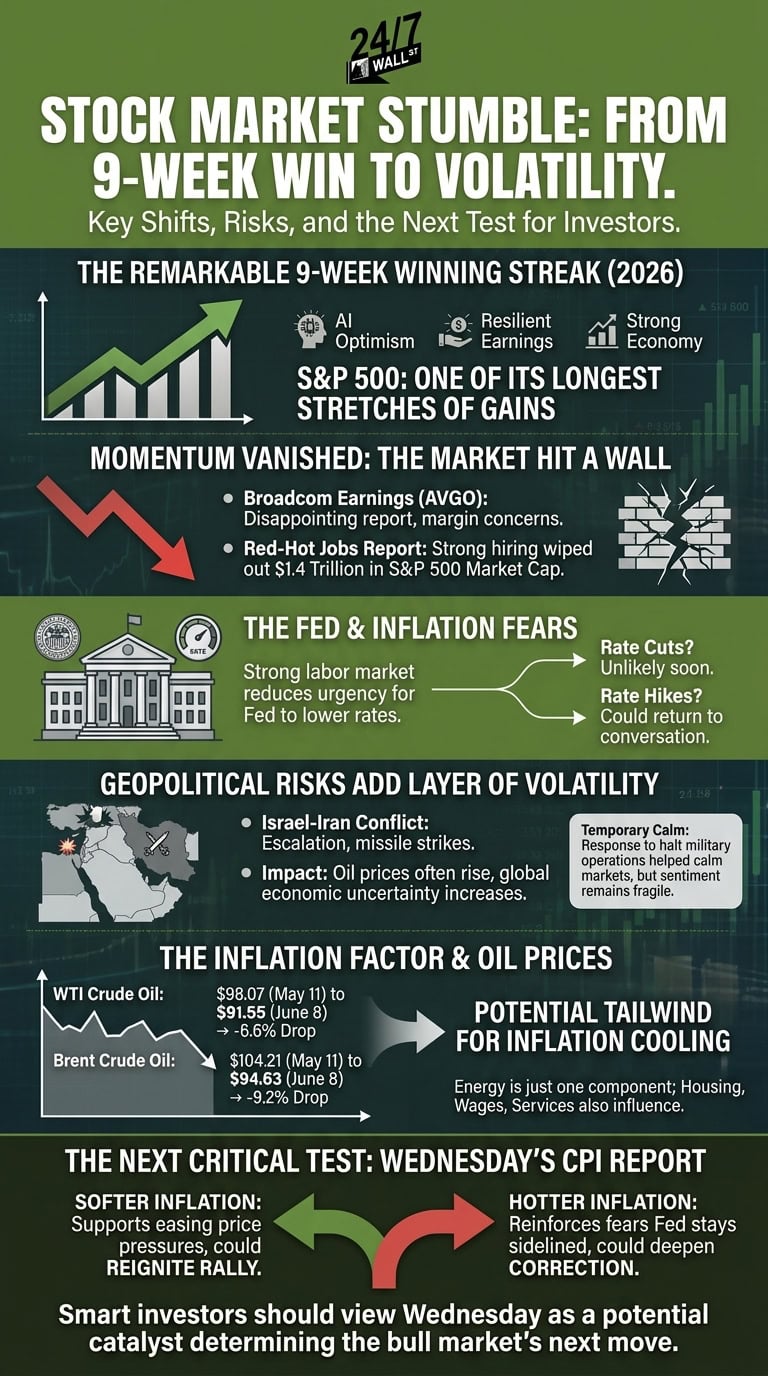

The stock market spent most of 2026 doing what few investors expected after last year’s volatility: climbing steadily higher. The S&P 500 entered June riding a remarkable nine-week winning streak, one of its longest stretches of gains in recent years. Optimism surrounding artificial intelligence, resilient corporate earnings, and a surprisingly strong economy helped fuel the advance. Then, in the span of a few days, that momentum vanished.

