Target (NYSE:TGT | TGT Price Prediction | TGT Price Prediction) delivered the quarter bears said it couldn’t. Comparable sales jumped 5.6% on 4.4% traffic growth, digital comps rose 8.9%, and management raised full-year guidance to the high end of the $7.50 to $8.50 EPS range. Shares are up 31.56% year to date and sitting at $126.15. Can this turnaround push TGT to $175 in 2027?

Why Target Shares Trade Below 2021 Highs

Even after the rally, TGT is down 34.73% over five years, and shares slipped 3.61% over the past month.

University of Michigan consumer sentiment sits at 53.3, deep in pessimistic territory, and discretionary categories like Apparel and Home Furnishings remain under pressure. Operating income fell 22.89% year over year in Q1 despite the revenue beat, as higher product costs and team compensation investments squeezed profit. The stock has swung from a September 2025 low of $81.83 to today’s level. Investors are not yet convinced this is a durable inflection.

Wall Street Sees 3% Upside. I Think That’s Too Cautious

The consensus price target is $129.50, barely above today’s quote. The ratings tape reads 2 Strong Buys, 9 Buys, 23 Holds, and 3 Strong Sells. Only 30% of analysts are bullish.

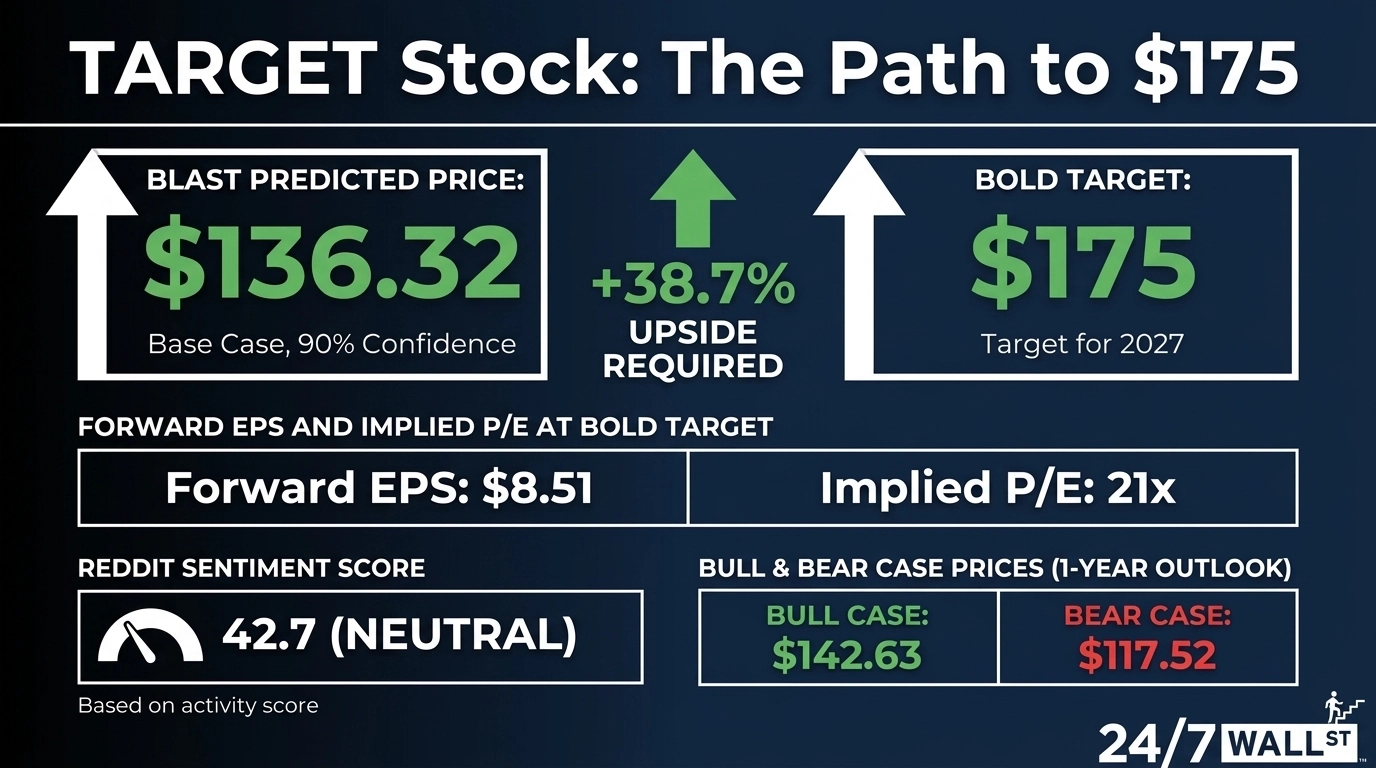

Our base case sits at $136.32 for 8.06% upside, with a bull case of $142.63 and a bear case of $117.52. Confidence on the base case is high at 90%. Analysts are anchoring on rough 2025 comparable sales declines and missing the magnitude of the Q1 inflection. When traffic accelerates while non-merchandise revenue (Roundel ads, Target+, Target Circle 360) grows nearly 25%, the earnings power story changes quickly.

The Path to $175 Per Share

Reaching $175 from today’s price of $126.15 would require a gain of 38.7%. With forward EPS of $8.51, a price of $175 implies a forward P/E of 21x. Our base case of $136.32 already implies 16x, meaning the bold target needs roughly 5 turns of additional multiple expansion.

The bull case hinges on multiple re-rating. A re-rating to 21x is achievable if FY2026 EPS lands at the high end of $8.50 and Q1’s momentum carries. CEO Michael Fiddelke stated “First quarter financial results were stronger than expected, providing encouraging early signs that our clarified strategy is resonating with our guests and driving broad-based growth across our business.”

Catalysts include same-day delivery via Target Circle 360 growing over 27%, gross margin expansion to 29.0%, and 2,002 stores generating positive comps again. Risk: tariff escalation could re-pressure margins management already excluded from guidance.

Where Target Trades Today vs Its Earnings Power

At $126.15 on forward EPS of $8.51, TGT trades at roughly 15x forward earnings. That is cheap for a defensive retailer printing high single-digit comp growth and 25% non-merchandise revenue expansion. Shares sit 2% below the 52-week high of $131.85 and well above the $81.83 low.

Over the past decade, the stock has returned 151.14%, proving the franchise can compound when execution lines up. A 21x multiple is reasonable for a name with this moat, dividend record, and digital reacceleration.

Is $175 Realistic?

Hitting $175 requires a 38.7% gain and a re-rating to 21x forward earnings. I call it a stretch, but achievable.

Three things need to go right: FY2026 EPS lands at the high end of the $8.50 range, comparable sales stay positive for three more quarters, and non-merchandise revenue keeps compounding above 20%. A renewed tariff shock or consumer rollover would derail the path quickly. We’ve outlined the blueprint for how Target could reach $175 in 2027.

Contact [email protected] for any questions or corrections.