A retiree who saved diligently and built a comfortable portfolio can face an unwelcome surprise at tax season: a bill far larger than expected. This happens when investment income combines with Social Security benefits in ways that trigger multiple tax consequences at once.

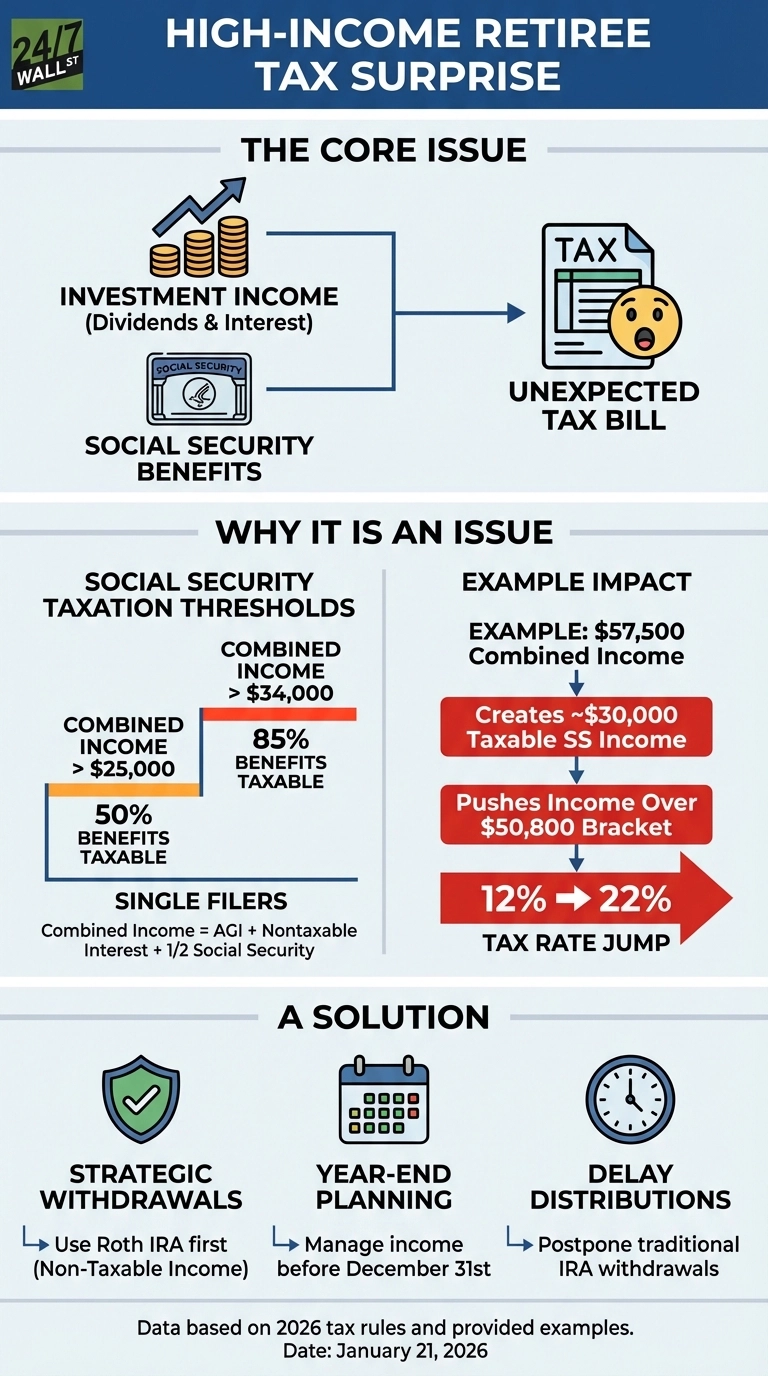

The core issue is how different income sources stack together. Dividend income from holdings like Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) or Vanguard High Dividend Yield ETF (NYSEARCA:VYM) can reach $20,000 to $30,000 annually, while bond interest adds another layer. Those amounts do not just get taxed on their own. They also determine whether Social Security benefits become taxable, creating a compounding effect that catches many retirees off guard.

