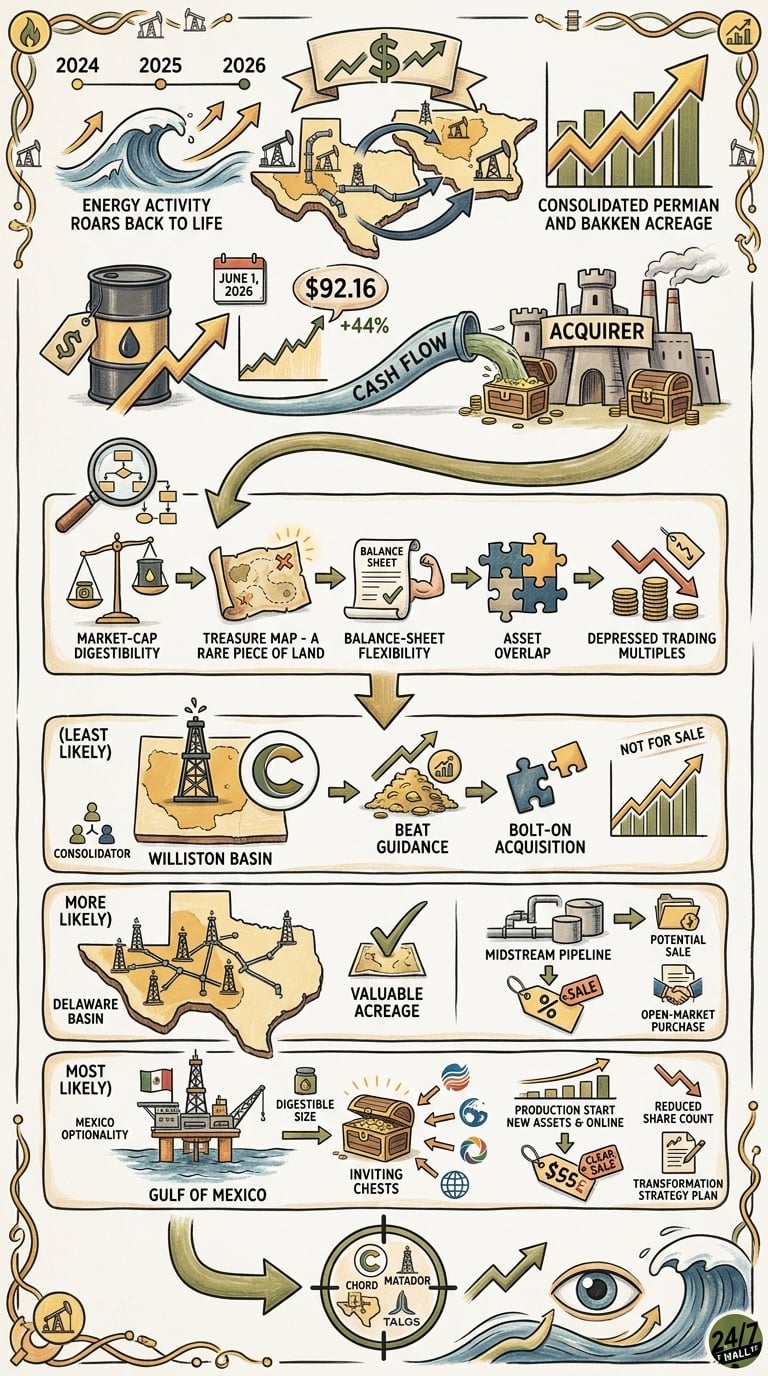

Energy M&A roared back to life in 2024 and 2025 as supermajors consolidated Permian and Bakken acreage. The catalysts for 2026 are firmly in place. West Texas Intermediate (WTI) crude trades at $92.16 per barrel as of June 1, 2026. That is roughly 44% above year-ago levels, fattening acquirer cash flows as a small group of mid-cap exploration and production companies (E&Ps) look strategically isolated. Our framework weighs market-cap digestibility, basin scarcity, balance-sheet flexibility, asset overlap with likely acquirers, and depressed trading multiples relative to peers. Three names stand out, ranked from the least likely target to the most acquirable.

