Income-focused investors face a persistent challenge: finding yield without sacrificing capital stability. The SPDR Blackstone High Income ETF (NYSEARCA:HYBL) blends high-yield corporate bonds, senior loans, and collateralized loan obligations (CLOs) into a single actively managed portfolio.

How HYBL Fits In Your Portfolio

HYBL serves as a fixed-income position for investors seeking monthly income with moderate credit risk exposure. The fund’s return engine operates through three channels: interest payments from high-yield bonds, floating-rate coupons from senior loans, and structured credit returns from CLO tranches. Sub-advised by Blackstone Credit, the ETF uses top-down allocation to shift weights among these three asset classes based on market conditions, paired with bottom-up security selection.

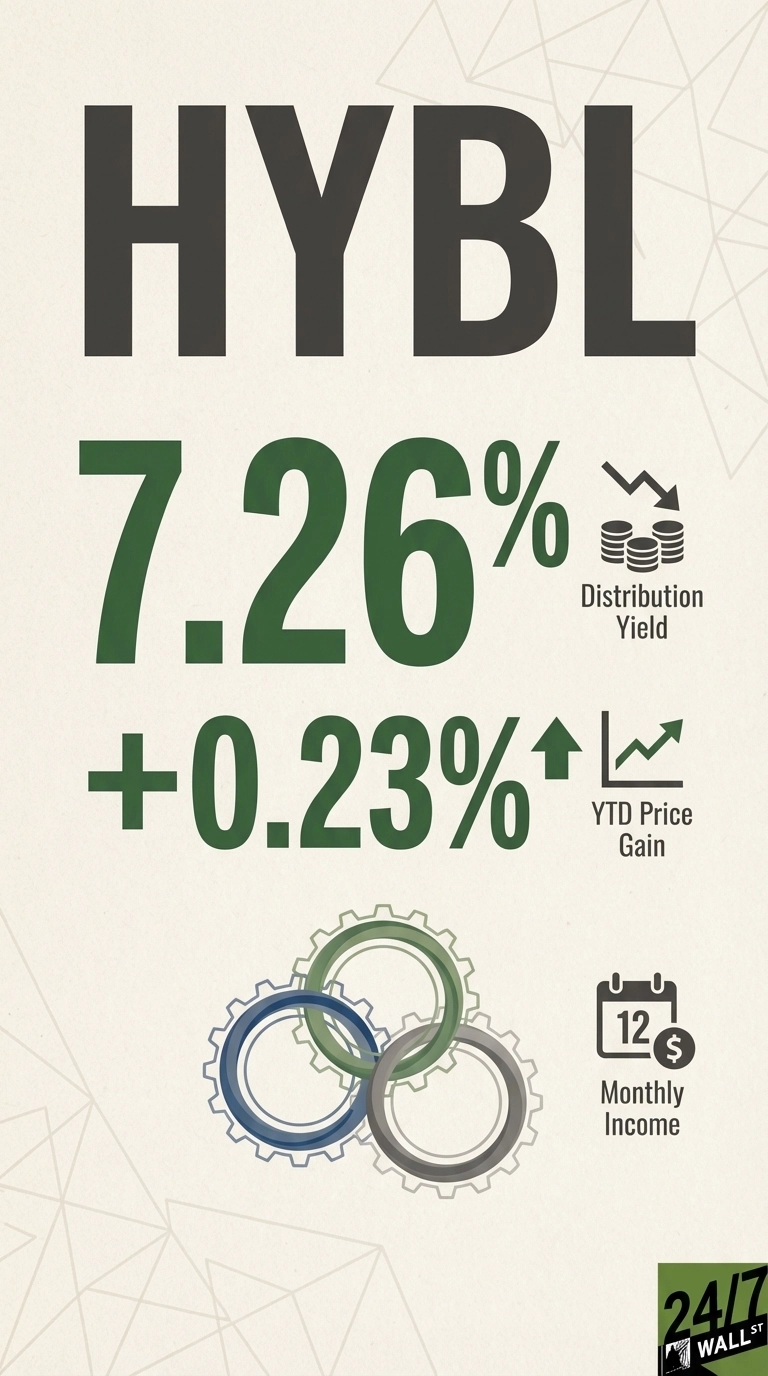

The strategy targets investors who want exposure to below-investment-grade credit but prefer professional management over direct bond or loan ownership. With 671 holdings and a weighted average all-in rate of 7.06%, the fund distributes income monthly. The 30-day SEC yield stands at 6.76%, though the fund distribution yield based on actual payouts reaches 7.26%. One Reddit user in the r/dividends community asked whether HYBL would be “a good diversification for high income” alongside equity-based income funds like JEPI and JEPQ, highlighting how investors view it as a complement to covered-call strategies.

Whether It Achieves That Goal Well

HYBL has delivered on its capital preservation mandate in 2025. The ETF opened the year at $28.39 on January 2 and closed at $28.455 on December 12, producing a 0.23% price gain. Including monthly distributions totaling approximately $1.89 per share through December, the total return for 2025 reached 7.38% year-to-date, slightly outperforming the high-yield bond category average of 7.34%.

Price volatility has been remarkably low. The ETF experienced its most significant drawdown in April 2025, falling to $27.01 on April 8th (a 4.86% decline from the year’s opening price). It recovered within 30 trading days and has since traded in a narrow range between $28.40 and $28.70 for eight consecutive months. This stability reflects the underlying credit quality and diversification across 671 positions, though returns come primarily from income rather than capital appreciation.

The Tradeoffs Investors Must Accept

The 0.70% expense ratio is higher than passive bond ETFs but reasonable for an actively managed credit strategy with Blackstone’s sub-advisory involvement. Investors pay for active allocation decisions and credit research, which may justify the cost during credit stress but represents a drag during stable markets.

Credit risk remains the primary concern. The fund invests in below-investment-grade debt, and senior loans often finance leveraged buyouts or highly indebted companies. While senior loans offer first-lien protection in bankruptcy, defaults still result in losses. CLO tranches add structural complexity and can behave unpredictably during liquidity crises, as seen in March 2020 when even AAA-rated CLO tranches experienced price dislocations.

Contact [email protected] for any questions or corrections.