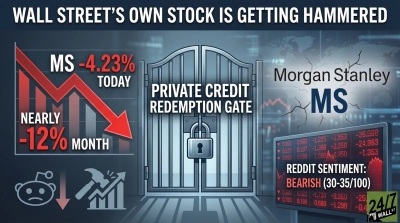

Private credit was supposed to be the safe, sleepy corner of finance where pension money quietly clipped coupons. That story is fraying. Morgan Stanley (NYSE:MS | MS Price Prediction) just capped investor withdrawals at 5% from its $7 billion private credit fund, and Apollo Global Management (NYSE:APO) is again limiting redemptions from its largest non-traded retail private credit fund.

Withdrawal requests across the $1.8 trillion private credit market have spiked this quarter, and on Bloomberg Businessweek, Len Tannenbaum, the founder of Tannenbaum Capital Group who built Fifth Street Capital to roughly $5 billion before selling it to Oaktree in 2017, says the redemption gates are just the beginning.

Why Tannenbaum thinks the stress is structural

Tannenbaum’s argument is that the cracks showing up at Morgan Stanley and Apollo are the predictable result of how the asset class scaled. A wave of direct loans was originated in the 2021 and 2022 zero-rate era, underwritten without accounting for the rate hikes that followed. Those borrowers now have to refinance into a very different curve. As of June 24, 2026, the five-year Treasury yields 4.15% and the 10-year sits at 4.38%, with the 30-year at 4.85%. Layer a private credit spread on top of that, and a software company that borrowed at maybe 7% all-in now faces a refinancing closer to double digits.

What happens when the math no longer works? According to Tannenbaum, the loan gets quietly restructured. Troubled software loans are being converted into PIK securities, meaning the borrower pays interest with more debt rather than cash.

Non-accruals are creeping up. The headline NAV barely budges because the manager remarks the loan at a small discount and keeps moving. The redemption queue at the retail vehicles is what forces the issue out into daylight.

The marks problem

Tannenbaum is blunt about the marks. BDC and non-traded fund managers are carrying private loans at marks between 70 and 90 cents on the dollar, and he doubts those marks would survive a real bid. He borrowed a line from Goldman Sachs to make the point. “If you really want to find a price, sell 10% and I’ll tell you what the price is.” The scale of the disclosure gap is visible in BDC quarterly filings such as Apollo’s 10-Q filings with the SEC, where Level 3 fair-value inputs dominate the loan book.

The industry’s own outlooks tiptoe around the same anxiety. Goldman frames recent blowups at First Brands, Tricolor, and Cantor Group as “isolated, idiosyncratic occurrences, not indicators of rising systemic credit risk”, while still flagging that US banks carry roughly $360 billion of private equity and private credit loans, about 11% of their total loans.

JPMorgan’s 2026 view echoes that the September defaults “appear to be isolated to issuer-specific concerns and the auto sector rather than signaling broader systemic risks” while quietly conceding that “pockets of risk may exist” as spreads have compressed. Tannenbaum’s read is that the pockets are bigger than the brochures suggest, and a canary in the coal mine is coming.

The contrarian trade he’s actually making

The warning has a twist. Tannenbaum is leaning further in. He is launching a new BDC focused on lower-middle-market deals with $5 to $25 million of EBITDA, the slice of the market the mega-funds find too small to bother with. His pitch is that the next two years are “a great vintage” precisely because the legacy book is impaired. Spreads widen when capital gets scared. Covenants tighten when borrowers run out of lenders. New money written today, on tougher terms, against companies that have already survived the rate reset, looks structurally different from a 2021 unitranche.

That is the trade hidden inside the warning. The same conditions choking off redemptions at Morgan Stanley and Apollo, the refinancing wall, the suspect marks, the PIK creep, are what make new capital powerful. The Goldman 2026 outlook makes a similar point in softer language, calling for “rigorous underwriting and surveillance in private credit” as the price of staying in the game. For investors watching the gated funds and wondering what to do, the question is whether you trust the marks on what you already own. Tannenbaum’s answer, expensive as it sounds, is to find out by trying to sell some.

Contact [email protected] for any questions or corrections.