Kinder Morgan (NYSE:KMI | KMI Price Prediction) and Williams Companies (NYSE:WMB) just closed the books on record 2025 results, and both pipeline operators are pointing the same firehose of capital at LNG exports and data center power demand. The way they are doing it, however, looks quite different. One is leaning on a $10 billion pipeline backlog. The other is buying into power generation itself.

Records on Both Sides, but the Mix Tells the Story

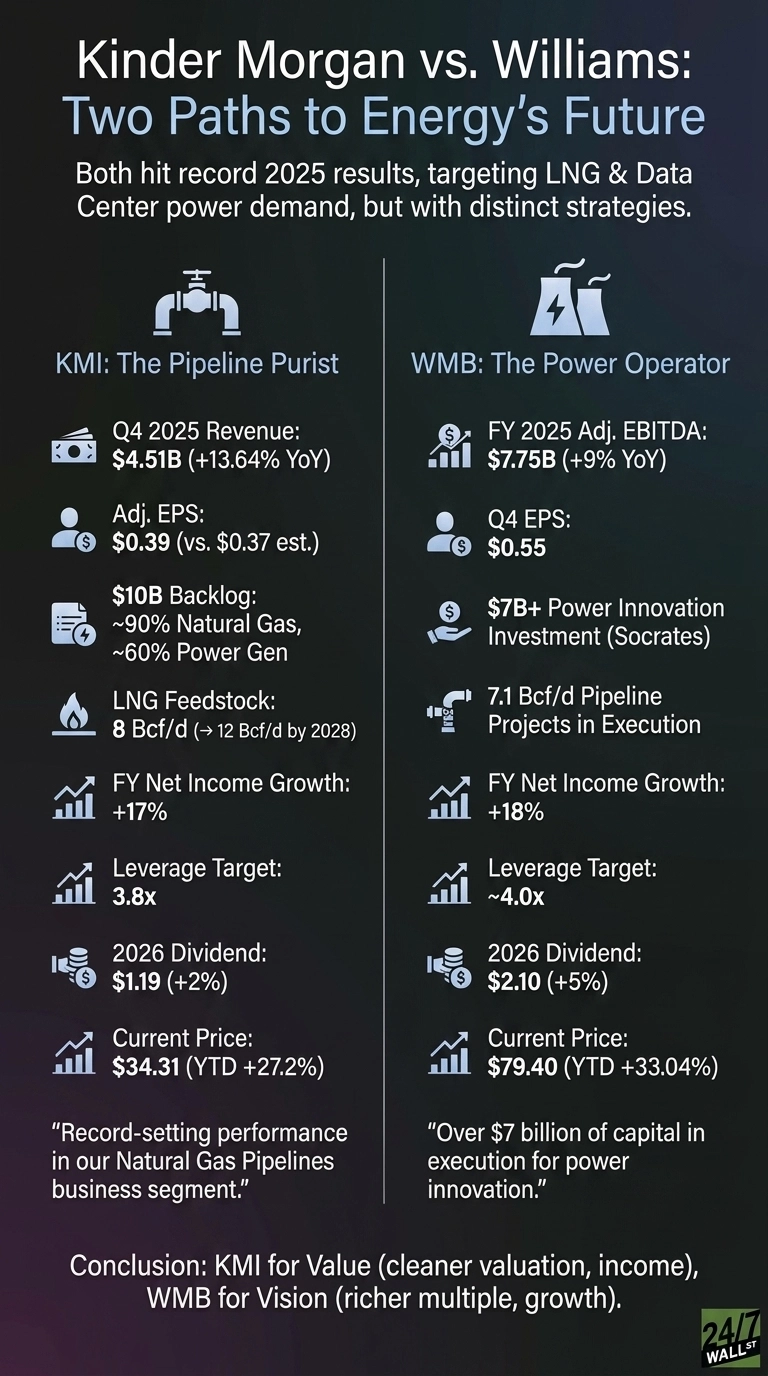

Kinder Morgan delivered adjusted EPS of $0.39 against a $0.37 estimate on $4.51 billion in revenue, up 13.64% year over year. CEO Kim Dang credited “record-setting performance in our Natural Gas Pipelines business segment”, with transport volumes up 9% and gathering volumes up 19%. The CO2 segment was the weak spot, dragged by softer commodity and D3 RIN prices.

Williams, under new CEO Chad Zamarin since July 2025, posted full-year adjusted EBITDA of $7.75 billion, up 9%, and Q4 EPS of $0.55. Transco continues to do the heavy lifting, with Transmission, Power & Gulf adjusted EBITDA of $3.71 billion, a $403 million jump. A $212 million impairment on Mid-Continent gas gathering was a reminder that not every basin is humming.

| Business Driver | Kinder Morgan | Williams |

| FY revenue | $16.94B | $11.95B |

| FY net income growth | +17% | +18% |

| Leverage target | 3.8x | ~4.0x |

| 2026 dividend | $1.19 (+2%) | $2.10 (+5%) |

Pipeline Purist vs. Power Operator

Kinder Morgan is doubling down on what it already does best. Its $10 billion project backlog is roughly 90% natural gas, with about 60% tied to power generation. Trident Intrastate, SSE4, and Mississippi Crossing are all traditional pipeline projects. Dang says “total demand for natural gas is expected to grow by 17% through 2030, led by LNG exports”, and KMI already moves 8 Bcf/d to LNG facilities, growing to 12 Bcf/d by end of 2028.

Williams is taking a bolder step. Zamarin is putting over $7 billion of capital into power innovation projects, including the newly announced “Socrates the Younger.” The Cogentrix platform, Rimrock and Saber acquisitions, and the Woodside Energy LNG partnership all push Williams further down the value chain than a traditional pipeline operator goes. Investors are paying for that ambition: WMB trades at a 34 P/E versus 23 for KMI.

The Next Test Is Whether the Premium Pays Off

WMB shares are up 33.04% year to date and just touched a 52-week high, while KMI has climbed 27.2%.

I will be watching whether Williams’ first power innovation project hits its second-half 2026 commissioning on budget. For Kinder Morgan, the catalyst is FERC certificates on SSE4 and Mississippi Crossing, both expected in July 2026. Analyst targets sit at $81.99 for WMB and $35.33 for KMI, leaving modest implied upside in both names.

Why I Lean Toward Kinder Morgan for Value, Williams for Vision

The two stocks frame distinct investor profiles. KMI offers a cleaner valuation, a 3.49% yield, an S&P upgrade to BBB+, and a backlog that is already commercialized, an income-style profile tied to LNG and power gas.

Williams trades at a richer multiple and asks investors to underwrite execution on power plants and acquisitions, a growth-tilted profile with more upside if Socrates works. Steel tariff moves and 2026 power demand forecasts are the key variables that could reshape either thesis.

Contact [email protected] for any questions or corrections.