well. Based on a median price target of $13.04 and a share price of around $7.30, the upside potential is 78.6%. At the high price target of $15.10, the upside potential is around 107%.

Analysts expect the company to report fiscal second-quarter revenue that is down 1.6% sequentially and 10.3% lower year over year. EPS are forecast at $0.16, up 55.5% sequentially and 23% year over year. For the full year ending in December, analysts are looking for EPS of $0.73, down 6%, and revenue of $23.92 billion (down 6.9%).

The stock trades at 10.2 times expected 2022 EPS, 9.2 times estimated 2023 earnings of $0.81 and 8.4 times estimated 2024 earnings of $0.89 per share. Ericsson’s 52-week range is $7.22 to $13.40, and the company pays an annual dividend of $0.27 (yield of 2.24%). Total shareholder return over the past 12 months is negative 43%.

[recirclink id=1149912]

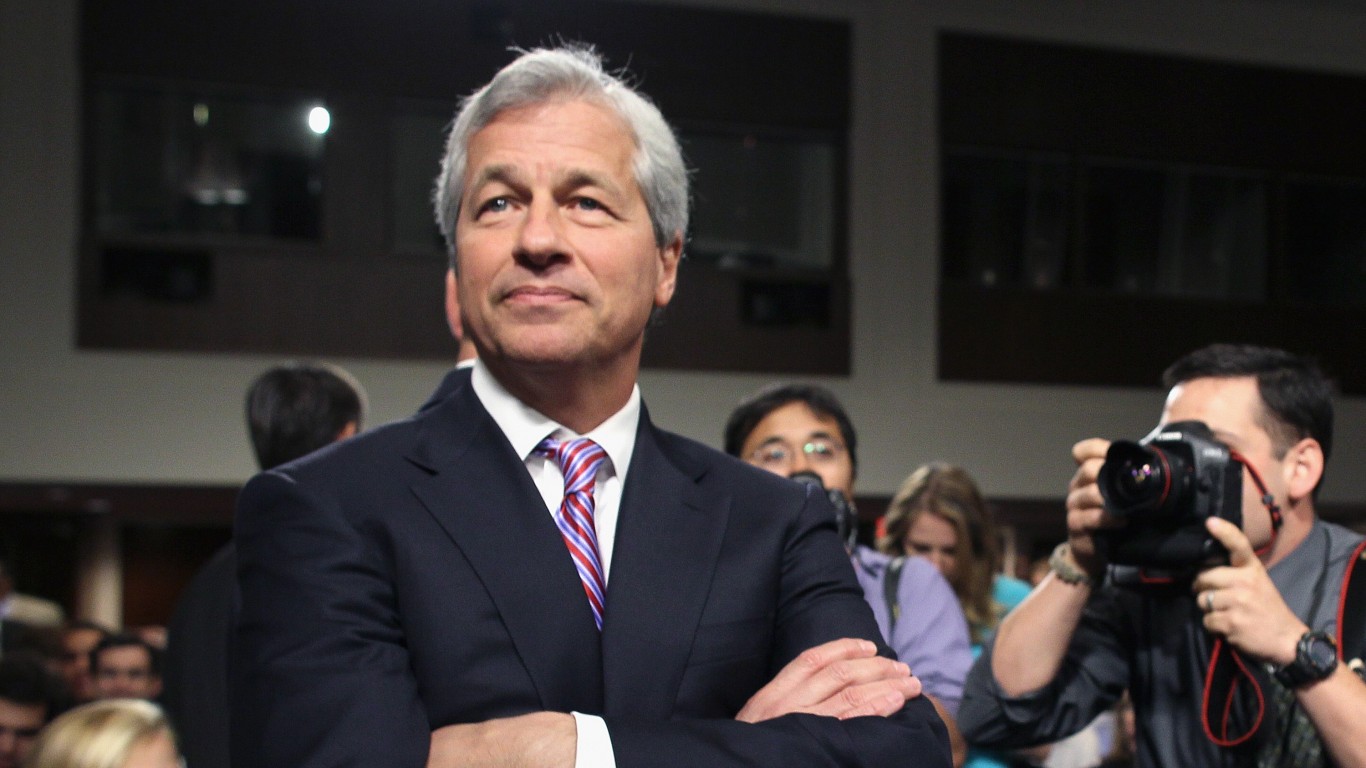

JPMorgan

The largest (by market cap) of the big U.S. banks, JPMorgan Chase & Co. (NYSE: JPM) has seen a share price decline of about 25.5% over the past 12 months. Rising interest rates have helped JPMorgan as it has all banks. One issue facing the country’s big banks is maintaining their provisions for bad loans. That is a particular issue for JPMorgan, which prides itself on its fortress balance sheet. CEO Jamie Dimon’s comments should be revealing.

