UiPath (NYSE: PATH | PATH Price Prediction) and Palantir Technologies (Nasdaq: PLTR) both beat Q3 estimates, but the results reveal fundamentally different AI business models. UiPath turned its first GAAP profit on automation software that executes tasks. Palantir posted 63% revenue growth on analytics software that interprets data.

Automation Agents vs. Data Intelligence

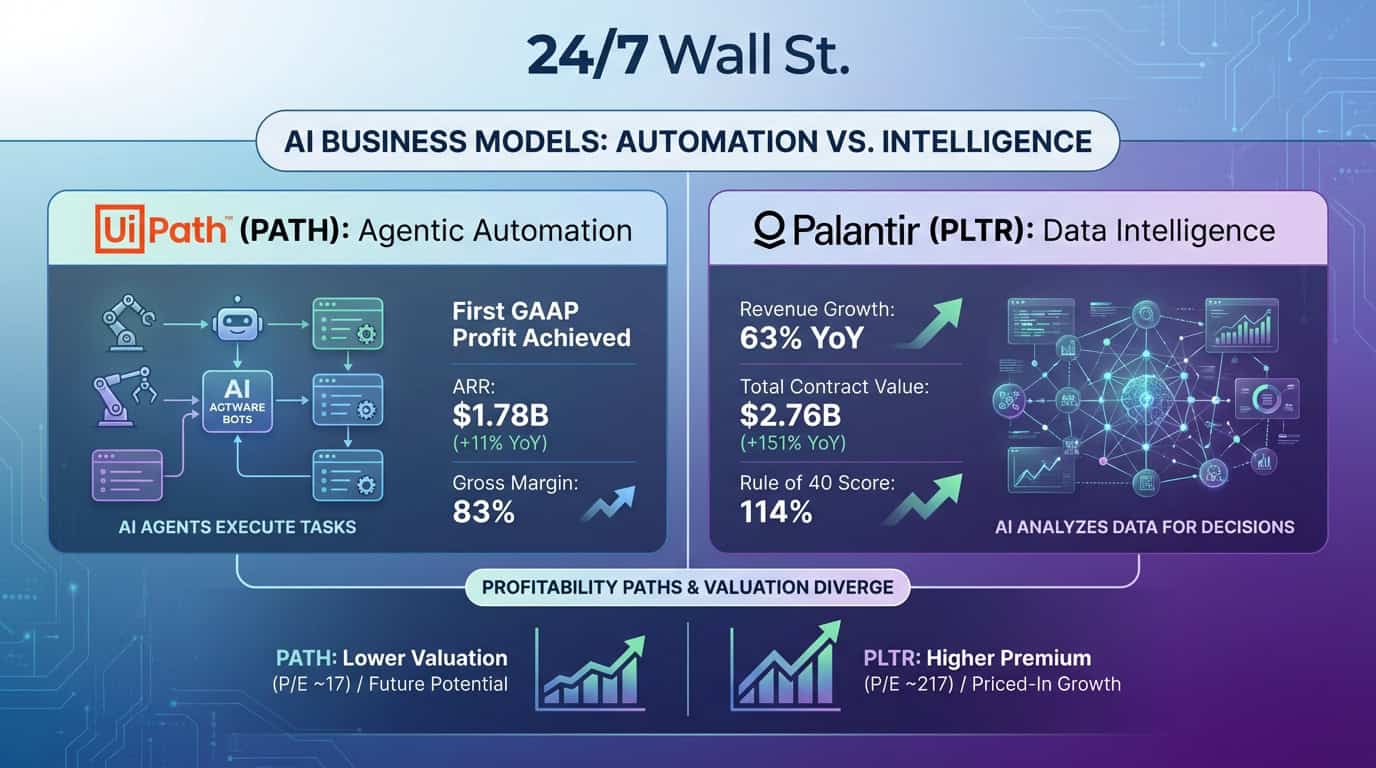

UiPath delivered $411 million in Q3 revenue, beating estimates by $10 million, with annual recurring revenue of $1.78 billion up 11% year-over-year. The company achieved $13 million in GAAP operating income for the first time, validating CEO Daniel Dines’ “agentic automation” vision. The platform now orchestrates AI agents that autonomously handle business processes rather than automating repetitive clicks. Gross margin hit 83%.

Palantir crushed expectations with $1.18 billion in quarterly revenue, $89 million above estimates. U.S. commercial revenue exploded 121% year-over-year to $397 million, while government revenue climbed 52% to $486 million. The company closed $2.76 billion in total contract value, up 151% from last year. CEO Alex Karp highlighted a Rule of 40 score of 114%. Adjusted operating margin reached 51%.

| Business Model | UiPath | Palantir |

| Core Function | AI agents execute tasks | AI analyzes data for decisions |

| Q3 Revenue Growth | 16% YoY | 63% YoY |

| Operating Margin | 3.2% (GAAP) | 33.3% |

| Key Metric | ARR: $1.78B | Contract value: $2.76B |

Platform Consolidation vs. Dual-Market Dominance

UiPath is betting enterprises will consolidate around unified automation platforms. The company integrated Microsoft Azure AI Foundry, launched a conversational agent with Google Gemini, and built a ChatGPT connector. Management projects Q4 revenue of $462 to $467 million with non-GAAP operating income around $140 million, implying a 30% operating margin.

Palantir’s advantage comes from serving two distinct markets with the same core platform. Government contracts provide stable, high-margin revenue while commercial deals accelerate faster. U.S. commercial growth of 121% suggests the AI Platform is breaking through enterprise adoption barriers. The company raised full-year revenue guidance to $4.40 billion, implying 53% growth, with U.S. commercial revenue expected to exceed $1.43 billion for 104% annual growth.

Profitability Paths Diverge Sharply

UiPath’s path to profitability required years of investment to reach breakeven. The company generated $28 million in operating cash flow during Q3, but GAAP operating margin remains just 3.2%. Non-GAAP operating margin of 21% shows the underlying unit economics once stock compensation adjusts out.

Palantir already operates at scale with 51% adjusted operating margins and $601 million in adjusted operating income on $1.18 billion in revenue. The company holds $6.4 billion in cash, up 733% year-over-year. Net income hit $477 million. This profitability gap explains the valuation premium, with Palantir trading at a forward P/E of 217 versus UiPath at 17.

Valuation Gap Reflects Different Risk-Reward Profiles

UiPath trades at a PEG ratio of 0.48 compared to Palantir’s 3.62, despite 60% earnings growth last quarter. Analysts revised earnings estimates upward 19 times in three months with zero downward revisions. The stock trades near $18 against analyst price targets suggesting potential upside if agentic automation adoption accelerates through 2026.

Palantir’s 111x price-to-sales ratio reflects its current execution and market expectations for continued growth. The valuation premium indicates the market has already priced in substantial future performance, while UiPath’s valuation suggests the market has not yet fully priced in potential agentic automation adoption through 2026.

Contact [email protected] for any questions or corrections.