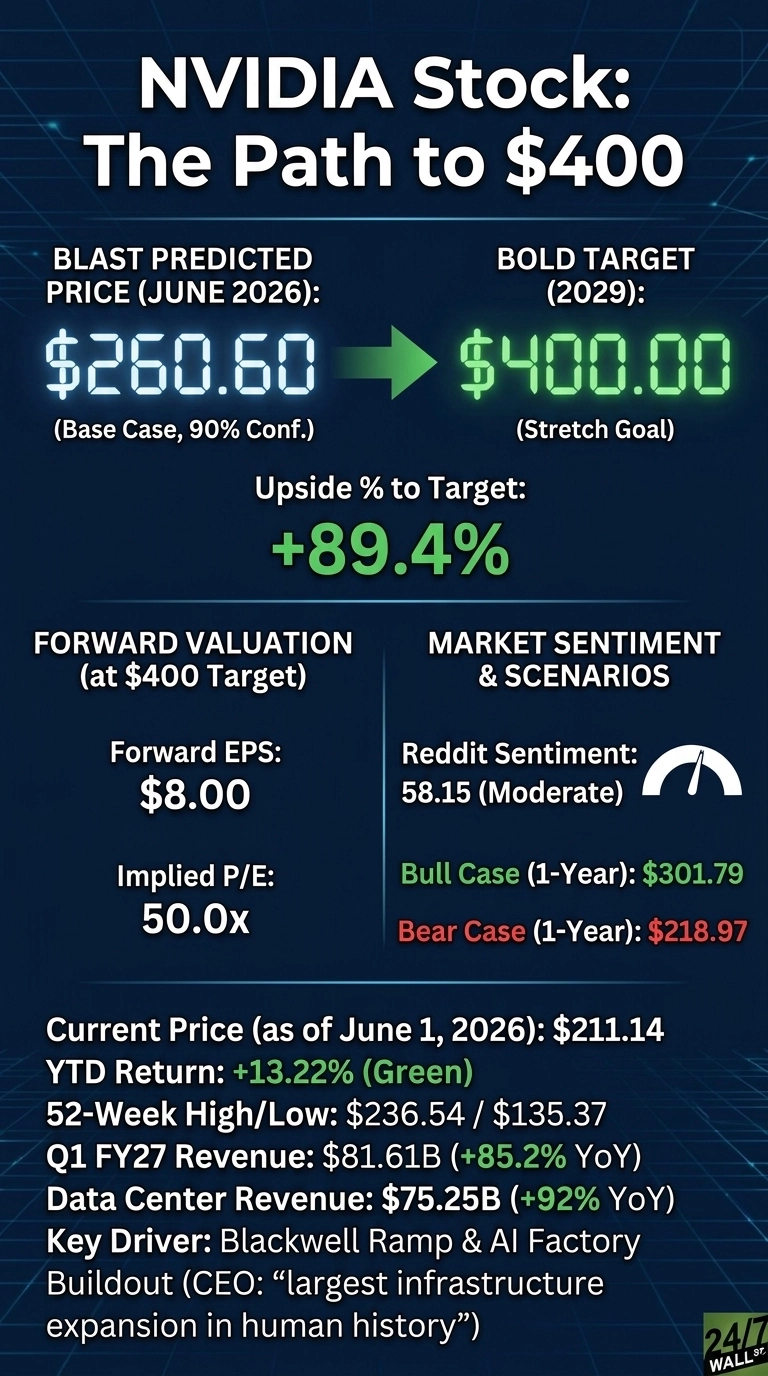

NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) delivered $81.61 billion in Q1 FY2027 revenue, up 85.23% year over year, with data center sales hitting $75.25 billion, up 92%. Yet shares are only up 13.22% year to date, sitting at $211.14.

CEO Jensen Huang calls this “the largest infrastructure expansion in human history.” Can NVIDIA shares reach $400 by 2029?

Why NVIDIA Shares Are Stuck Despite Record Earnings

The disconnect is real. Even after a blowout quarter, NVDA is down 1.95% over the past week and barely positive 0.9% over the past month. Three headwinds weigh on the stock:

First, China. NVIDIA guided no Data Center compute revenue from China in Q2 FY27, versus $4.6 billion a year ago. Second, supply concerns. NVIDIA carries $119 billion in supply commitments, a number that scares investors who remember past inventory cycles. Third, volatility. With a beta of 2.24, NVDA moves roughly twice the market, and traders are skittish at all-time-high valuations.

Reddit and stock chatter have flagged a 38% decline in H200 GPU rental prices through late May, raising questions about whether hyperscaler demand is plateauing.

Wall Street Sees 41% Upside. Our Model Says It’s Bigger

The Street is bullish. 10 strong buys, 48 buys, 2 holds, and just 1 sell, with a consensus target of $296.81. That’s 95% bullish sentiment. Our internal model places base-case fair value at $260.60 with 90% confidence, with a bull case of $301.79 on a one-year horizon.

Push out to 2029 and our base case checkpoint is $338.39, with the bull case at $388.10. Analysts appear too conservative on 2027 earnings power. Quarterly earnings grew 214.5% year over year, and forward EPS estimates haven’t fully caught up to the Blackwell ramp.

The Path to $400 Per Share

Reaching $400 from today’s price of $211.14 would require a gain of 89.4%. With forward EPS of $8, a price of $400 implies a forward P/E of 50x. Our base case of $260.60 already implies 36x, meaning the bold target requires roughly 14x of additional multiple expansion or, more realistically, EPS growth that compresses that multiple.

The EPS path matters more. Internal podcast commentary already cites an upgrade calling for $8 in EPS in 2026 and $11 in 2027. If NVIDIA earns $11 in fiscal 2027 and grows from there, $400 at a sane 30x to 35x multiple by 2029 becomes achievable.

Huang himself sees “tens of gigawatts of NVIDIA AI infrastructure in the not-too-distant future” and “some 800 AI factories being built.” The primary risk is a hyperscaler CapEx air pocket if model training economics roll over.

Where NVIDIA Trades Today vs Its Earnings Power

At $211.14 against forward EPS of $8, NVDA trades around 26x forward earnings. That’s cheap for a company growing data center revenue 92% with a 75% non-GAAP gross margin. Shares sit between a 52-week high of $236.54 and a low of $135.37, and have returned 1,203% over five years and 18,311% over ten. If the AI buildout is real, today’s multiple isn’t expensive.

Is $400 Realistic? Here’s My Verdict

$400 by 2029 requires an 89.4% gain. It’s a stretch, but not crazy.

Three things need to go right: EPS must clear $11 to $13 by fiscal 2028, the Vera Rubin platform must ramp as cleanly as Blackwell, and Washington must provide daylight on China export rules. What derails it is a hyperscaler CapEx pause that lets inventory pile up against those $119 billion in commitments. We’ve outlined the blueprint for how NVIDIA could reach $400 in 2029.

Contact [email protected] for any questions or corrections.