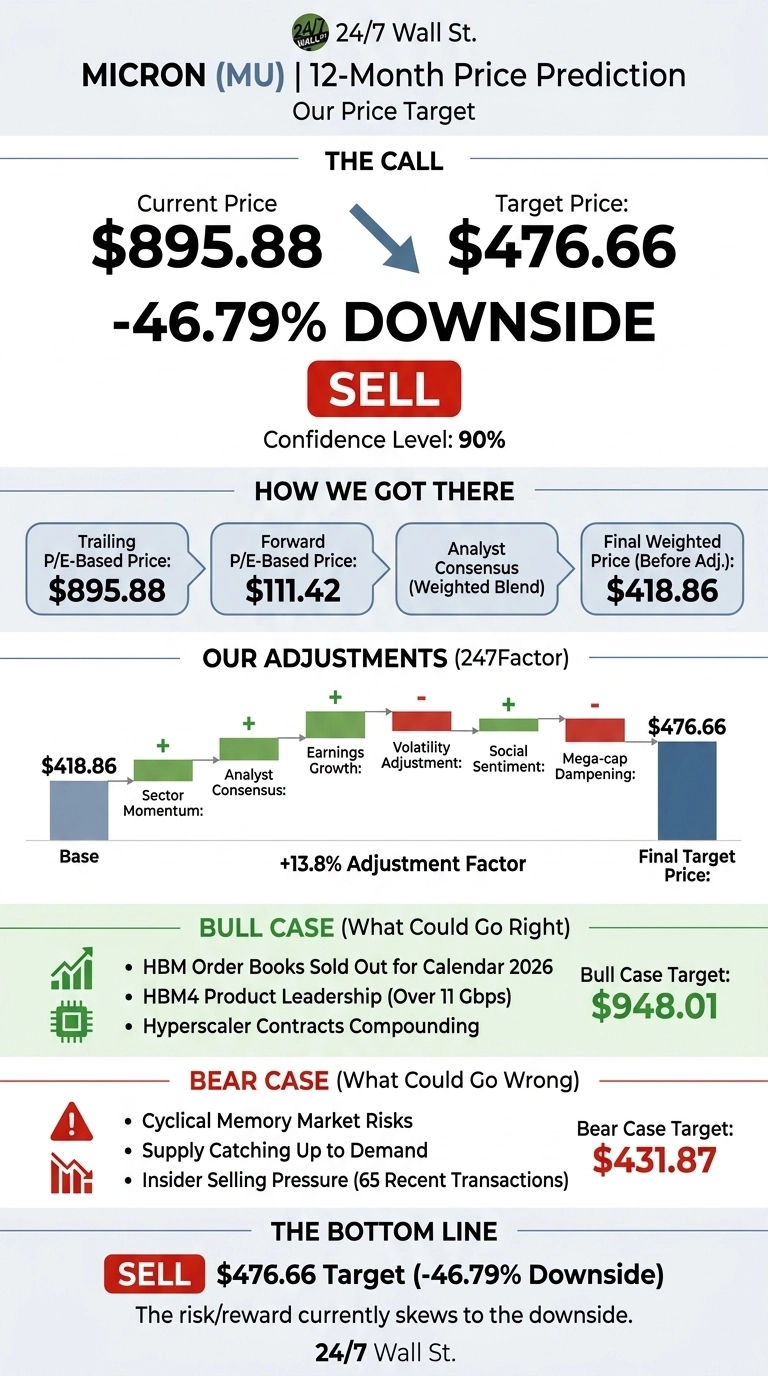

Micron Technology (NASDAQ:MU | MU Price Prediction) just joined the trillion-dollar club after a 19.29% single-day surge on UBS analyst Timothy Arcuri’s price target hike from $535 to $1,625. Micron now trades at $895.88. The question for investors is whether anything is left in the tank.

Our 24/7 Wall St. price target for Micron is $476.66 over the next 12 months, implying 46.79% downside. Our recommendation is sell with a 90% confidence level. A memory cyclical trading at 35x trailing earnings after a 861.83% one-year run does not square mathematically.

| Metric | Value |

|---|---|

| Current Price | $895.88 |

| 24/7 Wall St. Price Target | $476.66 |

| Upside/Downside | -46.79% |

| Recommendation | SELL |

| Confidence Level | 90% |

Why We Could Be Wrong

Micron is one of the most divisive stocks in the market. Real upside could come from HBM order books that are sold out for all of calendar 2026, or from the company’s industry-leading HBM4 product running at over 11 gigabits per second. A detailed bull case appears below.

From $93 to a Trillion-Dollar Cap in 12 Months

Micron is up 214.04% year to date and 80.36% in the past month alone.

Fiscal Q1 2026 results drove the move: revenue of $13.643 billion, up 56.6% year over year, non-GAAP EPS of $4.78 versus $3.94 expected, and GAAP gross margin expanding to 56% from 38.4% from a year earlier. Management guided Q2 revenue to a record $18.70 billion with EPS of $8.42. On May 26, Reuters reported Micron’s entry into the trillion-dollar club alongside SK Hynix, and UBS raised its price target.

The Case for $1,625 and Beyond

Bulls have ammunition. CEO Sanjay Mehrotra told analysts the company forecasts “an HBM TAM CAGR of approximately 40% through calendar 2028, from approximately $35 billion in 2025 to around $100 billion in 2028”. He added that “the gap between the demand and supply for all of DRAM, including HBM, is really the highest that we have ever seen“.

UBS’s $1,625 target assumes hyperscaler memory contracts continue to compound. Of 44 analysts, 39 rate it Buy or Strong Buy with zero Sells, and consensus sits at $613.23. If HBM4 ramps cleanly in 2026 and pricing holds, our bull-case scenario flags $948.01 within 12 months.

The Risks Worth Watching

Memory is cyclical. Trailing P/E of 35x on peak-cycle earnings is the warning sign. Our bear-case 12-month target sits at $431.87, and our 5-year base case projects $280.56 as supply catches up.

The dashboard flags 65 recent insider transactions with net selling. Bulls counter that insider sales follow parabolic moves and that Micron’s 8x forward P/E looks cheap if FY27 earnings hold, but that “if” is the entire trade.

The Risk Isn’t Worth the Reward

My 24/7 Wall St. price target is $476.66 with a sell rating and 90% confidence. Paying 35x trailing earnings for a cyclical at the top of its cycle is how investors get hurt.

The bull thesis strengthens if HBM4 ramps faster than guidance and 2027 contracts confirm pricing power. The bear thesis strengthens if forward bit growth surprises to the upside on the supply side. For now, the risk/reward skews to the downside.

Micron Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $476.66 |

| 2027 | $410.00 |

| 2028 | $355.00 |

| 2029 | $315.00 |

| 2030 | $280.56 |

These projections assume Micron’s HBM leadership holds but the broader memory market normalizes as supply catches demand by 2028. Significant upside could materialize if the $100 billion HBM TAM arrives early or if multiyear hyperscaler contracts lock in pricing through 2030.

Contact [email protected] for any questions or corrections.