The Nasdaq has whipsawed retail investors in 2026, and nowhere has the volatility been more brutal than in beaten-down names trading under $20. Short-seller reports, foreign exchange noise, and headline-driven panic have left genuine category leaders priced like distressed assets. For investors willing to look past the noise, sub-$20 tickers attached to monopoly-style business models are where the asymmetric setups live right now.

With that in mind, here is one stock trading under $20 that owns a near-monopoly on global sports data infrastructure, with management buying hand over fist after a brutal drawdown.

Sportradar (NASDAQ: SRAD)

Sportradar (NASDAQ:SRAD) is the Swiss-based scaled leader in the global sports data ecosystem, supplying betting, gaming, media, and integrity services to sportsbooks, leagues, and broadcasters worldwide.

Shares trade under $14 following a period of downward movement in 2026, down 43.92% year-to-date and 23.43% over the past month. For a retail investor scanning under-$20 tech names, the entry sits well below the 52-week high of $32.22 and just above the $11.66 low.

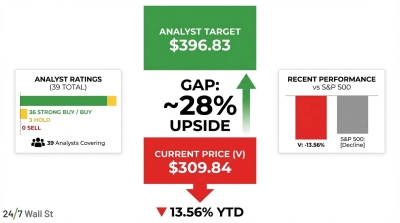

Fundamentals back the contrarian setup. Market cap sits near $3.93 billion on TTM revenue of $1.33 billion, with an EV/EBITDA of just 6 and a forward P/E of 31. The Street consensus target of $21.25 implies meaningful upside from current levels, and the analyst board reads 3 Strong Buy, 15 Buy, 3 Hold, with zero sells.

The bull case is straightforward. Sportradar holds exclusive multi-year global data rights for the NBA, NHL, and major sports betting structures worldwide, and management reiterated FY2026 constant-currency revenue growth of 23% to 25% alongside adjusted EBITDA growth of 34% to 37%. CFO Craig Felenstein told investors “our revenue growth in the first quarter would have been 16% on a constant currency basis, excluding the impact of FX movements.” The reported 11.34% Q1 growth understates the underlying business because of a $9.28M FX loss on USD-denominated sports rights, the kind of accounting noise that Wall Street routinely overweights in the short term.

The moat keeps widening. Sportradar covers over one million matches annually, expects to stream over 700,000 matches in 2026, and posted a customer net retention rate of 108%. The IMG ARENA acquisition is tracking ahead of plan, with management “fully anticipat[ing] exceeding the 25% synergy target”, and Integrity Services revenue jumped 81% year over year.

Capital allocation reinforces the conviction. The board authorized a $250 million enhanced open-market repurchase program on April 28, 2026, on top of the original $1 billion authorization. CEO Carsten Koerl said “I believe the company’s current valuation does not reflect the strength of our business and our long-term prospects” and committed to personally buying $10 million worth of shares. Form 4 filings confirm follow-through: Koerl purchased roughly 651,000 shares between late April and early May 2026, with multiple directors also buying in the open market.

However, a Muddy Waters research report on April 22, 2026 alleged exposure to illegal gambling markets, triggering a 22% single-day decline and a wave of securities class actions with a July 17, 2026 lead plaintiff deadline. Management has pushed back, with Koerl quantifying gray-market exposure in the low- to mid-single-digit range of revenue, but litigation overhang will linger. That risk is the reason shares trade where they do, and it does not override a near-monopoly position with accelerating margins.

For investors hunting infrastructure-grade compounders under $20, Sportradar checks the boxes: scaled leadership, double-digit constant-currency growth, expanding free cash flow, and aggressive insider buying into the drawdown.

A low share price is never a thesis on its own. Sub-$20 tickers carry real risk, particularly when active litigation and FX volatility are in the mix, and the right move is to study the filings, weigh the legal overhang, and size positions accordingly before acting on any name covered here.

Contact [email protected] for any questions or corrections.