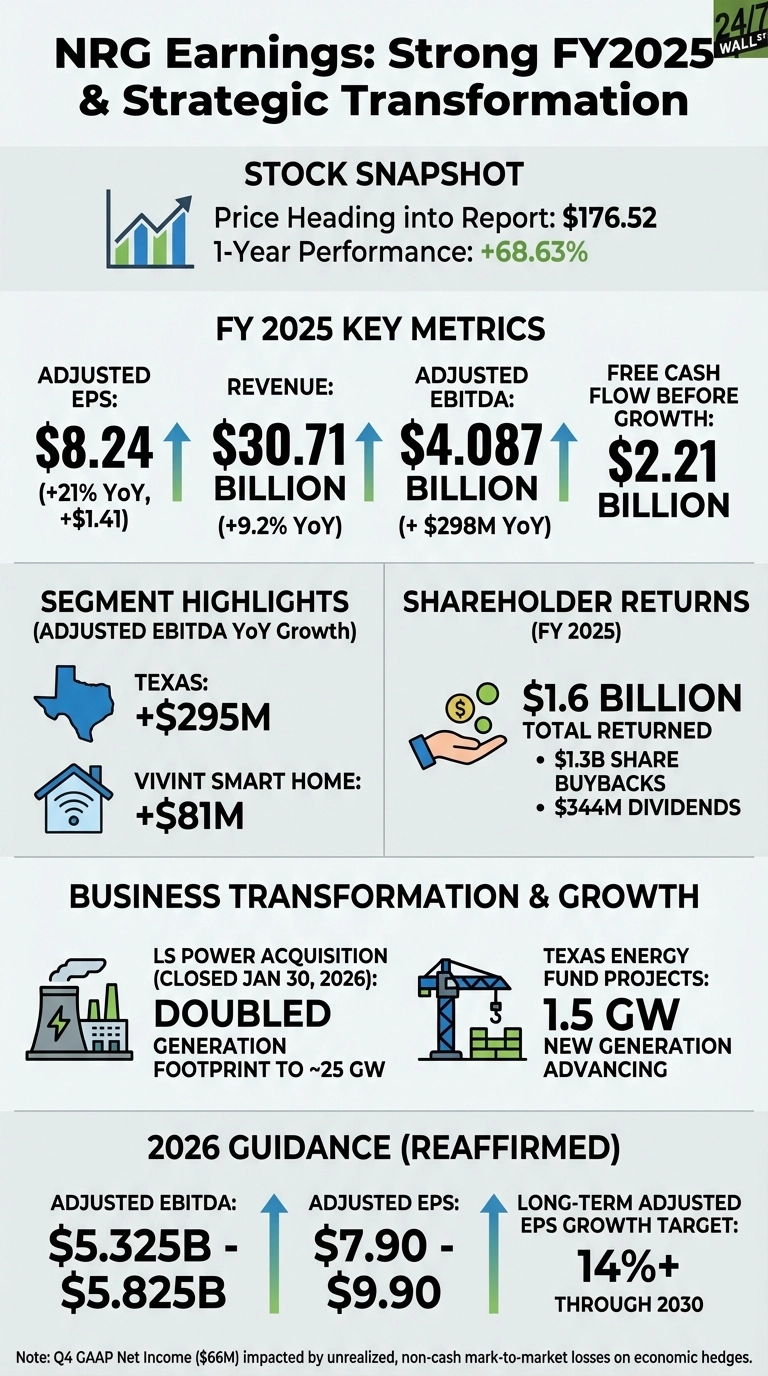

NRG Energy (NYSE:NRG) reported Q4 2025 earnings before the open this morning, posting a strong full-year performance headlined by a 21% jump in adjusted EPS. The stock was trading at $176.52 heading into the report, up nearly 69% over the past year. The headline numbers were solid, but the real story here is the transformation underway at NRG.

Texas Carries the Year

The Texas segment was the standout, with Adjusted EBITDA rising $295 million year over year through improved margins and supply cost optimization. Vivint Smart Home also contributed meaningfully, with Adjusted EBITDA up $81 million YoY on record new customer additions and strong retention. Full-year Adjusted EBITDA came in at $4.087 billion, up $298 million from the prior year. $2.21 billion in free cash flow before growth gives NRG flexibility heading into a heavy investment cycle.

GAAP Net Income Masks Adjusted Strength

The one number that looks jarring is GAAP net income. Q4 GAAP net income fell nearly 90% year over year to $66 million, and the full-year figure dropped as well. This is almost entirely a product of unrealized, non-cash mark-to-market losses on economic hedges. It doesn’t reflect the operating business. That said, the East segment did post a $25 million YoY decline in Adjusted EBITDA due to higher retail costs and the retirement of the Indian River facility. Not alarming, but worth keeping an eye on.

The Numbers Reflect a Business in Transition

Key Figures (Full Year 2025)

- Adjusted EPS: $8.24, up $1.41 YoY (+21%)

- Revenue: $30.71 billion, up 9.2% YoY

- Adjusted EBITDA: $4.087 billion, up $298 million YoY

- FCF before Growth: $2.21 billion

- Q4 Revenue: $7.76 billion, up ~14% YoY

- Q4 Adjusted EPS: $1.04

- Shareholder Returns: $1.6 billion total ($1.3B buybacks + $344M dividends)

The share count reduction of 11 million weighted average basic shares was a quiet but meaningful contributor to EPS growth.

CEO Sees a Power Demand Supercycle

CEO Larry Coben sounded confident and expansive. “We’ve doubled our generation footprint, advanced 1.5 GW of new generation through three Texas Energy Fund projects, and expanded our demand response and residential VPP capabilities,” he said. He pointed directly to data centers as a growth driver, citing NRG’s “bring your own power” strategy for hyperscalers. The tone was bullish, and it was grounded in specific capacity milestones rather than vague optimism.

2026 Guidance Points Higher, With One Caveat

NRG reaffirmed 2026 guidance that reflects the January 30 close of the LS Power acquisition, which doubled generation capacity to roughly 25 GW. The company is targeting Adjusted EBITDA of $5.325 billion to $5.825 billion and Adjusted EPS of $7.90 to $9.90. The long-term EPS growth target of 14%+ through 2030 is ambitious. The caveat is $4.9 billion in new debt used to finance the acquisition, which will weigh on interest expense. How quickly integration synergies materialize will be a key factor in offsetting that added interest expense burden.