Pfizer (NYSE:PFE | PFE Price Prediction) and Merck (NYSE:MRK) both just closed earnings chapters that frame the 2026 dividend debate clearly. Pfizer wrapped fiscal 2025 with a $0.66 adjusted EPS Q4 beat. Merck followed with a Q1 2026 report dominated by a $9 billion Cidara acquisition charge. Two very different income stories for yield hunters.

One Pays You to Wait. One Pays You to Believe.

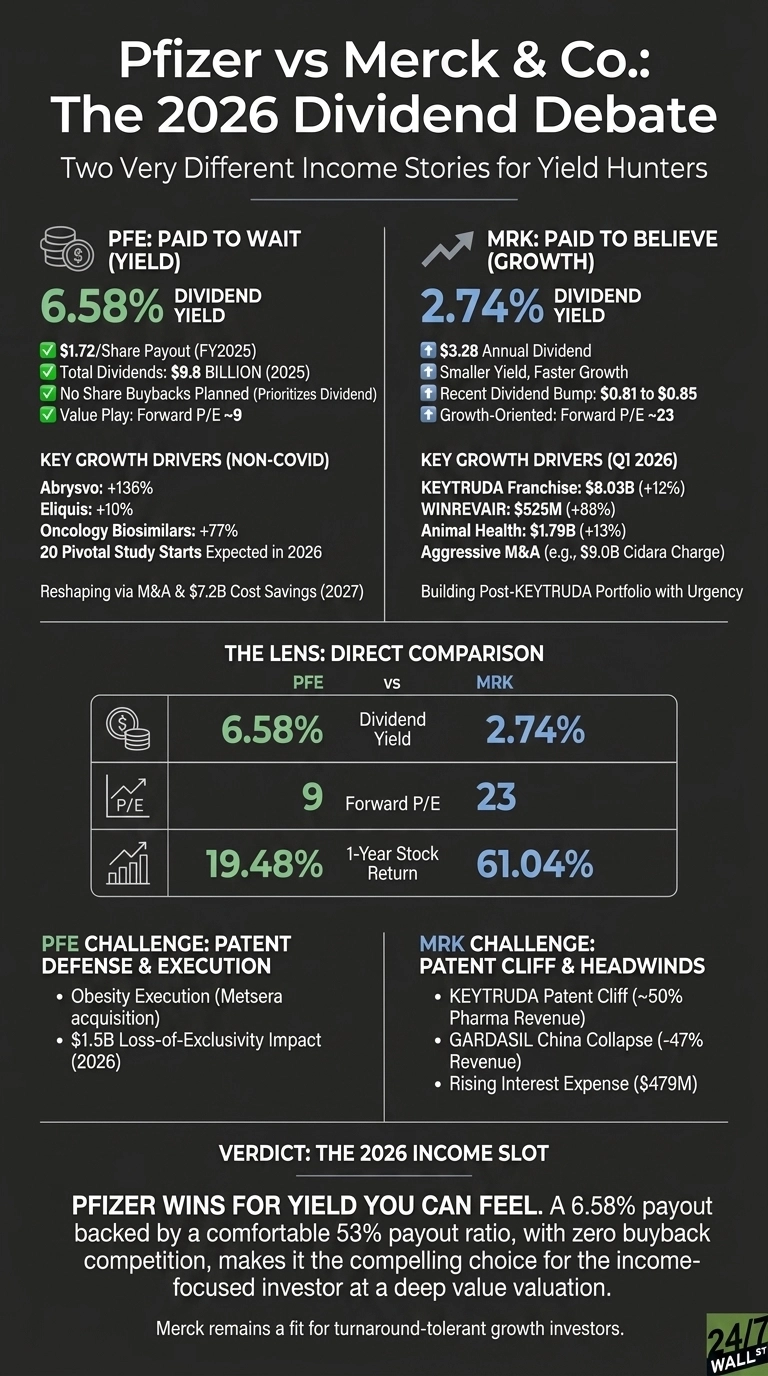

Pfizer is now a 6.58% yielder, distributing $9.8 billion in 2025 dividends at $1.72 per share. That payout sits on a $3.22 adjusted EPS base, so coverage looks comfortable even with COVID revenue fading. Non-COVID growth told the real story: Abrysvo jumped 136%, Eliquis added 10%, and oncology biosimilars surged 77%.

Merck pays a smaller yield of 2.74% on a $3.28 annual dividend, but the underlying business is growing faster. KEYTRUDA delivered $8.03 billion in Q1 2026, up 12%, while WINREVAIR rocketed 88% to $525 million. Animal Health added a steady 13%. The recent quarterly dividend bump from $0.81 to $0.85 signals confidence.

| Lens | Pfizer | Merck |

| Dividend Yield | 6.58% | 2.74% |

| Forward P/E | 9 | 23 |

| 1-Year Stock Return | 19.48% | 61.04% |

Yield Hunter vs. Pipeline Believer

Pfizer is reshaping itself through M&A. CEO Albert Bourla told investors “2026 will be an important year rich in key catalysts, including our expectation for approximately 20 key pivotal study starts”.

The $7 billion Metsera buy pushes Pfizer into obesity, and management is chasing $7.2 billion in net cost savings by 2027. Buybacks remain off the table, which I read as a clean signal that the dividend is the priority.

Merck is building a post-KEYTRUDA portfolio with urgency. The Cidara deal closed, Terns is pending at roughly $5.8 billion, and Verona Pharma already contributed $131 million in Q1. The risk: GARDASIL revenue in China fell 47%, and interest expense climbed to $479 million. Faster growth, heavier balance-sheet lifting.

The Next Test Is Patent Defense

For Pfizer, I will be watching whether Metsera’s ultra-long-acting GLP-1 candidates can credibly compete with Novo and Lilly. The $1.5 billion loss-of-exclusivity headwind in 2026 is manageable, but obesity execution is the swing factor.

For Merck, the KEYTRUDA biosimilar clock is the dominant concern, given it represents roughly 50% of pharma revenue. WINREVAIR and the animal health franchise need to keep compounding.

Why I Lean Toward Pfizer for the 2026 Income Slot

If you want yield you can actually feel, Pfizer wins this matchup. A 6.58% payout backed by a 53% payout ratio and zero buyback competition for cash is hard to ignore at a forward P/E of 9.

Merck is the better operating business and its 61.04% one-year gain proves it, but you are paying 23 times forward earnings for a 2.74% yield. For a turnaround-tolerant growth investor, Merck still fits. For my dividend bucket in 2026, Pfizer’s combination of value and income reads more compelling.

Contact [email protected] for any questions or corrections.