Adobe (NASDAQ:ADBE | ADBE Price Prediction) has been one of the most punished large-cap software names of 2026, and that selloff is exactly where our model finds opportunity. After a brutal 27.61% year-to-date decline, the stock now trades well below where the fundamentals suggest it should.

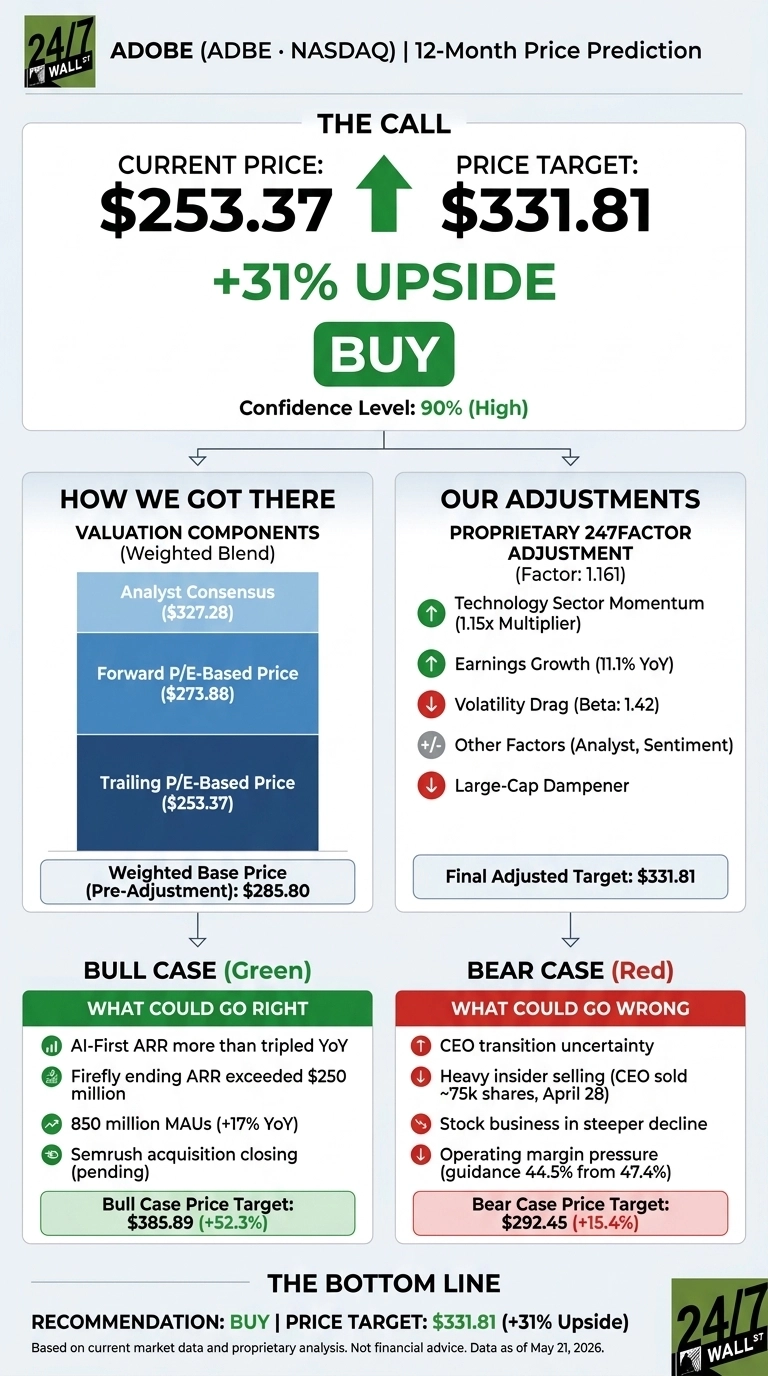

Our 24/7 Wall St. price target for Adobe is $331.81, implying roughly 31% upside from current levels over the next 12 months. The recommendation is buy, with a high model confidence reading of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $253.37 |

| 24/7 Wall St. Price Target | $331.81 |

| Upside | 30.96% |

| Recommendation | BUY |

| Confidence Level | 90% |

How a $400 Stock Became a $250 Stock

Adobe was a $417 stock a year ago. It is now $253.37, down 39.33% over 12 months and 22% below its $421.48 52-week high.

The carnage came despite four straight earnings beats. Q1 FY2026, reported March 12, 2026, delivered revenue of $6.40 billion (+12.0% YoY) and non-GAAP EPS of $6.06, ahead of the $5.87 consensus. Yet the stock fell 7.58% on the report as CEO Shantanu Narayen announced his transition after 18 years at the helm. The pending Semrush acquisition and AI competition narrative have kept sellers in control. Encouragingly, ADBE has rallied 7.33% over the past week.

Our Proprietary Model Points to $331.81

The 24/7 Wall St. price target blends three valuation anchors. The trailing P/E based price comes in at $253.37, the forward P/E based price at $273.88, and the analyst consensus target weights in at $327.28. That weighted blend produces a pre-adjustment value of $285.80.

The Case for $385 and Above

Our bull scenario sees ADBE reaching $385.89, a 52.3% total return. The driver is AI monetization translating from usage to revenue. AI-first ARR more than tripled year over year in Q1, Firefly ending ARR exceeded $250 million, and the Adobe ecosystem now boasts 850 million monthly active users, growing 17% YoY.

With a forward P/E of just 11 and a PEG ratio of 0.724, the multiple compression has gone too far. Of 39 analysts, 16 rate ADBE Buy or Strong Buy, with a consensus target of $327.28. The Semrush acquisition closing in Q2 would add brand visibility capabilities not yet baked into guidance.

What Could Push ADBE Back to $225

The bear scenario from our model targets $292.45, still above today’s price, but the real downside risk centers on execution. CEO succession is unresolved. Insider activity has skewed heavily toward selling, with Narayen disposing of roughly 75,000 shares on April 28 at $243 to $245.

Adobe’s stock photography business is in steeper decline than expected, a roughly $450 million segment under pressure from generative AI. Q2 guidance implies non-GAAP operating margin slipping to 44.5% from 47.4%.

Bulls would counter that margin compression reflects deliberate reinvestment into Firefly, GenStudio, and freemium funnels, with management explicitly acknowledging this dampens ARR in the short term but builds the monetization base.

Why the Risk/Reward Looks Compelling Here

At 11x forward earnings with a 29.5% profit margin, 58.8% return on equity, and AI-first ARR tripling, I think the market has overcorrected. The 24/7 Wall St. price target stays at $331.81, a buy with 90% confidence. The bull case rests on whether Adobe can convert its 850 million MAU funnel into paying subscribers over the next 18 months.

The bear case rests on whether the CEO transition triggers strategic drift, or AI native competitors capture the SMB creative market faster than Adobe can defend it. The valuation reset has done the hard work for new buyers.

Adobe Price Prediction 2026 to 2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $331.81 |

| 2027 | $378 |

| 2028 | $432 |

| 2029 | $487 |

| 2030 | $548.32 |

These projections assume Adobe sustains roughly 16.7% annualized base-case returns, in line with its 5-year model trajectory. Material upside or downside could come from Semrush integration outcomes, the CEO succession choice, and how aggressively OpenAI, Google, and Microsoft monetize competing creative tools.

Contact [email protected] for any questions or corrections.