At $116.56, Strategy Inc. (NASDAQ:MSTR | MSTR Price Prediction) looks vulnerable, with dilutive equity issuance colliding with a hawkish incoming Fed under Kevin Warsh setting up a potential path back toward $65. The stock has lost 68.93% of its value over the past year, and Michael Saylor’s resumed bitcoin buying has not arrested the slide.

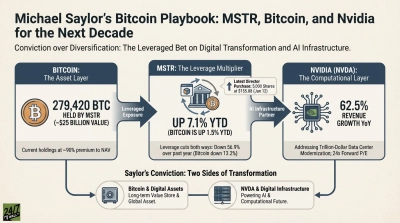

Strategy, the rebranded MicroStrategy run by CEO Phong Le with Saylor as Executive Chairman, pairs a small enterprise software business with the largest corporate bitcoin treasury in the world, now 818,334 BTC. Q1 was crushed by a $14.46 billion unrealized loss on digital assets under ASU 2023-08 fair-value accounting, producing EPS of -$38.25 against a -$18.98 consensus. With bitcoin off its January high and the Fed about to turn over, the question is what holds this equity up.

The Bull Pitch: A Capital Markets Machine That Still Works

Saylor argues the capital flywheel is healthier than ever. Strategy has raised $11.68 billion year to date, roughly half via common equity and half via the STRC preferred, which carries an $8.5 billion notional value, $375 million in daily trading volume, and 3% volatility achieved during a bitcoin bear market.

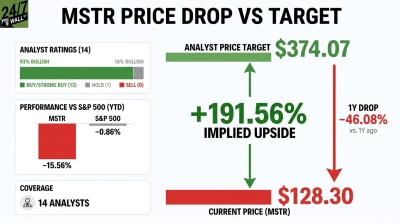

The underlying software business is accelerating, with subscription services revenue up 58.7% year over year to $58.88 million. Saylor told analysts the average MSTR price target is about $323, and prediction markets place 92.5% odds on another bitcoin purchase being announced this week. Bulls argue the discount to NAV will not persist.

The Bear Pitch: Dilution, Dividends, and a Hawkish Fed

Fair-value accounting drags every bitcoin drawdown straight through GAAP earnings. The $12.54 billion Q1 net loss proves it. Strategy carries $8.17 billion in long-term debt and $229.53 million in quarterly preferred dividend obligations that grow with every STRC issuance.

The ATM program funding bitcoin purchases is dilutive to common shareholders. Prediction markets give a 57% probability of MSCI delisting by year-end, a forced-seller event. Saylor conceded on the call that “When we go to a restrictive monetary policy, that is bad for Bitcoin, really bad for Bitcoin.” Warsh’s first meeting as Fed Chair is the catalyst bears are pointing at.

The Hold Pitch: Waiting for the Fed and the Bitcoin Print

Patient investors note the capital machine is running, software is growing, and crowd-implied margin-call risk sits at only 7%. The base case is that Strategy survives even if the equity wobbles. The open question is whether the next move comes from a Warsh dovish surprise that rekindles bitcoin or a hawkish hold that triggers another leg lower.

What the Numbers Say at Current Levels

MSTR trades at $116.56 with a market cap near $39.1 billion. The stock is down 23.29% year to date and 30.05% in the past month, against an S&P 500 up 8.66% year to date and 24% over the past year.

Management cited an average analyst price target near $323, implying roughly 80% upside if hit, though targets are one data point and most were set when bitcoin was meaningfully higher than today’s $64,617.

The Verdict: A Bearish Setup Toward $65

At $116.56, Strategy Inc. looks bearish on a risk-reward basis.

Three converging headwinds drive further downside. The at-the-market equity machine funding bitcoin purchases mechanically dilutes common holders, and Saylor confirmed the company will keep pressing it. Warsh’s first Fed meeting is unlikely to deliver the dovish pivot bitcoin needs after the slide from the $92,807.99 January peak. A 57% market-implied probability of MSCI delisting introduces a forced-seller dynamic disconnected from fundamentals.

The risk-reward at $116 is unattractive. Saylor’s breakeven math requires bitcoin to compound above 2.27% annually just to keep the dividend stack solvent indefinitely, and the convertible note overhang remains. A retreat to $65 would mark MSTR back to where it traded five years ago, before the leverage stack ballooned.

The thesis breaks if Warsh signals a fast cutting cycle, bitcoin reclaims $90,000, and the STRC dilution pace cools. Until those three line up, the risk-reward looks unfavorable. Investors tracking the name should monitor Warsh’s policy signals and watch for a retest near $65.