When Portfolio Income Makes Social Security Taxable

Social Security taxation hinges on “combined income,” which is the sum of adjusted gross income, nontaxable interest, and half of Social Security benefits. The mechanism creates a compounding effect where portfolio withdrawals do not just face their own tax rates. They also activate taxation on benefits that would otherwise remain untaxed.

Cross certain thresholds and suddenly half or even 85% of benefits become taxable. For single filers, that first threshold sits at $25,000 in combined income, and the 85% tier kicks in above $34,000. For married couples filing jointly, the two cutoffs are $32,000 and $44,000. These numbers have been frozen by statute since 1983 and are not adjusted for inflation, which means more retirees drift into taxable territory every year. The 2026 Social Security cost-of-living adjustment of 2.8% increased monthly benefit payments and, by itself, pushed some recipients closer to the thresholds without any change in their other income.

Consider a retiree receiving $35,000 in Social Security who also collects $40,000 in dividends and interest. The tax code requires adding the investment income to half the Social Security benefits to arrive at combined income, which is then compared to the taxability thresholds.

In this scenario, combined income reaches $57,500, well past the 85% tier. The result adds roughly $30,000 to taxable income. That is money that would have been tax-free with a lower level of portfolio withdrawals, and there is no way to undo the calculation after December 31.

The Bracket Creep That Catches People Off Guard

The 2026 tax brackets create a compounding problem for retirees already in this position. A retiree who starts in the 12% bracket can find that taxable Social Security benefits push total income above $50,400, at which point the next dollars face the 22% rate. That bracket jump means the last slice of income is taxed at nearly double the rate the retiree expected, turning a comfortable withdrawal strategy into an unexpectedly expensive one.

Qualified dividends enjoy preferential 15% rates for most retirees, but this apparent advantage carries a hidden cost. That dividend income still counts in the combined income calculation and can trigger ordinary-rate taxation on Social Security benefits. The same income creates a second delayed consequence: Medicare Part B premiums are based on modified adjusted gross income from two years earlier. With the 2026 standard Part B premium at $202.90 per month and IRMAA surcharges beginning at $109,000 in income for single filers, a high-dividend year can raise Medicare costs well into the future, long after the portfolio year that caused the spike.

A New Deduction That May Help Some Retirees

Legislation enacted in 2025 introduced a temporary senior bonus deduction of $6,000 per qualifying individual age 65 or older, available for tax years 2025 through 2028. A married couple where both spouses are 65 or older can claim $12,000. The deduction reduces taxable income after the combined income test has already determined how much of Social Security is taxable, so it does not move the thresholds themselves. For lower- and middle-income retirees, though, the practical effect can be significant: a lower taxable income figure after the Social Security inclusion may keep a retiree in the 12% bracket even when some benefits are taxable.

How This Fits With Withdrawal Strategy

Understanding these interactions changes how retirees should approach tapping different accounts. Traditional IRA distributions add to adjusted gross income just like dividends do, and can trigger the same Social Security taxation cascade. Roth IRA withdrawals do not count toward combined income and will not affect Social Security taxation or Medicare premiums, making Roth accounts particularly valuable for managing the tax bill in retirement. Retirees who convert traditional IRA balances to Roth accounts before claiming Social Security can reduce their future combined income and the exposure that comes with it.

What to Think Through First

Calculate combined income before year-end. If you are close to a threshold, even small adjustments matter. Delaying an IRA distribution by a few weeks or trimming dividend-paying positions can keep combined income below the level where Social Security becomes taxable. Once that line is crossed, the tax impact escalates quickly, and nothing can reverse it once the calendar year closes. The same logic applies to IRMAA: income that looks manageable today can raise Medicare premiums two years from now, so retirement planning needs to account for that lag.

Editor’s note: This article was updated to correct the 2026 single-filer 22% bracket threshold from $50,800 to $50,400 per IRS Revenue Procedure 2025-32, and to add current context including the 2026 Social Security COLA of 2.8%, the frozen nature of the combined income thresholds since 1983, the new $6,000 temporary senior bonus deduction created by the One Big Beautiful Bill Act, and the 2026 Medicare Part B standard premium of $202.90 with IRMAA surcharges beginning at $109,000 for single filers.

Contact [email protected] for any questions or corrections.