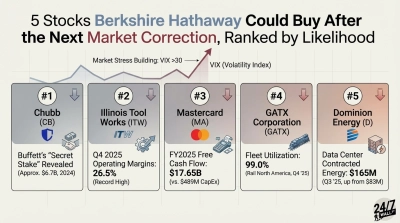

Berkshire Hathaway rarely adds to a position unless management sees meaningful upside ahead, which is why investors tend to closely watch every move the conglomerate makes.

Recent filings show Berkshire increasing positions in the New York Times, Chevron, Chubb, and Domino’s Pizza, signaling growing conviction in four very different businesses across media, energy, insurance, and consumer spending.

Perhaps more importantly for investors, several of these stocks still appear attractively positioned today, offering insight into where one of the world’s most successful investing firms may continue to see value despite a market trading near historic highs.

New York Times Could Be Berkshire’s Surprise New Compounder

The most attention-grabbing move was Berkshire’s first-ever stake in the New York Times (NYSE:NYT). The firm disclosed ownership of 5,065,744 shares worth roughly $351.7 million at year-end 2025, marking Berkshire’s return to media investing after exiting its newspaper portfolio in 2020.

What Berkshire appears to like is that The New York Times has transformed into a modern subscription-driven digital business rather than a legacy newspaper operator. The company ended 2025 with 12.78 million digital-only subscribers after adding approximately 450,000 net digital subscribers in Q4 alone.

That subscriber growth is translating directly into stronger financial results. Digital-only subscription revenue rose 13.9% year over year to $381.5 million in Q4, while digital advertising jumped 24.9% to $147.2 million. Full-year free cash flow climbed 44.4% to $550.5 million.

CEO Meredith Kopit Levien recently said management expects “another year of healthy growth in subscribers, revenue, and profitability,” reinforcing the view that the company’s momentum remains intact. The stock is not cheap, trading at roughly 38 times trailing earnings and 29 times forward earnings, but Berkshire’s purchase suggests the firm believes the market may still be underestimating the long-term durability of the business. Shares have climbed 67% over the past year.

Chevron Remains Berkshire’s Big Energy Conviction

Chevron (NYSE:CVX | CVX Price Prediction) has long been one of Berkshire’s highest-conviction energy holdings, and the company added to that position again in Q4 2025. Berkshire increased its stake from 122.1 million shares to 130.2 million shares during the quarter, signaling continued confidence despite broader concerns around oil prices and energy-sector volatility.

Operationally, Chevron continues to execute well. Full-year production reached a record 3,723 MBOED, up 12% year over year, while the Permian Basin surpassed its target of 1 million barrels of oil equivalent per day. The company also generated record operating cash flow of $33.9 billion during 2025 and returned $27.1 billion to shareholders through dividends and buybacks.

Chevron’s dividend was recently raised 4% to $1.78 per quarter, marking the company’s 39th consecutive annual dividend increase. Shares currently yield 3.59%, and management continues targeting $3 billion to $4 billion in structural cost savings by the end of 2026. Chevron stock has jumped 46% over the past year.

Chubb Strengthens Berkshire’s Insurance Empire

Berkshire also deepened its position in Chubb (NYSE:CB), increasing its stake from 31.3 million shares to 34.3 million shares in Q4. The move adds to Berkshire’s already significant insurance exposure and gives the conglomerate a larger stake in one of the highest-quality property and casualty insurers in the public markets.

Chubb’s recent operating performance helps explain Berkshire’s growing interest. The company posted a record property and casualty combined ratio of 81.2% in Q4 2025, improving from 85.7% a year earlier and signaling elite underwriting discipline. Net premiums written increased 8.9% to $13.13 billion, while quarterly net income rose 24.7% year over year to $3.21 billion. Core operating EPS came in at $7.52, well above analyst expectations of $6.78.

CEO Evan Greenberg said he expects “excellent” results in 2026, including strong operating earnings growth and double-digit expansion in both EPS and tangible book value. Despite that performance, Chubb trades at just 13 times trailing earnings and 12 times forward earnings, a relatively modest valuation for a business producing this level of profitability. Shares are up 17.65% over the past year.

Domino’s Looks Like Berkshire’s Consumer Value Play

Berkshire also increased its position in Domino’s Pizza (NASDAQ:DPZ), bringing its stake to roughly 3.4 million shares. The move caught attention among retail investors because Berkshire appears to be buying into recent weakness. Domino’s remains the only one of Berkshire’s recent major purchases trading below its reported entry price.

Fundamentally, the business continues to perform well. Domino’s generated $671.5 million in free cash flow during fiscal 2025, up 31.2% year over year. U.S. same-store sales accelerated to 3.7% growth in Q4, up sharply from 0.4% in the prior-year period, while the company added 776 net new stores globally during the year. Management also raised the quarterly dividend 15% to $1.99 per share, continuing Domino’s long track record of returning capital to shareholders.

Shares trade at roughly 18 times forward earnings, while analyst consensus targets imply upside toward $475.74 versus the current price near $363.63. After falling 17.87% over the past year, Berkshire may view Domino’s as a temporarily discounted compounder with improving momentum.