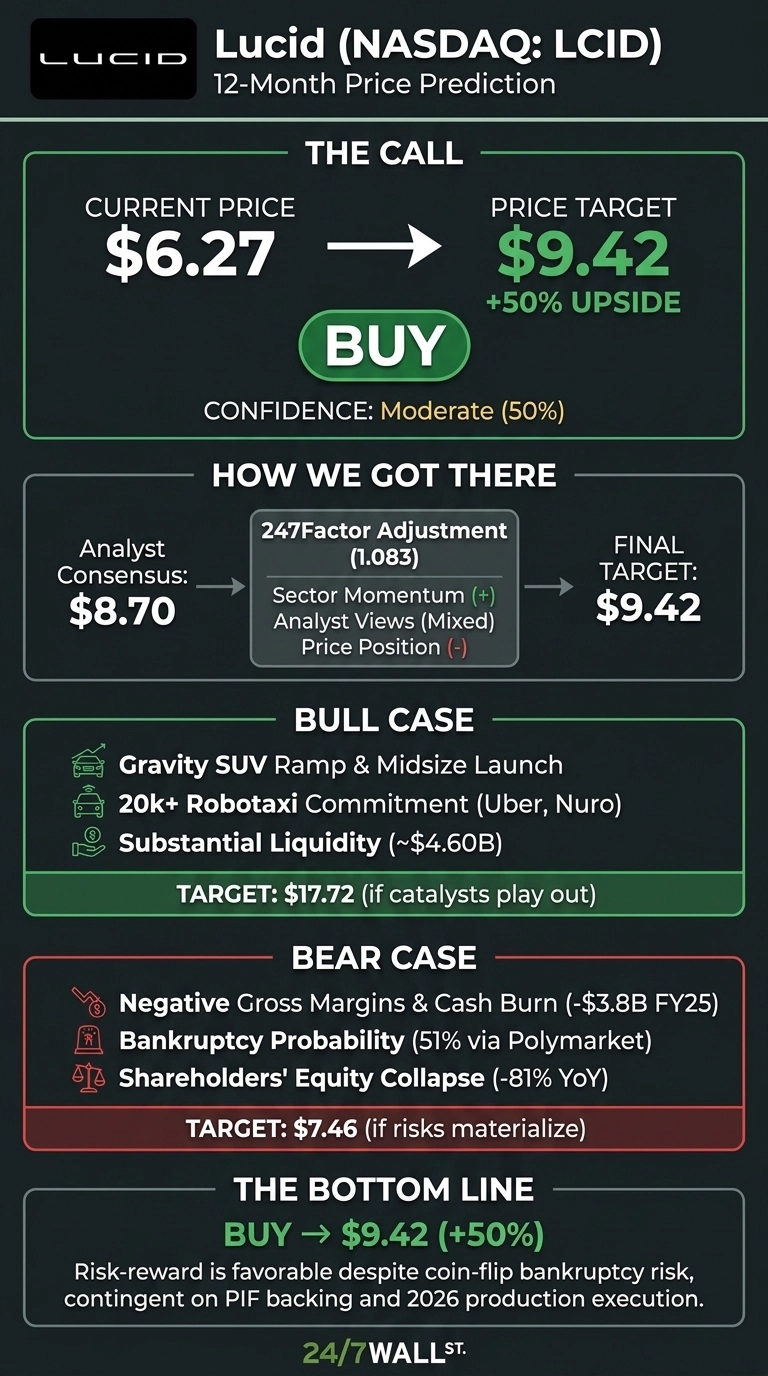

Few stocks divide investors like Lucid (NASDAQ:LCID | LCID Price Prediction). The luxury EV maker has the technology, partnerships, and Saudi backing. It also has deeply negative gross margins and a Polymarket bankruptcy market trading near a coin flip. When our model points to upside, it deserves careful framing.

Our 24/7 Wall St. price target for Lucid is $9.42 over the next 12 months, implying roughly 50.27% upside from the recent $6.27 close. Our recommendation is buy, with moderate confidence of 50%. This is a high-variance setup, and the price target reflects a base case rather than a slam-dunk thesis.

| Metric | Value |

|---|---|

| Current Price | $6.27 |

| 24/7 Wall St. Price Target | $9.42 |

| Upside | 50.27% |

| Recommendation | BUY |

| Confidence | 50% (moderate) |

A Brutal Year, and Why the Setup Has Changed

Lucid shares are down 77.28% over the past year and 40.68% year to date, trading roughly 74% below the 52-week high of $33.70.

Q4 2025, reported February 24, delivered $522.73M in revenue, up 122.39% year over year and beating consensus by 10.78%. Vehicle deliveries hit 5,345 units, up 72%. Non-GAAP EPS came in at -$3.08, missing consensus by 42.81%. For 2026, management guided production to 25,000 to 27,000 vehicles, with the Midsize launch and first commercial robotaxi deployments on deck.

Why Bulls See a Path to $17

The bull thesis hinges on three catalysts. First, the Gravity SUV ramp and Midsize launch push 2026 volume meaningfully higher. Second, the robotaxi opportunity: the Uber and Nuro partnership commits to a minimum of 20,000 Lucid Gravity vehicles with Level 4 autonomy, plus a strategic Uber investment and NVIDIA collaboration for autonomous driving.

Third, liquidity remains substantial, with roughly $4.60 billion in total liquidity after PIF expanded its term loan facility. Our bull case scenario points to $17.72 over 12 months, a 182.54% return if execution holds. Of the analyst panel, 2 rate the stock Buy.

What Could Go Wrong

The bear case is real. Cost of revenue of $944.64M in Q4 exceeded revenue, and full-year free cash flow was -$3.80 billion. Shareholders’ equity collapsed 81.48% in a year. Polymarket’s bankruptcy market sits at 51% probability before 2027, and dilution overhang from up to 69.1 million registered shares is material.

Of analyst ratings, 3 sit at Sell or Strong Sell. Bulls argue the EPS miss and cash burn reflect heavy investment in the Gravity ramp, Saudi AMP-2 facility, and robotaxi engineering fleet. Revenue grew triple digits in Q4. Our bear case still implies $7.46, an 18.93% return, because the stock has already absorbed extraordinary punishment.

Risk-Reward and What to Watch

The 24/7 Wall St. price target of $9.42 and buy recommendation reflect a view that the risk-reward at $6.27 has skewed favorable, even with a coin-flip bankruptcy market. The tipping factor is continued PIF backing and a 2026 production guide that, if hit, materially shrinks the cash-burn gap.

The setup looks constructive if Gravity deliveries stay on the 25,000 plus path and the Midsize launches on schedule. The thesis weakens if PIF support softens or Q1 free cash flow comes in worse than Q4’s -$1.24 billion.

Looking ahead, here is where our model projects Lucid could trade, assuming the Gravity ramp succeeds and the robotaxi business scales.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $9.42 |

| 2027 | $11.26 |

| 2028 | $13.45 |

| 2029 | $16.08 |

| 2030 | $19.21 |

These projections assume Lucid executes on its production ramp and reaches positive gross margins by the back half of the decade. Significant upside or downside could come from robotaxi commercialization or disruption to PIF financing.

Contact [email protected] for any questions or corrections.