The headline number for this article is $180, and I want to address it head on before anyone scrolls further.

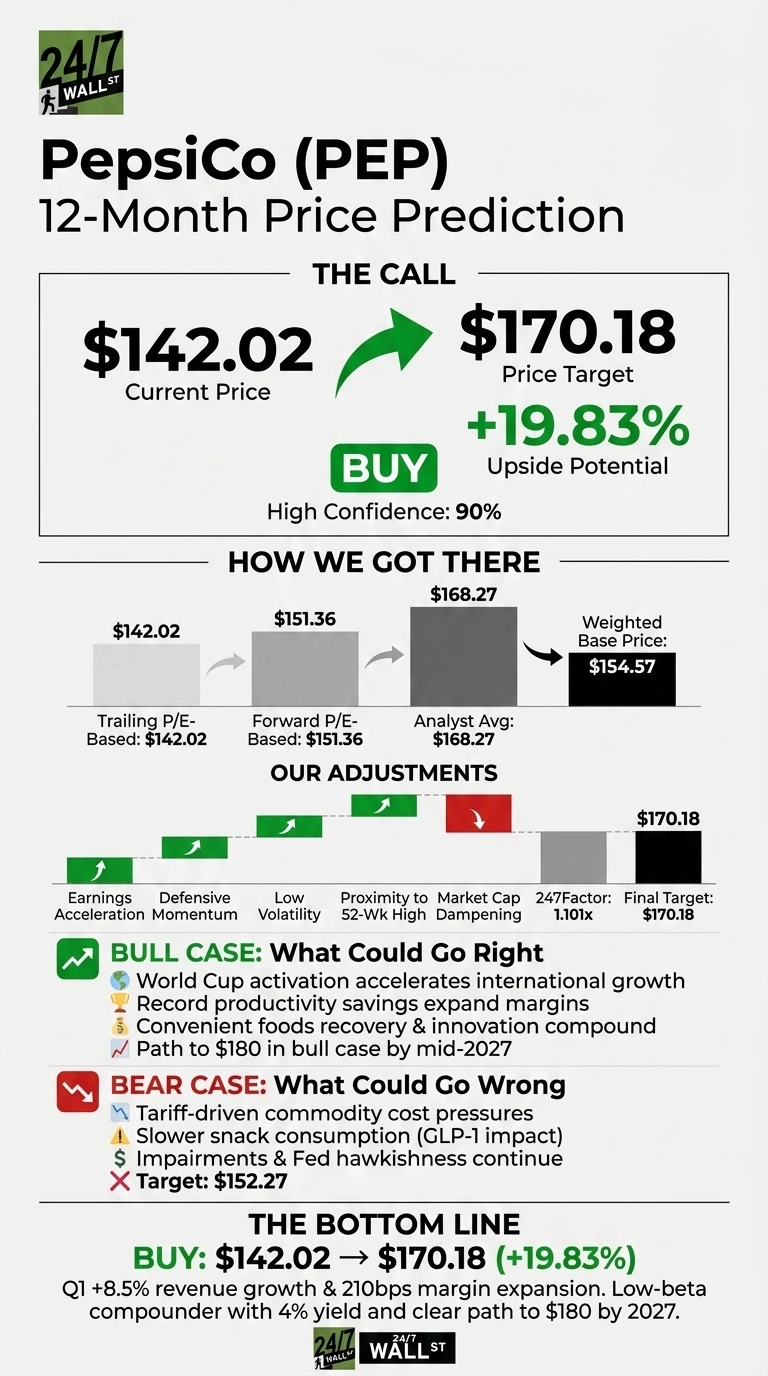

Our proprietary 24/7 Wall St. price target for PepsiCo (NASDAQ:PEP | PEP Price Prediction) is $170.18 over the next 12 months, with a clear path to $180 in the bull case as the World Cup activation, productivity savings, and convenient foods recovery compound through 2027. With shares at $142.02, that base case implies 19.83% upside.

| Metric | Value |

|---|---|

| Current Price | $142.02 |

| 24/7 Wall St. Price Target | $170.18 |

| Upside | 19.83% |

| Research View | Constructive |

| Confidence Level | 90% |

A Defensive Name That Just Went on Sale

PEP has fallen 4.42% over the past 30 days and 1.19% in the last week, partly reflecting hawkish Fed commentary that dimmed appetite for dividend stocks. Zooming out, shares are up 14.55% over the past year and Pepsi remains a Consumer Defensive anchor with a beta of 0.359.

Q1 FY2026 delivered core EPS of $1.61 on revenue of $19.44 billion, a 8.5% year-over-year gain. Operating margin expanded 210 basis points to 16.5%, and management reaffirmed full-year organic revenue growth of 2% to 4%. The next earnings catalyst lands on July 9, 2026.

Why Bulls See $180 by Mid-2027

Piper Sandler maintains an Overweight rating with a $178 price target, while TIKR’s longer-term model points to $208 by December 2030. Our bull case scenario lands at $177.28 by June 2027, with the $180 mark within reach if Q2 and Q3 earnings extend the Q1 beat streak.

Growth drivers are tangible. CEO Ramon Laguarta noted that PBNA grew 9% in Q1, and international markets are accelerating around the 2026 World Cup activation. PFNA added 300 million new consumption occasions versus the prior year.

Laguarta stated: “We’ve seen momentum in PBNA, both organic and reported…And sequential growth in PFNA.” Add a $10 billion buyback authorization, the 54th consecutive dividend hike, and active institutional buying, and the bull math works.

The Risks Worth Watching

Tariff-driven commodity costs hit PBNA with an 11 percentage point impact in Q4 25, and FY25 operating income fell 19.57% on Rockstar and Be & Cheery impairments totaling $1.993 billion. Volume softness in convenient foods and slower snack consumption tied to GLP-1 adoption could pressure organic growth toward the bottom of the 2% to 4% range. Our bear case scenario stops at $152.27.

The FY25 impairments were one-time charges. Operating cash flow still came in at $12.087 billion, with FCF conversion guided above 80%. Bulls argue the impairments reflect aggressive portfolio cleanup rather than core business deterioration.

PepsiCo Price Prediction 2026-2030

The 24/7 Wall St. price target stands at $170.18 with 90% model confidence. Q1 delivered +8.5% revenue growth and a 210 bp margin expansion, yet shares trade closer to the 52-week low than the high.

The setup looks constructive for a low-beta compounder with a 4% yield and a clear path to $180 by 2027. The thesis weakens if Fed hawkishness continues penalizing dividend payers through the back half of 2026.

Here is where our model projects PEP could trade, assuming current growth trajectories and margin recovery hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $156 |

| 2027 | $180 |

| 2028 | $202 |

| 2029 | $224 |

| 2030 | $247 |

These projections assume PEP continues executing the productivity and innovation strategy Laguarta outlined, with the World Cup activation and poppi integration supporting beverage growth.

Significant upside or downside could result from sustained commodity inflation, faster-than-expected GLP-1 impacts on snack volumes, or larger buyback execution against the new $10 billion authorization.

Contact [email protected] for any questions or corrections.