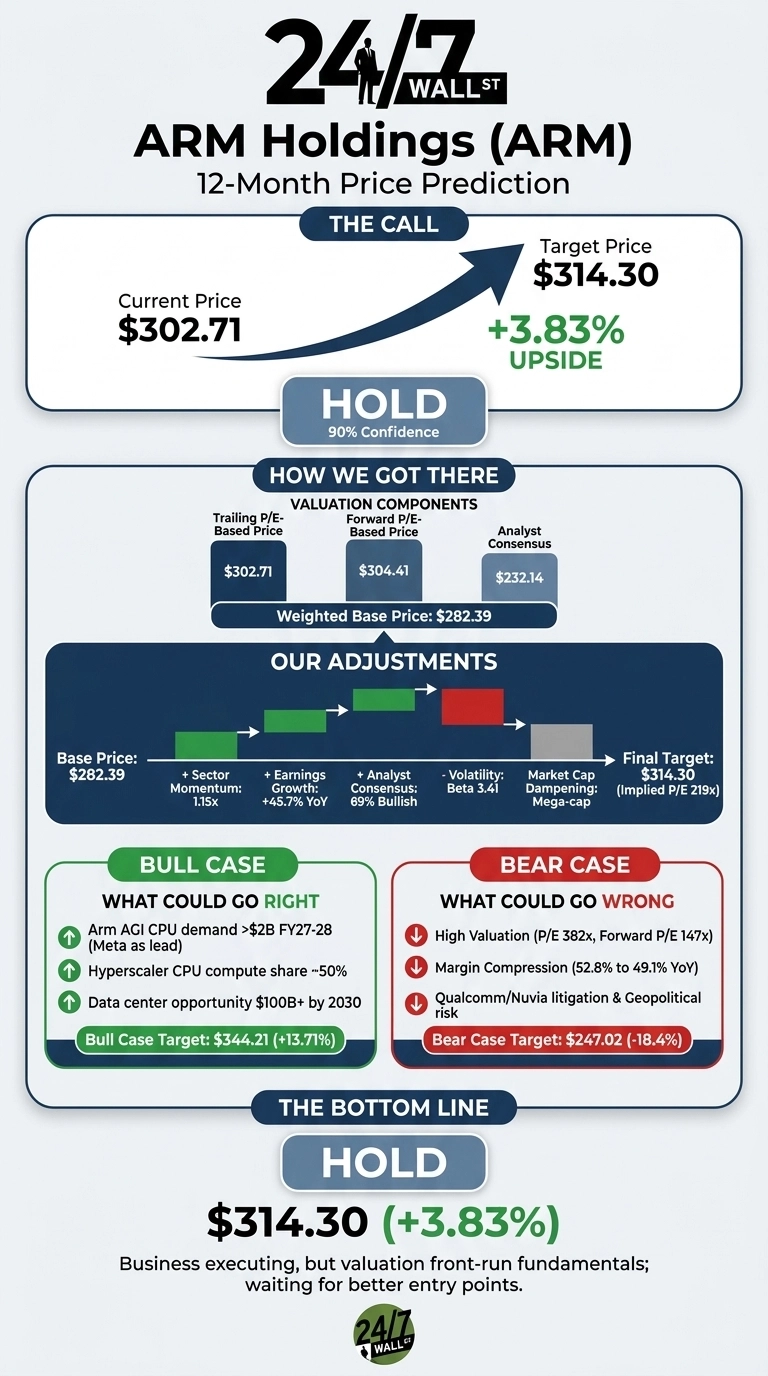

I’ll cut to the chase. Arm Holdings (NASDAQ:ARM | ARM Price Prediction) has more than doubled year-to-date, and our proprietary model now sees only a sliver of upside left in the near term. Our 24/7 Wall St. price target for Arm is $314.30 over the next 12 months, implying roughly 3.83% upside from the recent close of $302.71. The recommendation is hold, with a high confidence reading of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $302.71 |

| 24/7 Wall St. Price Target | $314.30 |

| Upside | 3.83% |

| Recommendation | HOLD |

| Confidence Level | 90% |

An AI Compute Story That Has Already Repriced

Arm has been one of the cleanest AI infrastructure trades of 2026. Shares are up 176.93% year to date, 40.22% in the past month, and 17.91% in the past week alone, even after a 5.76% pullback on May 27. The stock sits 29% below a 52-week high of $325 and well above the $100.02 52-week low.

The fundamentals justify the move. Q4 FY2026 revenue hit $1.49 billion, growing 20.1% YoY and beating consensus, while non-GAAP EPS of $0.60 beat the $0.57 estimate. Data center royalty revenue more than doubled YoY. CEO Rene Haas framed the year as a turning point, citing “a third consecutive year of more than 20% revenue growth” and noting Arm AGI CPU demand “has exceeded expectations.”

The Case for $344 and Higher

Bulls have a clean narrative. Arm AGI CPU, the company’s first data center chip, already has more than $2 billion in committed customer demand across FY2027 and FY2028, with Meta as lead partner.

Arm holds roughly 50% CPU compute share among top hyperscalers, with NVIDIA Vera, Google Axion, and Microsoft Cobalt all built on Arm. Management is targeting a $100 billion data center CPU opportunity by 2030. ACV grew 22% YoY to $1.66 billion, and full-year FCF jumped 395.51%. Our bull case scenario lands at $344.21, or 13.71% upside.

What Could Go Wrong

The bear case starts with valuation. Arm trades at a trailing P/E of 382 and a forward P/E of 147, leaving little margin for error. The consensus analyst target of $232.14 sits well below the current quote. Non-GAAP operating margin compressed from 52.8% to 49.1%, RPO fell 7% YoY, and Q4 FCF declined 17.39%.

Bulls would counter that the margin pressure reflects a 43% ramp in R&D to $1.911 billion, funding the AGI CPU roadmap. Add the Qualcomm/Nuvia trial expected in Q4 2026, US export controls, a 25% tariff on semi imports, and SoftBank’s controlling stake, and the downside scenario lands at $247.02, or -18.4%.

Arm Price Prediction 2026-2030

My 24/7 Wall St. price target for Arm is $314.30 with hold at 90% confidence. The business is executing, but the stock has front-run the fundamentals after a 177% YTD rally. A pullback toward the $250 to $270 zone would mark a more attractive entry, where royalty growth and AGI CPU bookings would carry the valuation.

Caution is warranted if Arm trades through $325 without a fresh customer announcement or if the Qualcomm trial in Q4 introduces overhang. For now, holders should keep an eye on the stock and let the bookings do the work.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $314.30 |

| 2030 | $376.50 |

These projections assume Arm continues converting AGI CPU demand into royalty revenue and hyperscaler share holds near 50%. Material upside or downside could come from the Qualcomm verdict, China export policy, or a step-change in agentic AI capex.

Contact [email protected] for any questions or corrections.