Sandisk (NASDAQ:SNDK | SNDK Price Prediction) stock is down 8% in Thursday trading, with shares falling to around $623. Meanwhile, Micron Technology (NASDAQ:MU) stock is sliding roughly 5% to near $364, extending a brutal week for the memory sector.

Both stocks have been under pressure all week. Sandisk stock has dropped 18% over the past five trading days, while Micron stock has also shed 18%. The selling comes even as both companies posted strong recent earnings and carry bullish analyst ratings, raising a pointed question: is the market seeing something Wall Street is not?

Several headwinds are converging. Google’s TurboQuant algorithm, which reduces key-value cache memory size by at least 6x without sacrificing accuracy, has raised concerns that AI workloads may require less memory than previously assumed. Today’s selling reflects investors weighing that structural risk against an analyst community pushing back hard.

Google’s Compression Threat Meets an Analyst Defense

The TurboQuant concern continues to weigh on sentiment across the memory space. Analysts defending the sector argue the risk is speculative and long-term. Their core argument: memory supply shortages are intensifying rather than easing, and customers are prepaying for large memory deals, a behavior that signals genuine forward demand conviction.

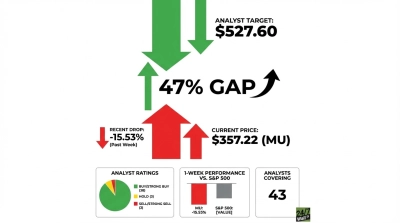

The analyst consensus on Micron stock reflects that confidence. 38 analysts rate the stock a buy or strong buy, against just 2 sells and 3 holds. The average price target sits at $525, well above where shares trade today. As for Sandisk stock, 14 analysts carry buy or strong buy ratings with zero sells, and the consensus target is $770, roughly 23% above current prices.

Micron CEO Sanjay Mehrotra has been direct about the company’s positioning, describing Micron as an essential AI enabler with order books stretching into 2027. That visibility is exactly what analysts point to when arguing the TurboQuant narrative is overblown near term.

Sandisk’s Nanya Bet Adds a Capital Allocation Overhang

Sandisk carries additional weight today. The company recently committed $1 billion to acquire a minority stake of just under 4% in Nanya Technology, a Taiwanese DRAM supplier, as part of a broader $2.5 billion consortium investment. The strategic logic is sound: securing DRAM supply in a shortage environment. Yet, investors appear skeptical about the price tag and timing.

Sandisk’s free cash flow came in at $980 million in Q2 fiscal 2026, a dramatic improvement. Deploying nearly that entire quarterly free cash flow into a minority stake in a Taiwanese supplier, when trade policy and tariff risks are elevated, invites second-guessing. SNDK stock’s year-to-date gain of nearly 186% means there is plenty of profit-taking fuel for investors looking for an exit.

Micron’s Week of Volatility Continues

Micron’s situation is distinct but parallel. The company’s most recent earnings revealed elevated capital expenditure guidance alongside a debt repurchase tender offer, details that have kept the stock volatile all week. Despite a 307% gain over the past year, MU stock has pulled back sharply from recent highs as investors recalibrate expectations.

The forward valuation tells an interesting story. Micron trades at a forward price-to-earnings ratio of roughly 8x, with a PEG ratio of 0.3. A PEG ratio that low, relative to earnings growth, is what keeps analysts bullish even as the stock sells off.

The bear case is real, though. SK Hynix is reportedly considering a potential $14 billion U.S. listing that would add competitive supply pressure to a market where Micron and Sandisk currently benefit from constrained competition.

Why Analysts Are Holding Firm

The bull case rests on structural demand. AI infrastructure requires enormous amounts of memory, shortages are real, and customers prepaying for future supply do not behave like buyers who expect demand to evaporate.

Micron’s cloud memory business generated $5.284 billion in revenue at 66% gross margins last quarter. Sandisk guided for Q3 revenue of $4.40 billion to $4.80 billion with gross margins of 65% to 67%. A sector with those margins and that revenue trajectory has real forward momentum.

The bear case is a convergence of risks arriving simultaneously: TurboQuant’s long-term demand implications, SK Hynix’s potential U.S. listing, Sandisk’s capital-intensive Nanya bet, and Micron’s elevated capex commitments. None of these individually should tank SNDK and MU stocks.

Together, however, they create enough uncertainty to keep sellers active. Whether analysts or the market has the better read on the memory sector’s next 12 months will likely become clear as AI infrastructure spending data rolls in through the rest of 2026.