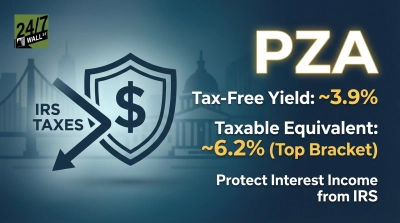

For high earners hunting tax-free monthly income, the Invesco National AMT-Free Municipal Bond ETF (NYSEARCA:PZA) has become a reliable workhorse. PZA pays a 3.65% federal tax-free yield through monthly distributions, and it has now strung together 217 consecutive payments since 2007 without a miss. The question facing income investors is whether that streak rests on durable bond interest or on a yield level that the next leg of the rate cycle could squeeze. The data tilts clearly toward durable.

How PZA Turns Muni Interest Into Monthly Checks

PZA tracks the ICE BofAML National Long-Term Core Plus Municipal Securities Index, a basket of investment-grade municipal bonds issued by U.S. states, cities, school districts, and revenue authorities. The defining filter is the AMT screen: every bond in the portfolio is structured so its interest does not feed the alternative minimum tax calculation. That matters because the 2026 AMT exemption phases out at $500,000 for single filers and $1,000,000 for joint filers, exactly the income tier this fund is built for.

Income flows in one direction. Issuers pay semiannual coupons into the trust, Invesco pools the cash, deducts the 0.28% expense ratio, and distributes the rest monthly. There is no options overlay, no leverage, no return-of-capital game. The yield is bond coupons, full stop.

What Actually Drives Distribution Safety

Three things determine whether PZA’s monthly check holds up: credit quality, the reinvestment yield on maturing bonds, and duration risk.

On credit, the index is restricted to investment-grade issues, and municipal default rates in this tier have historically run a fraction of corporate defaults. A water utility or state general-obligation bond is not Tesla paper. Distribution risk from credit losses is therefore minor.

On reinvestment, the trend is a tailwind. Monthly distributions climbed from a $0.05 to $0.06 range in 2022 to roughly $0.07 across 2026 year to date. The May 2026 payment of $0.07 sits near the top of that band. As older low-coupon bonds mature, Invesco is replacing them with paper issued into today’s higher-rate market, which is feeding the rising distribution.

Duration is where the honest risk lives. The fund holds long-dated bonds, and the 10-year Treasury yield at 4.47% sits in the 91st percentile of its 12-month range. If long rates push back toward the 4.67% peak from May 19, NAV will take a hit even as coupon income keeps flowing. That is price risk, not distribution risk, and the two should not be confused.

Total Return Tells the Honest Story

Yield in isolation flatters this fund. PZA is up 8.4% over the past year and 2.4% year to date, but the five-year price chart is essentially flat at essentially flat. Over ten years the share price is up 20% $23.

Holders made their money from distributions, not capital appreciation, which is exactly what a long-duration muni ETF is supposed to do.

The Verdict and a Cheaper Alternative

The distribution is safe. Coupon income from an investment-grade, AMT-free muni portfolio is among the most predictable cash flows in fixed income, the streak of 18 years of monthly payments is not an accident, and the reinvestment math currently runs in the fund’s favor. The risk to monitor is NAV, not the check.

For investors who want the same AMT-aware muni exposure at a lower cost, the Schwab Municipal Bond ETF (NYSEARCA:SCMB) charges 0.03% against PZA’s 0.28%, a 25 basis point gap that compounds into real money over a decade. PZA earns its higher fee only if its long-duration tilt and AMT-specific construction matter to the holder. For a top-bracket retiree drawing tax-free monthly income, that case still holds. For everyone else, the cheaper alternative deserves a look.

Contact [email protected] for any questions or corrections.