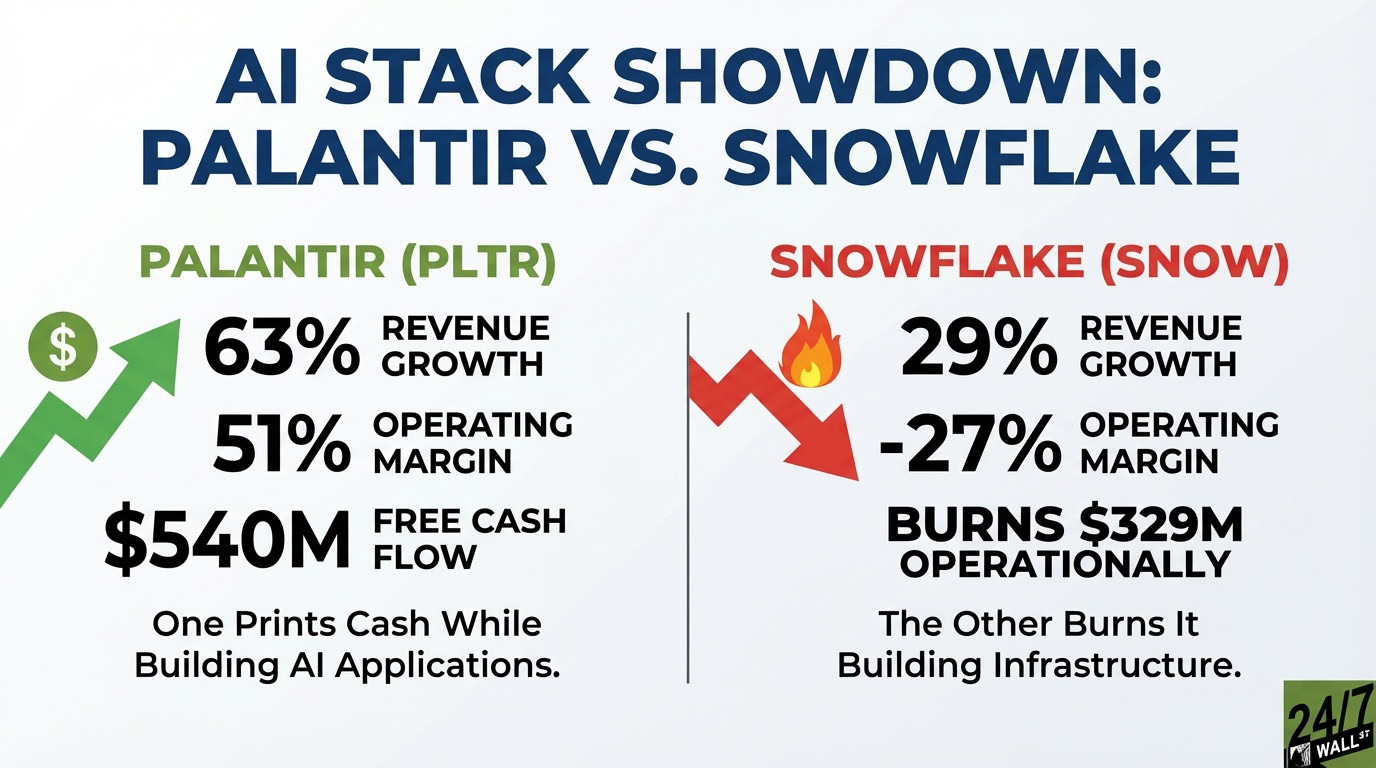

Palantir (NYSE: PLTR | PLTR Price Prediction) and Snowflake (NYSE: SNOW) just reported earnings revealing two companies attacking AI from opposite ends of the stack. Palantir posted 63% revenue growth with 51% operating margins. Snowflake grew 29% but burns cash with a negative 27% operating margin.

One Prints Cash While Building AI Applications. The Other Burns It Building Infrastructure.

Palantir’s Q3 showed a company hitting escape velocity. U.S. commercial revenue surged 121% to $397 million. The Artificial Intelligence Platform (AIP) drives customers from boot camp to seven-figure deals in under two months. CEO Alex Karp: “We have 44% growth in the most important market in the world while having a Rule of 68, the best in the world. We are going to maintain the contradiction of having both high margins and high growth.”

That Rule of 68 score (growth rate plus operating margin) is exceptional. Palantir generated $393 million in operating income, up 248% year over year, and $540 million in free cash flow. The company crossed $1 billion in trailing 12-month free cash flow for the first time.

Snowflake’s quarter looked solid on the surface. Revenue hit $1.21 billion, beating estimates, with product revenue up 29%. Net revenue retention held at 125%, and the company added customers spending over $1 million. But Snowflake lost $329 million operationally and $288 million net. Cash flow was positive at $138 million, but the path to sustained profitability remains murky.

| Metric | Palantir | Snowflake |

| Revenue Growth | 63% | 29% |

| Operating Margin | 51% | -27% |

| Free Cash Flow | $540M | $138M |

| Market Cap | $437B | $75B |

Application Layer Versus Data Foundation

Palantir bets AI value lives in production deployment, not model training. CTO Shyam Sankar: “The models are converging while pricing for inference is dropping significantly. This only strengthens our conviction that the value is in the application and workflow layer.” AIP automates workflows. One insurance customer cut underwriting time from two weeks to three hours using 78 AI agents. Trinity Rail saw a $30 million bottom-line impact in three months.

Snowflake owns the data warehousing layer. CEO Sridhar Ramaswamy emphasized “there is no AI strategy without a data strategy.” Snowflake Intelligence saw strong early adoption. But Snowflake must convince customers to consolidate workloads onto its platform while competitors like Databricks and cloud providers push their own solutions.

Palantir also benefits from government revenue (52% growth to $486 million) that Snowflake lacks. Maven Smart System reduced military targeting cells from 2,000 people to 20, a 100x efficiency gain.

Valuation Reflects Two Different Bets

Palantir trades at 112x sales despite being profitable. Snowflake trades at 17x sales despite losing money. The market prices Palantir for continued AI dominance and margin expansion. Snowflake gets valued as a turnaround play.

Palantir has mostly Hold ratings with a $186 target price (current price near $191). Snowflake has 43 Buy or Strong Buy ratings with a $282 target (29% upside from $218). Institutional ownership favors Snowflake at 74% versus Palantir’s 60%.

Why I Would Choose Palantir Despite the Valuation

For AI application software exposure with proven unit economics, Palantir is the cleaner bet. The 51% operating margin gives management room to invest aggressively without sacrificing profitability. AIP’s rapid customer conversion (boot camp to contract in weeks) suggests a product solving real problems. The valuation is absurd at 112x sales, but execution justifies premium pricing.

Snowflake appeals if you believe data infrastructure will consolidate and margins will flip positive at scale. The 29% growth rate is respectable, and $7.88 billion in remaining performance obligations provides revenue visibility. But I need to see operating leverage before committing capital. Burning $329 million operationally while growing 29% suggests the business model needs work. For now, Palantir’s combination of growth and profitability wins.

Contact [email protected] for any questions or corrections.