Tech workers who receive restricted stock units face an income recognition problem that most financial planning frameworks underestimate. RSUs vest as ordinary income at the full market value on the vesting date, regardless of whether the worker sells a single share. That income stacks on top of a base salary already sitting in the upper brackets. For workers at large technology companies, vesting years routinely push total compensation into the 37% bracket.

The second layer arrives in retirement. A tech worker who spent two decades maximizing a traditional 401(k) accumulates a large pre-tax balance. When required minimum distributions begin, those withdrawals are hit as ordinary income. The combination means two layers of ordinary income (RSU income during peak earning years and RMD income in retirement), potentially stacking into the 37% bracket in both phases, never experiencing a lower-tax window.

The mathematically correct response for many workers is to maximize traditional 401(k) contributions during RSU vesting years to partially offset that income, then execute Roth conversions during any sabbatical, layoff, or early retirement window before RMDs begin. The question then becomes where to hold assets outside the 401(k) and how to structure those holdings to minimize tax drag during vesting years. That is where ETF selection matters.

One clarification before the funds: tech workers with significant company stock should evaluate the Net Unrealized Appreciation (NUA) strategy if those shares are held within the company’s 401(k) plan. While many assume NUA applies to any employer stock, it is exclusively available for shares distributed directly from a qualified plan, not for typical RSUs that vest into a standard brokerage account. This distinction is a frequent source of confusion. Because most RSUs are treated as retired upon vesting, they are ineligible for NUA’s favorable capital gains treatment. Workers who do happen to hold employer stock inside their 401(k) must be extremely careful; rolling that balance into an IRA before considering NUA effectively destroys the tax benefit forever.

Vanguard Total Stock Market ETF: The Core Taxable Account Holding

Vanguard Total Stock Market Index Fund ETF Shares (NYSEARCA:VTI) is the default holding for tech workers building wealth in a taxable brokerage account during high-income years. VTI owns the entire U.S. equity market essentially in a single fund, with a net expense ratio of 0.03% and a portfolio turnover rate of 3%. Low turnover means the fund rarely realizes and distributes capital gains, which would otherwise create a taxable event in the year of distribution.

For a worker already facing a large ordinary income event from RSU vesting, avoiding additional capital gains distributions in a taxable account matters. VTI’s ETF share class structure also gives it an advantage in managing capital gains at the fund level. The fund holds roughly $2.1 trillion in net assets, making it one of the most liquid instruments available.

The tradeoff is concentration in technology. Information technology represents about 32% of the fund’s weight, with top holdings including the same mega-cap names that dominate many tech workers’ RSU grants. A worker with large unvested RSUs in a large technology company who also holds VTI is adding correlated exposure. That concentration risk does not disqualify VTI as a taxable account holding, but it is worth acknowledging.

Schwab U.S. Broad Market ETF: The Tax-Loss Harvesting Pair

Schwab U.S. Broad Market ETF (NYSEARCA:SCHB) is the natural tax-loss harvesting partner for VTI. During RSU vesting years, when a tech worker is already generating large ordinary income, harvesting capital losses in a taxable account can offset all capital gains plus up to $3,000 of that high-tax ordinary income. SCHB carries a net expense ratio of 0.03% and a portfolio turnover rate that has recently hovered around 2%, ensuring the economic cost of switching remains negligible.

The wash-sale rule prevents an investor from selling a security at a loss and buying it back within 30 days. VTI tracks the CRSP US Total Market Index while SCHB tracks the Dow Jones U.S. Broad Stock Market Index, which means selling VTI at a loss and immediately buying SCHB maintains near-identical market exposure without triggering a wash sale. SCHB carries a net expense ratio of 0.03% and the same 3% portfolio turnover as VTI, so the economic cost of switching is negligible.

This strategy only matters in years when a taxable account position has unrealized losses. The value of holding SCHB as a designated pair is that the infrastructure exists to act quickly when a market decline creates harvesting opportunities. The tradeoff is that two nearly identical funds add minor complexity to portfolio tracking.

iShares Core S&P Total U.S. Stock Market ETF: A Third Leg for Active Harvesting

iShares Core S&P Total U.S. Stock Market ETF (NYSEARCA:ITOT) adds a third layer for workers who want to cycle through tax-loss harvesting positions without sitting in cash or triggering wash sales. ITOT tracks the S&P Total Market Index, which is distinct from both the CRSP index (VTI) and the Dow Jones index (SCHB). A worker who has already harvested losses by moving from VTI to SCHB can later harvest again by swapping SCHB for ITOT, maintaining continuous market exposure throughout the 30-day wash-sale window.

ITOT holds approximately $82 billion in net assets, carries a 0.03% expense ratio, and maintains a portfolio turnover rate of approximately 3%. Its sector composition mirrors VTI closely, with information technology representing about 31% of the portfolio—a slightly lower tech concentration than the broader CRSP index. ITOT serves primarily as a harvesting destination rather than a unique investment thesis. For workers not actively seeking to bank capital losses, holding all three funds is unnecessary; however, for those in the 37% bracket, it is a powerful tool for maintaining a “tax-ready” portfolio.

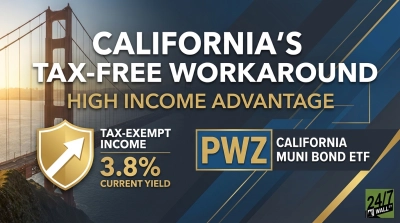

Vanguard Tax-Exempt Bond ETF: Tax-Free Income for High-Bracket Years

Vanguard Tax-Exempt Bond ETF (NYSEARCA:VTEB) addresses a different part of the problem. During peak RSU vesting years, any bond allocation held in a taxable account should generate income that does not add to an already elevated ordinary income tax bill. Municipal bond interest is exempt from federal income tax, making VTEB’s income stream effectively invisible to the IRS for most investors.

The fund holds investment-grade municipal bonds across various states, with approximately $45 billion in net assets and a 0.03% expense ratio. The 30-day SEC yield currently runs near 3.5% on a tax-exempt basis. For a worker in the 37% federal bracket, a 3.5% tax-exempt yield delivers significantly more in after-tax terms than a comparable taxable yield. The precise advantage depends on state taxes, but the after-tax “alpha” is undeniable for high-income earners in states like California or New York.

The tradeoff is interest rate sensitivity. Municipal bond funds lose value when rates rise, and the 10-year Treasury yield currently sits near 4.34%, at roughly the 75th percentile of its recent range. Workers approaching a Roth conversion window who need stable assets to fund the tax payment should hold shorter-duration instruments rather than VTEB’s intermediate-term profile.

Matching Funds to the Situation

VTI belongs in almost every tech worker’s taxable account as the primary equity holding. Its low turnover and minimal distributions suit high-income years well. SCHB and ITOT are harvesting infrastructure rather than independent positions: workers running an active tax-loss-harvesting program should hold all three in rotation, while workers who do not actively harvest losses need only VTI. VTEB suits workers who hold a bond allocation in taxable accounts and are in a high enough bracket that tax-exempt income offers a clear advantage over taxable bond alternatives. Workers whose bond allocation sits entirely in tax-deferred accounts have no use for VTEB.