AppLovin (NASDAQ:APP | APP Price Prediction) has had a wild ride in 2026. After a blistering 2025 that pushed shares higher, the stock has cooled meaningfully, leaving investors wondering whether the AI ad-tech story is broken or simply digesting gains. My read leans toward the latter, and the 24/7 Wall St. price target reflects that.

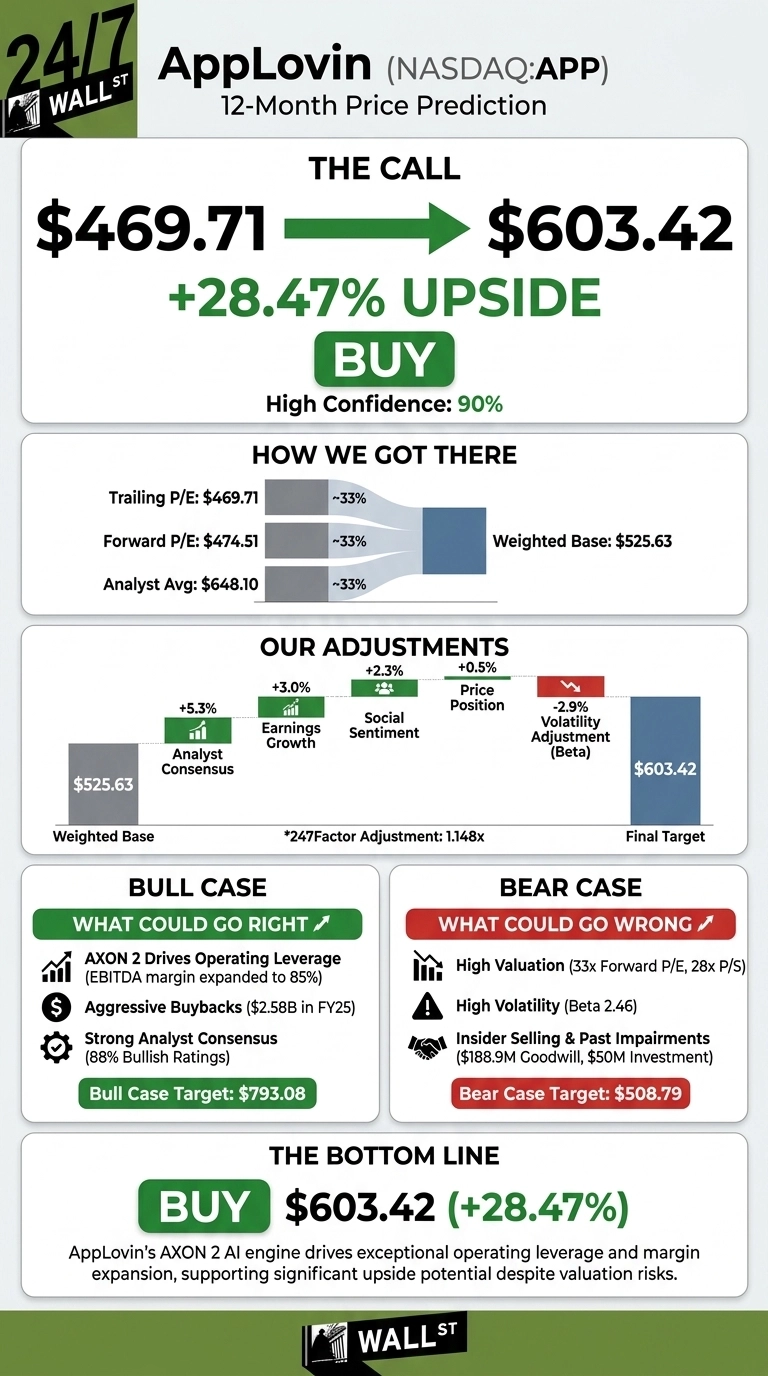

Our price target for AppLovin is $603.42, implying roughly 28.47% upside from the current price of $469.71. The recommendation is buy at a 90% confidence level, which is among the highest readings our model assigns.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $469.71 |

| 24/7 Wall St. Price Target | $603.42 |

| Upside | 28.47% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Volatile 2026 Has Reset Expectations

AppLovin is down 30.29% year to date, with shares slipping 1.85% over the past week and sitting 13% below the 52-week high of $745.61. Over a one-year window, however, the stock is still up 36.4%, and the five-year return of 432.49% reflects the payoff from the company’s pivot to a pure-play ad-tech model powered by the AXON 2 AI engine.

The fundamentals remain exceptional. Q1 FY26 revenue of $1.84B rose 24.15% YoY and beat estimates, while EPS of $3.56 topped the $3.46 consensus. Operating income jumped 117% YoY to $1.44B at a 78% margin, and the team returned $1B to shareholders through buybacks in the quarter.

Why Bulls See a Breakout Ahead

The bull case rests on AXON 2’s operating leverage. Adjusted EBITDA margin expanded from 81% in Q2 2025 to 85% in Q1 2026, and Q2 2026 guidance calls for revenue of $1.915B to $1.945B at 84-85% EBITDA margins. Free cash flow of $3.95B in FY25 funds aggressive buybacks, with 6.4M shares retired for $2.58B last year.

With 7 Strong Buy and 21 Buy ratings against just 4 Holds, the Street is loud. Our bull case scenario points to $793.08 over the next year, a 68.84% total return, if e-commerce ad expansion accelerates.

The Risks Worth Watching

The bear case starts with valuation. APP trades at a forward P/E of 33x and a P/S of 28x. A beta of 2.46 means any AI sentiment crack hits hard. Insider activity skews to selling across 165 transactions, and FY25 included a $188.9M goodwill impairment plus a $50M investment writedown.

Bulls would counter that these charges tie back to the Apps divestiture to Tripledot Studios for $400M cash plus 20% equity, a cleanup move that sharpens the pure-play ad-tech focus. Our bear case still nets a $508.79 target.

AppLovin Price Prediction 2026-2030

The 24/7 Wall St. price target of $603.42 with 90% confidence keeps me constructive. The decisive factor is operating leverage: net margin expanded to 65% while revenue grew 24%.

The constructive case strengthens if AXON 2 continues compounding ad pricing and impressions into 2027. The thesis weakens if forward guidance signals deceleration below 20% growth or if the e-commerce vertical disappoints.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $603 |

| 2030 | $969 |

These projections assume AppLovin continues executing on AXON 2 monetization and e-commerce ad expansion. Significant upside could come if connected TV ad share grows materially, while downside risk centers on platform policy shifts at Apple or Google.

Contact [email protected] for any questions or corrections.