A disappointing earnings report from Broadcom (NASDAQ:AVGO | AVGO Price Prediction) set the stage and prompted a market sell-off, while a red-hot jobs report delivered the knockout punch. Suddenly, investors who had been anticipating Federal Reserve rate cuts found themselves confronting a different possibility entirely — that cuts may not come at all, and that rate hikes could return to the conversation sooner than expected.

Now, with inflation data arriving Wednesday and Thursday, investors may be about to learn whether the bull market merely paused or whether something more serious is developing.

A Winning Streak Runs Into a Wall

The market’s stumble began with earnings from Broadcom. While the memory-chip maker continued to benefit from AI-related demand, investors focused on concerns surrounding margins and future growth expectations.

That weakness might have remained isolated had it not been followed by the Bureau of Labor Statistics’ latest employment report. The jobs data showed hiring remained remarkably strong, making it harder for the Federal Reserve to justify lowering interest rates anytime soon, wiping out $1.4 trillion in S&P 500 market cap.

A strong employment environment is often good news for workers. For stocks, however, it can create a problem. The Federal Reserve’s dual mandate requires it to keep inflation under control, and a strong labor market reduces the urgency for policymakers to provide economic stimulus through lower rates.

Middle East Tensions Add Another Layer of Volatility

As if investors didn’t have enough to worry about, geopolitical risks returned to the forefront this weekend.

Stock futures tumbled overnight after fresh conflict erupted between Israel and Iran. The latest escalation began after Israel bombed targets in Beirut, Lebanon. Iran responded with rocket attacks against Israel, prompting additional Israeli missile strikes targeting Tehran.

Markets reacted immediately. Rising geopolitical tensions often push oil prices higher and increase uncertainty about global economic growth.

Yet futures reversed course before the opening bell after President Trump called for both sides to halt military operations and return to negotiations. Iran subsequently indicated it would suspend further military action so long as Israel refrained from additional attacks in Lebanon.

That response helped calm markets, but it also highlighted how fragile investor sentiment remains. Every step toward peace has sparked rallies. Every setback has triggered selling. Regardless, the market’s most important test may still lie ahead.

Wednesday’s Inflation Report Could Be the Real Catalyst

However, what may matter most this week is inflation. BLS will release May Consumer Price Index data on Wednesday, followed by Producer Price Index data on Thursday. Those reports could have an outsized impact because investors are already worried that the Federal Reserve may be forced to keep rates elevated for longer than expected.

April’s CPI report showed inflation running higher at 3.8% and exceeding expectations. One major contributor was energy. Oil prices influence everything from transportation costs to manufacturing expenses, making them a critical inflation input.

The good news is that energy prices have moved in the right direction over the past month:

| Commodity | Price per Barrel May 11 | Price per Barrel June 8 | Past 4 Weeks |

| WTI Crude Oil | $98.07 | $91.55 | -6.6% |

| Brent Crude Oil | $104.21 | $94.63 | -9.2% |

Source: Oilprice.com

Those declines create a potential tailwind for inflation.

Granted, oil is only one component of the CPI basket. Housing costs, wages, insurance, healthcare, and numerous service categories also influence the final number. In addition, previous energy price increases can take time to work their way through the economy.

Still, lower oil prices are an encouraging sign. If Wednesday’s CPI report shows inflation cooling again, investors could quickly revisit expectations for future rate cuts.

Key Takeaway

In short, the market’s nine-week winning streak ended because investors suddenly had to confront the possibility that interest rates may stay elevated longer than expected. Geopolitical tensions have amplified that uncertainty, creating sharp swings in sentiment almost daily.

Wednesday’s CPI report now sits at the center of the investment landscape. A softer-than-expected inflation reading would support the case that price pressures are easing and could reignite the rally that defined much of 2026. A hotter reading, on the other hand, would reinforce fears that the Federal Reserve remains stuck on the sidelines.

Ultimately, smart investors should view Wednesday as more than just another economic report. It may determine whether President Trump’s bull market resumes its climb or whether the correction that began last week has further room to run.