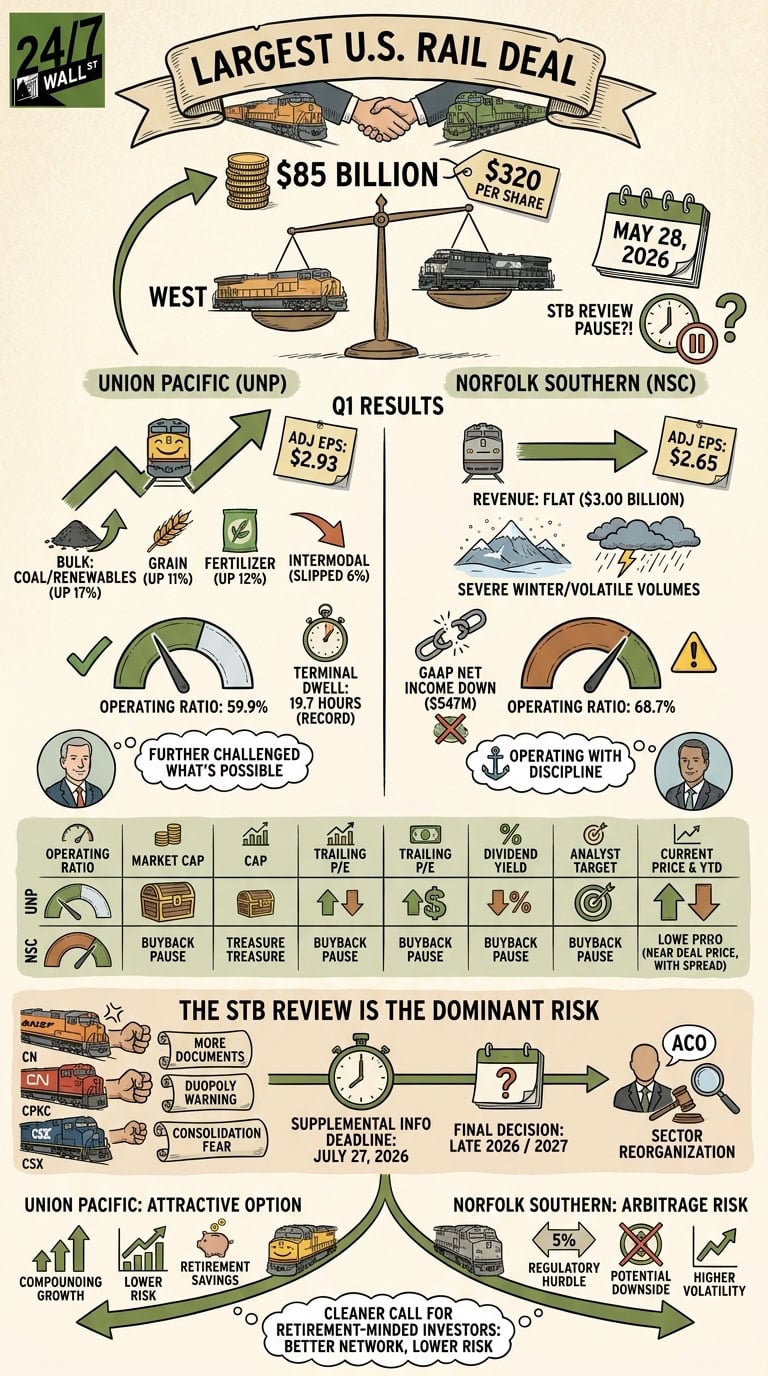

Union Pacific (NYSE: UNP | UNP Price Prediction) and Norfolk Southern (NYSE: NSC) sit on opposite ends of the largest rail deal in U.S. history: a stock-and-cash transaction valued at $320 per share and $85 billion in enterprise value. The Surface Transportation Board (STB) accepted the revised application on May 28, 2026, then paused the review to request more information. That backdrop reshapes how investors should read the companies’ Q1 results.

The Western Network Compounded. The Eastern One Held the Line.

Union Pacific delivered adjusted EPS of $2.93 on $6.22 billion in revenue, with a 59.9% adjusted operating ratio. Bulk did the heavy lifting: coal and renewables jumped 17%, grain rose 11%, and fertilizer climbed 12%. Although, intermodal slipped 6%. CEO Jim Vena said the team “further challenged what’s possible from our great railroad,” and the operating data backed him up, with terminal dwell of 19.7 hours hitting a record.

Norfolk Southern posted adjusted EPS of $2.65 on essentially flat revenue of $3.00 billion. The eastern carrier ran a much heavier 68.7% adjusted operating ratio, and GAAP net income fell to $547 million as a $185 million Eastern Ohio recovery in Q1 2025 turned into $10 million in net expenses. CEO Mark George credited the team for “operating with discipline amid volatile volumes, severe winter weather, and a rapidly shifting macroeconomic environment.”

Acquirer Discipline Versus Target Optionality

| Lens | Union Pacific | Norfolk Southern |

| Operating ratio | 59.9% | 68.7% |

| Market cap | $155.9B | $68.5B |

| Trailing P/E | 22 | 26 |

| Dividend yield | 2.1% | 1.8% |

| Analyst target | $291.05 | $335.29 |

Norfolk Southern shares closed at $304.96, leaving roughly a 5% spread to the $320 deal price. Union Pacific, at $262.64, has run up 13.5% year to date, even after a 3.9% drop on the STB pause. Both companies paused buybacks to preserve capital for the deal.

The STB Review Is the Dominant Risk

Rivals are pushing back hard. BNSF and CN have filed motions to force UP and NS to produce more merger documents, CPKC CEO Keith Creel has warned the deal would create a duopoly and trigger further consolidation, and CSX CEO Steve Angel opposed the merger at the May 16, 2026, shareholder meeting. The supplemental information deadline is July 27, 2026, with a final decision expected late 2026 or 2027. Activist pressure on CSX from Ancora confirms this is a sector reorganization.

The Case for Union Pacific Over Norfolk Southern

Union Pacific may be the more attractive option. The math is asymmetric. Norfolk Southern is essentially a 5% arbitrage with regulatory tail risk; if the STB blocks the deal or demands heavy divestitures, the stock likely retraces toward its standalone fair value, well below the $323.38 all-time high reached on May 27. Union Pacific keeps compounding either way. Vena’s team is targeting mid-single-digit EPS growth in 2026 and a high-single to low-double-digit CAGR through 2027, and the 2.1% dividend is funded by a railroad already running nine points tighter on operating ratio than its eastern partner.

For a retirement-minded investor, owning the operator with better network productivity and lower deal-break downside is the cleaner call. That view would change only if Norfolk Southern traded materially below its standalone fair value. At current prices, it does not.

Contact [email protected] for any questions or corrections.