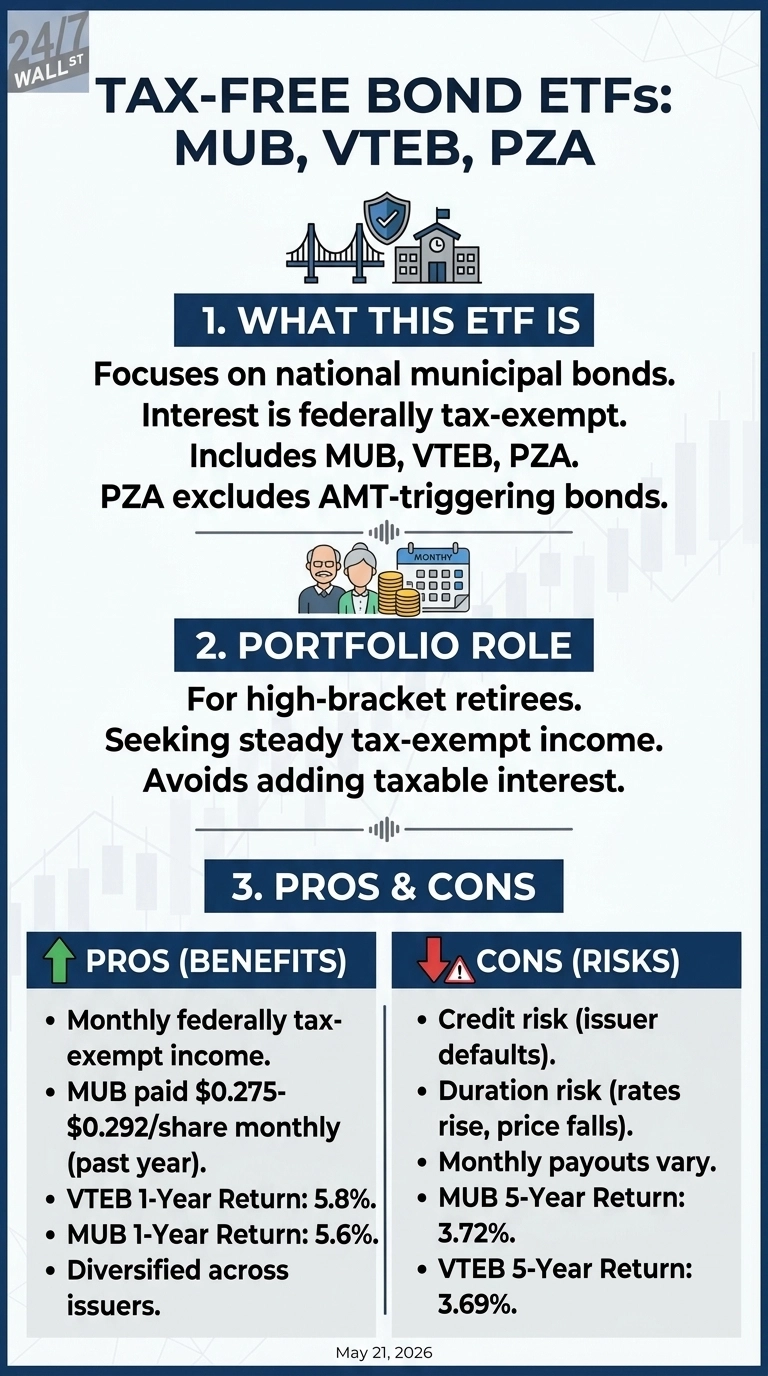

High-bracket retirees face a math problem that taxable bond funds cannot solve: every dollar of interest income gets taxed at the federal marginal rate, often layered with a state tax bite. The iShares National Muni Bond ETF (NYSEARCA:MUB) sits at the center of a three-fund solution that turns roughly $500,000 into about $1,750 a month of federally tax-exempt income. Pair MUB with Vanguard Tax-Exempt Bond ETF (NYSEARCA:VTEB) and Invesco National AMT-Free Municipal Bond ETF (NYSEARCA:PZA) and the combined position generates roughly $21,000 annually without adding to taxable income. For a California retiree in the 32% federal and 9.3% state brackets, that is equivalent to about $35,000 of pre-tax taxable income.

What MUB and Its Peers Actually Do

Municipal bond ETFs hold bonds issued by states, cities, school districts, and authorities. Interest is exempt from federal income tax under IRS Publication 550 and is frequently exempt from state tax if the bond is issued in the holder’s home state. MUB tracks the broad investment-grade national muni market. VTEB does roughly the same thing at Vanguard. PZA layers in a filter that excludes bonds whose interest can trigger the federal Alternative Minimum Tax, making it cleaner for higher earners who occasionally brush against AMT.

The return engine is simple: monthly coupon income from thousands of underlying issuers, with modest price movement tied to interest rates. MUB has paid between $0.275 and $0.292 per share each month over the past year. Current SEC yields run roughly 3.45% on MUB, 3.54% on VTEB, and 3.67% on PZA.

Does the Math Hold Up?

This exact cross-section is where tax-equivalent yield calculations truly matter. With the 10-year Treasury note hovering near 4.61%, a fully federally taxable bond alternative looks highly competitive on the surface. Yet for a high-income California retiree facing a steep 41% combined marginal tax bracket, a modest 3.54% tax-free yield translates to an equivalent taxable return of roughly 6.0%. Absolutely no sovereign Treasury or investment-grade corporate credit fund reliably delivers that risk-adjusted hurdle today.

Comprehensive total-return data paint a far more sober picture. MUB generated a 4.07% return over the past year but only a 3.72% cumulative advance across five years, capturing the severe fixed-income bear market of 2022 and 2023. VTEB has performed nearly identically, printing a 5.77% gain over one year and a 4.54% advance over five years. Across a full decade, MUB delivered approximately 21.36%. Wealth allocators who required aggressive principal growth got heavily punished. Conversely, retirees who strictly required predictable monthly checks received exactly what they originally signed up for.

The Tradeoffs Retirees Should Price In

- Credit risk is real. Detroit and Puerto Rico both defaulted on municipal debt over the past decade. ETF diversification across more than 1,000 issuers cushions individual blowups, but a credit-cycle stress event can still pressure NAVs.

- Duration risk. MUB’s price fell when rates rose, and the 10-year yield sits at the 98th percentile of its 12-month range. Further rate spikes would cut NAV before higher coupons rebuild it.

- Yields are not contractual. The $1,750-a-month figure assumes today’s distribution levels. Monthly payouts have varied within a roughly 5% band over the past year, and the forward number depends on bond reinvestment rates.

Who This Three-Fund Sleeve Fits

The MUB-VTEB-PZA combination earns its place in a portfolio for a high-bracket retiree, especially one in a high-tax state, who wants a steady monthly income without adding taxable interest to Social Security and required minimum distributions. California or New York residents may further improve the tax math by swapping in a state-specific fund, such as iShares California Muni Bond ETF (NYSEARCA:CMF) or iShares New York AMT-Free Muni Bond ETF (NYSEARCA:NYF). Anyone in the 12% or 22% federal tax bracket should consider taxable bond funds instead. The tax-exempt premium is paid only when the marginal rate is high enough to justify the lower headline yield.

Contact [email protected] for any questions or corrections.