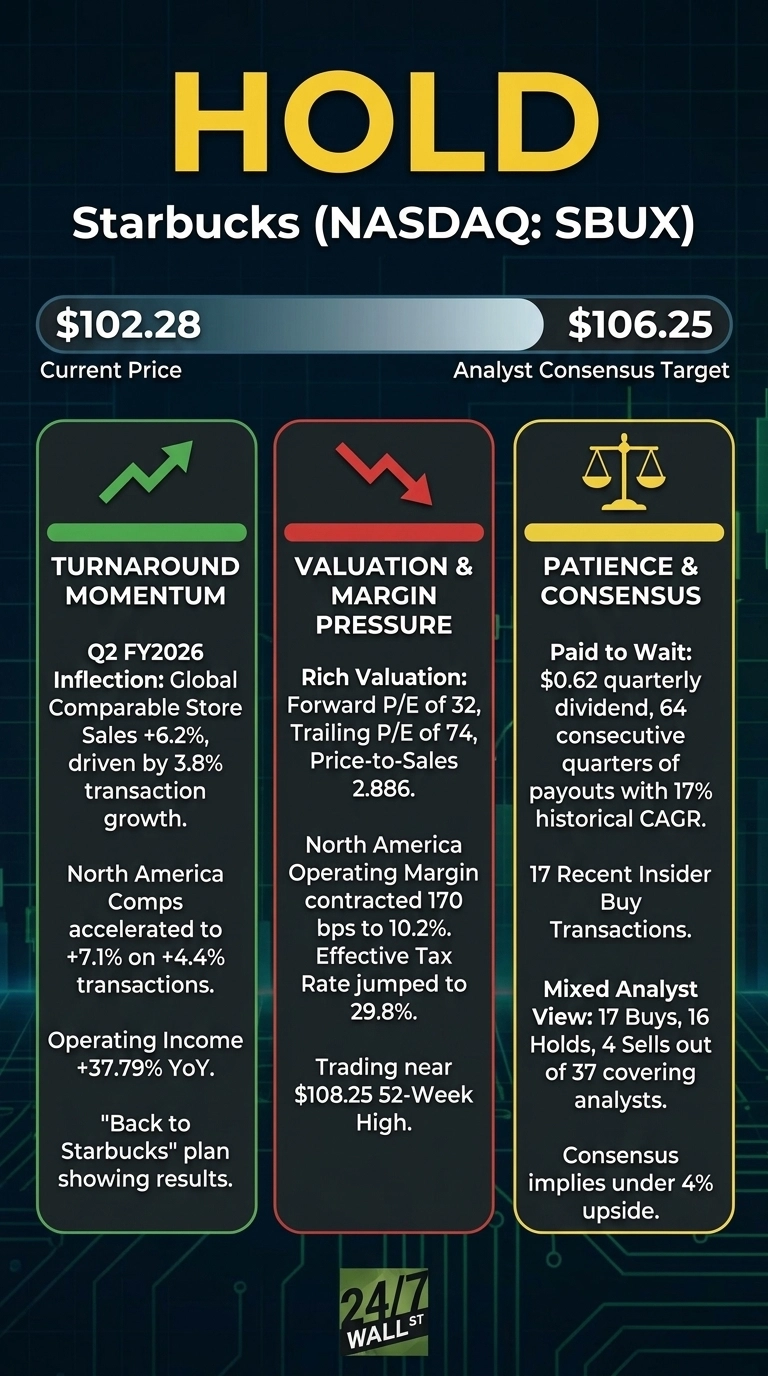

At $102.28, Starbucks (NASDAQ:SBUX | SBUX Price Prediction) is a Hold. The coffee giant has rallied within striking distance of its $108.25 52-week high as CEO Brian Niccol’s turnaround shows up in the numbers, but the easy money has been made.

Starbucks operates 41,129 coffeehouses globally, split roughly evenly between company-operated and licensed stores, with the U.S. and China accounting for 61% of the global footprint.

After four straight earnings misses and a stock that bottomed in the low $80s last October, the “Back to Starbucks” plan delivered an inflection in fiscal Q2 2026 that lifted shares to current levels.

The Turnaround Finally Has Numbers Behind It

Q2 FY2026 was the cleanest quarter Starbucks has reported in years. Adjusted EPS came in at $0.50 against a $0.44 consensus, revenue of $9.53 billion grew 8.79% year over year, and global comparable sales rose 6.2% on 3.8% transaction growth. North America comps accelerated to 7.1%, a level Niccol said reflected transaction strength the chain “hasn’t seen in 3 years.”

The China overhang has been removed. The $13 billion Boyu Capital transaction shifts International toward a high-margin license model, and management raised full-year guidance to non-GAAP EPS of $2.25 to $2.45 with global comps of 5% or better. Wolfe Research upgraded shares to outperform with a $112 price target, and operating income jumped 37.79% year over year.

Valuation Is Pricing In Near-Perfect Execution

The trailing P/E is 74, the forward P/E sits at 32, and the price-to-sales ratio of 2.886 is rich for a low-single-digit revenue grower. FY2025 net income fell 50.64% and operating income dropped 45.71%, leaving a low base that flatters recovery math. Shareholders’ equity is a negative $8.46 billion, reflecting heavy buyback-financed debt.

North America operating margin contracted 170 basis points to 10.2% as labor investments, tariffs, and elevated coffee prices weighed on results. The effective tax rate jumped to 29.8% from 23.5%. China comps grew only 0.5% with a 1.6% ticket decline.

Why Patience Beats Action Here

This is the textbook setup for a Hold. The bull thesis is intact but priced in, and the bear case requires execution to crack. Niccol has guided cautiously while flagging that hitting the high end requires “5% plus comps” plus coffee cost relief. The next two quarterly reports will reveal whether 7%-plus North America comps are sustainable or a one-quarter pop against weak comparisons.

Investors get paid to wait. The $0.62 quarterly dividend marks 64 consecutive quarters of payouts with a 17% historical CAGR, and the 17 recent insider buy transactions suggest leadership sees value.

The Numbers Behind the Call

Shares trade at $102.28 against a consensus analyst target of $106.25, implying roughly 3.9% upside. Of 37 covering analysts, the breakdown skews neutral:

- Strong Buy: 5

- Buy: 12

- Hold: 16

- Sell: 2

- Strong Sell: 2

SBUX is up 22.97% year to date, sharply outpacing the S&P 500’s roughly 8% gain over the same stretch. The stock sits 2% below its 52-week high of $108.25, with a 200-day moving average of $91.39 and beta of 0.977.

The Verdict: A Hold at the High End of the Range

At $102.28, Starbucks is a Hold. The turnaround is real, but the stock has already absorbed it. With shares within 2% of a 52-week high, a forward P/E of 32, and consensus pointing to under 4% upside, the risk/reward demands proof that 6%-plus global comps are durable rather than a comparison-driven bounce.

The trigger for a Buy upgrade is straightforward: a second consecutive quarter of 7%-plus North America comps combined with margin recovery and any sign that China stabilizes under the Boyu structure.

The trigger for a Sell is deceleration toward flat comps, continued ticket weakness, or a North America margin that fails to lap tariff and coffee cost pressure in the back half.

The cost of patience is modest given the 2.6% dividend yield and a base case price target of $105.64. The cost of chasing here is paying a premium multiple for a story whose next chapter is unwritten.

Hold until Niccol shows the second quarter looks like the first.