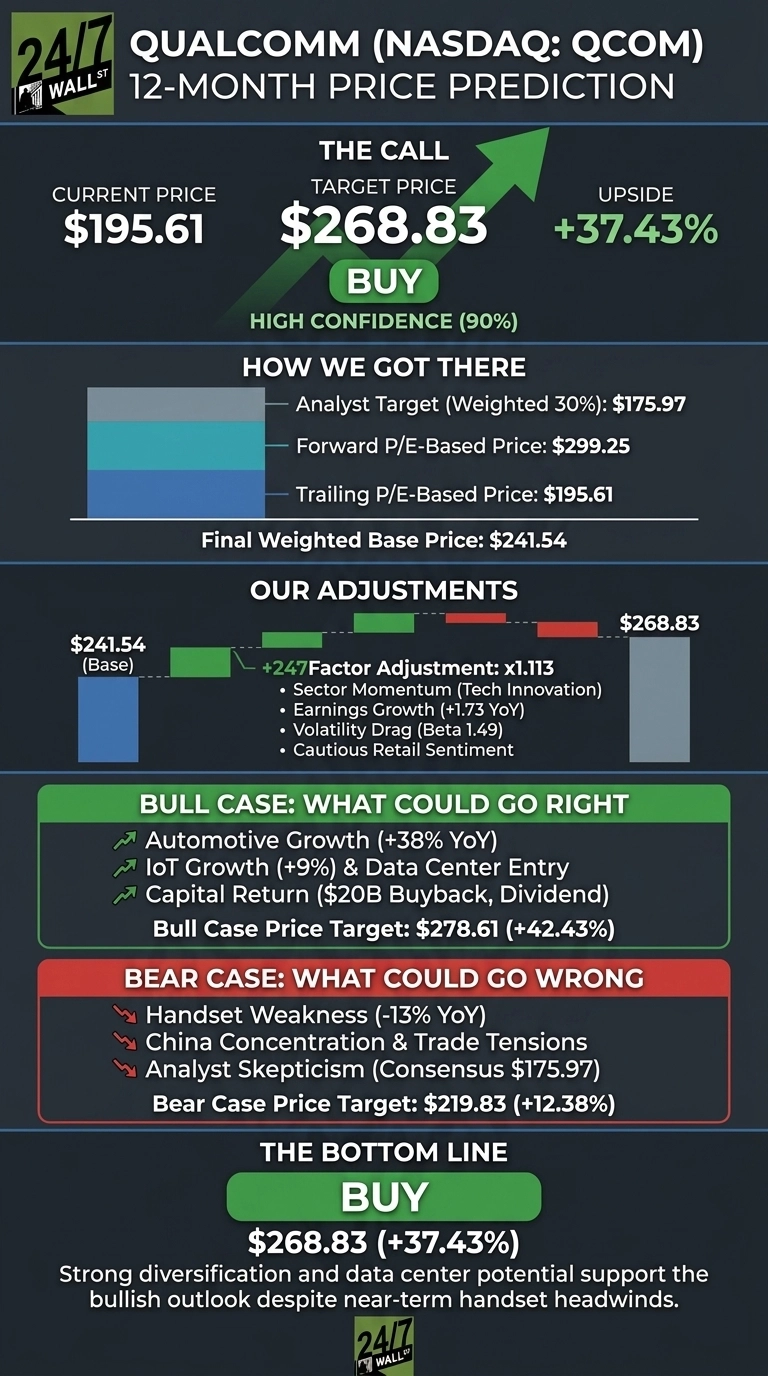

Qualcomm (NASDAQ:QCOM | QCOM Price Prediction) has staged a remarkable comeback, recovering 51.2% from its March low of $129.39 to today’s level near $195. The question now is whether the rally has legs or has run ahead of fundamentals. Our proprietary model says it still has room to run.

The 24/7 Wall St. price target for Qualcomm is $268.83 over the next 12 months, implying 37.43% upside from $195.61. Our model carries a 90% confidence level on this target, reflecting the data center and automotive growth thesis.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $195.61 |

| 24/7 Wall St. Price Target | $268.83 |

| Upside | 37.43% |

| Model Outlook | Bullish |

| Confidence Level | 90% |

A Sharp Rebound Backed by Real Catalysts

Qualcomm is up 43.62% over the past month and 30.25% over the past year, though shares pulled back 6.99% last week and sit 29% below the 52-week high of $247.90. Q2 FY26 results, reported in late April, beat on both lines: revenue of $10.60 billion and non-GAAP EPS of $2.65 against a $2.56 consensus.

The headline metric was the diversification story. Automotive revenue hit a record $1.33 billion (+38% YoY), IoT grew 9%, and handsets fell 13% on memory supply constraints across Chinese OEMs. CEO Cristiano Amon also confirmed that the company’s “leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year.”

The Case for $278 and Higher

Bulls argue the forward P/E of 19x on a company posting 38% automotive growth is too cheap. The Alphawave Semi acquisition, completed in Q1 FY26, opens the data center TAM, and the June 24 Investor Day on Data Center and Physical AI could be a re-rating catalyst.

Our bull case scenario projects $278.61 within 12 months, a 42.43% return. A new $20 billion buyback authorization plus the $0.89 quarterly dividend reinforces the capital return story.

The Risks Worth Watching

The consensus Wall Street analyst target sits at just $175.97, well below our target and current price, with 22 hold ratings versus 11 buys. Bears point to handset weakness, China concentration, and the risk Apple completes its modem in-sourcing.

Operating income fell 26% YoY in Q2, and Q3 guidance of $9.2 to $10 billion revenue implies further softness. Bulls would counter that the operating income drop reflects heavy R&D investment in data center and physical AI platforms, areas with multi-year payoff profiles. Our bear case lands at $219.83, still a 12.38% gain.

The Bottom Line

Our 24/7 Wall St. price target of $268.83 reflects high confidence (90%) that Qualcomm’s diversification beyond handsets is real and that the hyperscaler silicon engagement is a credible new revenue pillar.

The thesis strengthens if the June 24 Investor Day delivers a quantified data center roadmap. It weakens if the Q3 results show handset weakness deepening beyond guidance.

Looking further ahead, here is where our model projects Qualcomm could trade in the coming years, assuming current growth trajectories and capital return policy hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $268.83 |

| 2027 | $312 |

| 2028 | $365 |

| 2029 | $420 |

| 2030 | $477 |

These projections assume Qualcomm executes on its fiscal 2029 revenue goals and that data center custom silicon scales meaningfully. Significant upside or downside could result from the trajectory of Apple modem in-sourcing and the pace of AI inferencing migrating to edge devices.