3. Chord Energy (Least Likely)

Chord Energy (NASDAQ: CHRD | CHRD Price Prediction) is the largest at a $7.8 billion market cap and a pure-play Williston Basin operator. Logical acquirers would be Bakken-adjacent majors: ConocoPhillips, Chevron, or Exxon, all with demonstrated appetite for low-cost oil-weighted inventory. ConocoPhillips carries a $140.8 billion market cap and $23.35 billion in EBITDA. That is more than enough financial firepower to absorb Chord without straining its balance sheet.

Strategic fit is real: 917.5 MMBoe (million barrels of oil equivalent) of proved reserves and Q1 2026 oil production of 158.0 MBopd (thousand barrels of oil per day) that beat guidance of 152.5 to 155.5 MBopd make Chord the dominant Williston pure-play. Valuation, however, is not compelling. Shares closed at $138.00 on June 1, 2026, up 48.9% year to date and 53.3% over the past year. The consensus analyst target price of $173.44 suggests further upside. However, Chord just completed its own $542.2M XTO Williston bolt-on, positioning it as a consolidator rather than prey.

2. Matador Resources

Matador Resources (NYSE: MTDR) checks more acquisition boxes. The $7.0 billion market cap Delaware Basin pure-play holds roughly 217,600 net acres in the most consolidated basin in the United States. ConocoPhillips, Devon, or Diamondback would view the acreage and San Mateo midstream subsidiary as a clean strategic fit.

Operational momentum is undeniable. Q1 2026 adjusted EPS of $1.53 beat $1.26 by 21.41%, though revenue of $818.7 million fell short of estimates by 6.3%. Management raised FY26 oil guidance to 123,000 to 125,000 bpd with adjusted free cash flow of $1.1 billion to $1.2 billion. The midstream layer adds optionality: Five Point is exploring a continuation vehicle for its 49% San Mateo stake, a potential catalyst for a broader deal.

Valuation supports the case. Matador trades at a trailing P/E of 14x, forward P/E of 9x, and EV/EBITDA of 5x, a notable discount to large-cap Permian peers. The consensus target of $72.61 is well above the $56.07 close on June 1. CEO Joe Foran’s recent open-market purchase at $52.36 per share signals insider conviction, though founder-led companies often resist a sale until pricing is right.

1. Talos Energy (Most Likely)

Talos Energy (NYSE: TALO) tops our ranking. At a $2.5 billion market cap, it is the most digestible target. Its asset base is also genuinely scarce: a pure-play offshore Gulf of Mexico E&P with material Mexico optionality. Murphy Oil, Hess, Harbour Energy (already partnered on Zama), or an international major like Repsol or Equinor all have logical reasons to bid.

The strategic fit is strongest. Monument is expected to deliver first oil in late 2026 at 20 to 30 MBoed gross. CPN starts production in Q3 2026, and the Daenerys sub-salt Miocene discovery sits in a region where deepwater inventory is increasingly rare. Talos already sold its 30.1% Talos Mexico stake to Grupo Carso for $82.7 million with $33.0 million contingent, signaling willingness to monetize.

The valuation case is compelling. Despite an 85.1% one-year gain to $14.88, the stock remains down 59.0% over 10 years. Its performance was weighed down by a $145 million Q1 ceiling-test impairment and $173.55 million in derivatives losses. EV/EBITDA of 5x and an analyst target of $18.70 imply meaningful upside. Additionally, $135 million in buybacks since mid-2025 cut share count by 7%, shrinking the float a bidder must absorb. New CEO Paul Goodfellow’s transformation strategy and an extended $700 million borrowing base through January 2030 position the asset cleanly for a sale.

The Consolidation Setup

The 2026 backdrop favors continued energy M&A. With WTI elevated, free cash flow at majors swelling, and prime acreage in the Permian, Bakken, and deepwater Gulf increasingly scarce, mid-cap pure-plays with focused asset bases sit squarely in the crosshairs. Chord stands out for Williston scale, Matador for Delaware acreage and midstream optionality, and Talos as the scarcest, most digestible asset. The strategic, operational, and valuation conditions are more aligned than they have been in years.

Contact [email protected] for any questions or corrections.