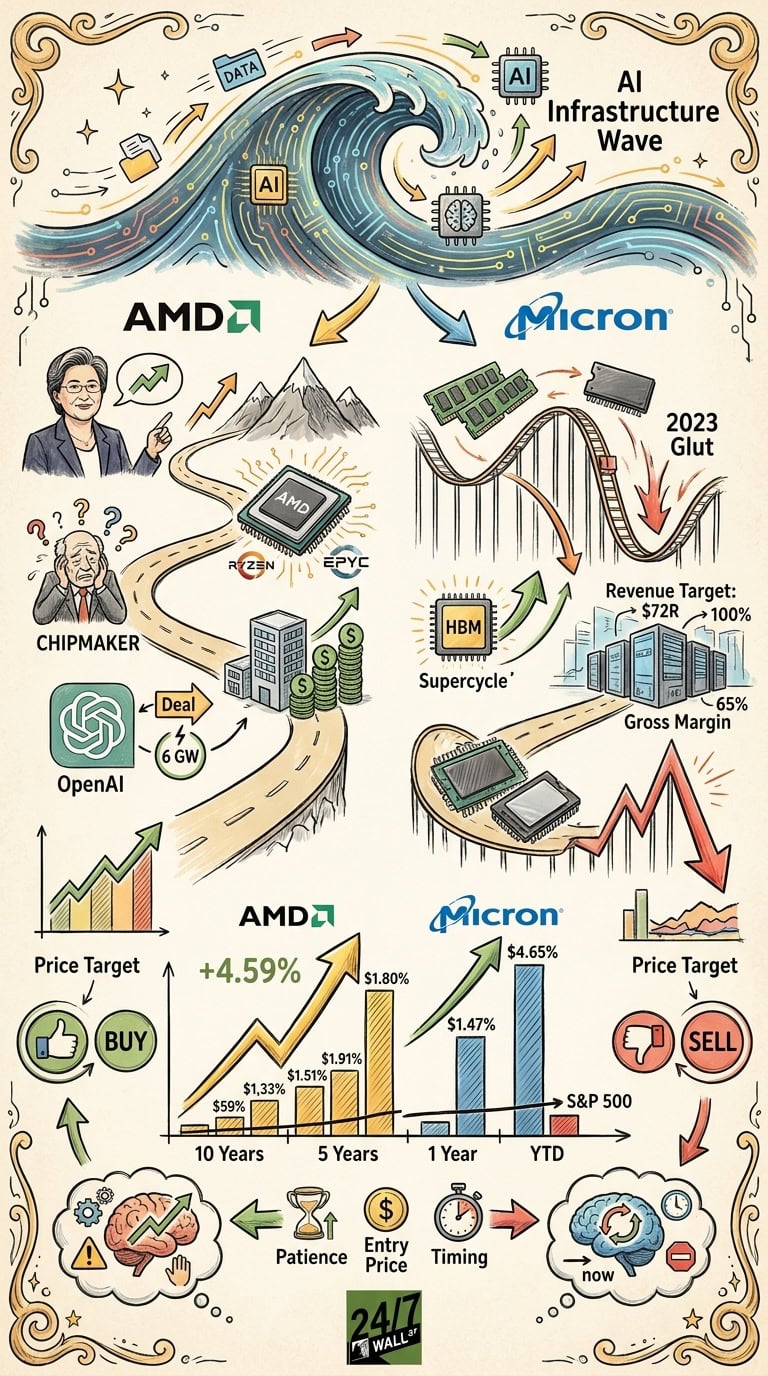

Advanced Micro Devices (NASDAQ: AMD | AMD Price Prediction) and Micron Technology (NASDAQ: MU) both ride the same AI infrastructure wave today, but they got here on very different paths. AMD spent a decade clawing back relevance under Lisa Su. Micron spent it surviving the memory cycle’s brutal swings. A $1,000 bet on either stock a decade ago would have crushed the S&P 500. Here is how the numbers shake out across four horizons.

| Period | AMD Return | MU Return | S&P 500 |

|---|---|---|---|

| 10 Years | 11,031.19% ($111,312) | 6,602.87% ($67,029) | 258.70% |

| 5 Years | 505.82% ($6,058) | 854.11% ($9,541) | 79.70% |

| 1 Year | 322.28% ($4,223) | 693.87% ($7,939) | 27.88% |

| YTD | 118.30% ($2,183) | 163.25% ($2,632) | 9.34% |

AMD: Lisa Su’s Decade-Long Turnaround

AMD traded near $4.20 a decade ago, a struggling chipmaker before Ryzen and EPYC rewrote the story. Data center revenue hit $5.775 billion last quarter, up 57% year over year, and the OpenAI deal for 6 gigawatts of GPU deployment validates the AI thesis. The 247Factor base case targets $527.29 over the next year and $705.04 over five years. The current recommendation is to buy shares. At a forward P/E of 67, the comeback appears mostly priced in.

Micron: The Memory Cycle Finds Its AI Moment

Micron’s chart captures every memory cycle of the past decade, including the 2023 supply glut. The HBM-driven supercycle has rewritten the script. FQ2 2026 guidance calls for $33.5 billion (plus or minus $750 million) in revenue with 81% non-GAAP gross margin. The 247Factor short-term base case is $444.07, implying 40.87% downside, even as analysts hold a $613.23 consensus target. The five-year base case lands at $286.77. The current recommendation is to sell shares. A forward P/E of 8 tells the cyclical story.

The Takeaway: Patience Paid, Entry Price Matters Now

AMD’s bull case rests on whether the hyperscaler deals (OpenAI, Meta, Oracle) translate into multi-year MI450 share gains against Nvidia and margins push toward 56%. The bear case kicks in if AI capex peaks before then and the 156x trailing P/E starts mean-reverting. Micron’s bull case requires accepting the cycle and trusting the order book reportedly stretching into 2027. The bear case rests on memories of 2023 and the model’s bearish base case. Thus, AMD’s secular growth narrative remains cautiously compelling, but Micron’s steep one-year run justifies near-term skepticism. Chip stocks reward patient capital, but they punish a mistimed entry just as quickly.

Contact [email protected] for any questions or corrections.