Of 26 analysts covering the stock, 14 have a Buy or Strong Buy rating, while another 10 rate the shares at Hold. At a trading price of around $112.90, the upside potential based on the median price target of $149.00 is 32%. At the high price target of $200.00, the upside potential is 77.1%.

Analysts expect JPMorgan to report second-quarter revenue of $31.74 billion, up by about 3.3% sequentially and 4.1% year over year. Adjusted EPS are forecast at $2.91, up 10.5% sequentially but down 23% year over year. For full fiscal 2022, current estimates call for EPS of $11.28, down 26.3%, on revenue of $126.34 billion, up 3.9%.

The stock trades at 10.0 times expected 2022 EPS, 8.9 times estimated 2023 earnings of $12.74 and 8.2 times estimated 2024 earnings of $13.79. The stock’s 52-week range is $109.60 to $172.96. JPMorgan pays an annual dividend of $3.90 (yield of 3.54%). Total shareholder return for the past 12 months was negative 25.5%.

Morgan Stanley

Morgan Stanley (NYSE: MS) has seen its share price drop by about 13.5% over the past 12 months. From the 52-week high set in February, the stock is down nearly 29%. Rising interest rates only help lenders if someone wants to borrow. Worse for Morgan Stanley, though, would be a further drop in its investment banking business. The first-quarter slowdown in mergers and acquisitions shaved nearly 40% from the bank’s institutional securities business. The second quarter is unlikely to show a marked improvement.

Sentiment remains bullish on the stock, with 21 of 29 brokerages assigning a Buy or Strong Buy rating. The rest rate the stock at Hold. At a share price of around $75.80, the upside potential based on a median price target of $97.00 is nearly 30%. At the high target of $123.00, the upside potential is 62.3%.

The consensus estimate for second-quarter revenue is $13.53 billion, down about 8.6% sequentially and about 12% lower year over year. Adjusted EPS are forecast at $1.61, down nearly 22% sequentially and 14.8% year over year. For the full 2022 fiscal year, analysts are looking for revenue of $56 billion, down 6.3%, and EPS of $7.25, down by 11.8%.

Morgan Stanley stock trades at 10.5 times expected 2022 EPS, 9.4 times estimated 2023 earnings of $8.02 and 8.5 times estimated 2024 earnings of $8.93. The stock’s 52-week range is $72.23 to $109.73, and the bank pays an annual dividend of $2.80 (yield of 3.69%). Total shareholder return over the past year was negative 13.5%.

[wallst_email_signup]

Taiwan Semiconductor

Last week, Taiwan Semiconductor Manufacturing Co. Ltd. (NYSE: TSM) reported that June sales dropped by 5.3% month over month but rose 18.5% year over year. Sales for the first six months of the year are up nearly 40%, compared with sales during the same period in 2021. Second-quarter sales topped NT$500 billion ($16.8 billion) for the first time in the company’s history. The weaker local currency and strong U.S. dollar are at least partially responsible for the record quarter.

Of 11 analysts covering the stock, nine have a Buy or Strong Buy rating and one has a Hold rating. At a share price of around $79.10, the implied upside based on a median price target of $157.90 is 99.6%. At the high price target of $150.00, the upside potential is 127.6%.

[recirclink id=1150132]

For TSMC’s second quarter of fiscal 2022, analysts are looking for revenue of $17.46 billion, up 1.8% sequentially and 31% higher year over year. Adjusted EPS are expected to come in at $1.49, up 6.3% sequentially and by 684% year over year. For the full fiscal year, EPS are forecast at $5.90, up 43.1%, on revenue of $70.55 billion, up 23.3%.

The stock trades at 2.6 times expected 2022 EPS, 2.6 times estimated 2023 earnings of $6.06 and 2.1 times estimated 2024 earnings of $7.49. The stock’s 52-week range is $73.74 to $145.00, and the company pays an annual dividend of $1.95 (yield of 2.39%). Total shareholder return for the past 12 months is negative 33.4%.

Contact [email protected] for any questions or corrections.