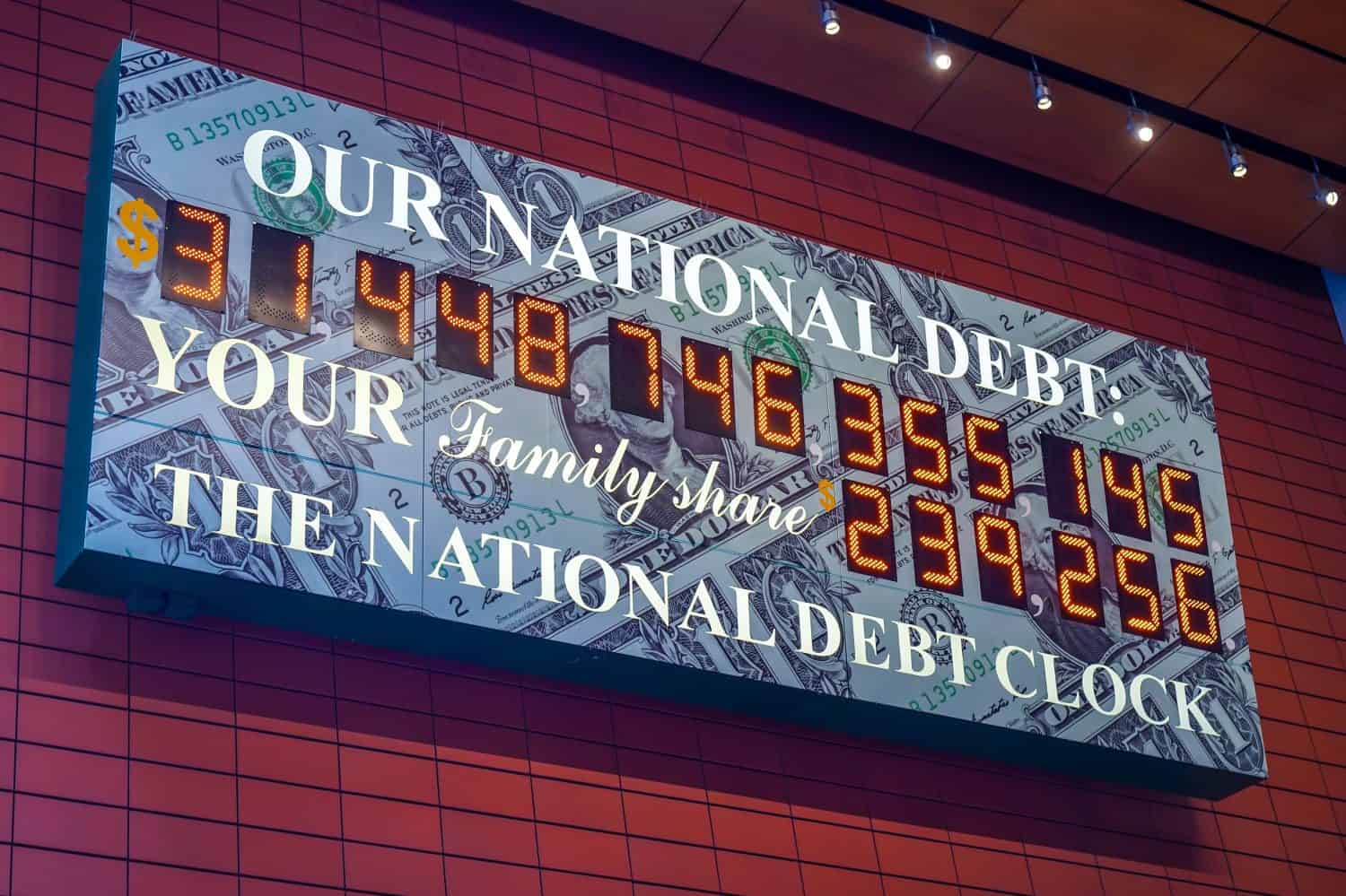

The last time America’s debt ratio crossed 100% of GDP, Harry Truman was in the White House and the country was still paying off World War II. It happened again on March 31 of this year, when the Treasury reported publicly held debt of $31.265 trillion against a trailing GDP of $31.216 trillion. The Wall Street Journal called the resulting 100.2% ratio a milestone the country would likely climb past for the foreseeable future because the federal government is running historically large annual deficits of nearly 6% of GDP.

That prediction is already playing out. Total federal debt has now reached $39.4 trillion, up $3.2 trillion in the last 12 months and $16.3 trillion since 2020. At the current pace, $50 trillion arrives before 2030.

What the Number Actually Means for Your Household

National debt has concrete household consequences. Here is what is happening:

- Debt level: $39.4 trillion, above 100% of GDP for the first time since 1946.

- Growth rate: Roughly $3.2 trillion added per year, or about $260 billion per month.

- Cost to service it: Treasury interest payments now run near $3 billion per day, on track to top $1 trillion in fiscal 2026.

- Household backdrop: The federal debt story is landing against a household sector with less cushion. The personal saving rate has fallen from 6.2% in early 2024 to 3.9%, while consumer sentiment remains weak by historical standards and close to recession-like levels. That leaves consumers more exposed to higher borrowing costs, sticky prices, and any wobble in the labor market.

The pain arrives through interest rates. Every dollar of new Treasury issuance must be sold at a market-clearing yield, and that yield feeds into the borrowing costs banks charge on mortgages, auto loans, and credit cards. The 10-year Treasury is sitting at 4.58% and the 30-year at 5.08%, even after the Fed cut its policy rate to 3.75% late last year. The long end of the curve is telling you what investors now demand to finance the debt trajectory.

The One Financial Reality That Drives This

The single force that makes rising debt dangerous is the compounding of interest expense on a floating rate stack. Roughly a quarter of the debt rolls over every year. When maturing bonds issued at 1% to 2% get refinanced at today’s 4.58% 10-year yield, the interest bill jumps mechanically, even before Congress adds another dollar of new spending.

So $39 trillion at a blended 3.5% costs roughly $1.37 trillion a year in interest. Push the blended rate to 4.5% as old low-coupon debt runs off, and the annual bill climbs closer to $1.76 trillion. That extra money has to come from somewhere. It flows from more borrowing, which can pressure yields higher, which raises the next refinancing cost. That is the loop.

Post-WWII, the country grew and inflated its way out. Nominal GDP outpaced debt. Today the setup is harder. Core PCE inflation is running at the 90.9th percentile of its historical range, so the Fed cannot let inflation rip without risking a bond-market backlash. GDP grew only 2.1% in Q1 2026, and quarterly growth has swung from 4.4% to 0.5% in the last four readings. Growth cannot be counted on to outrun the interest curve.

Three Moves That Actually Change Your Outcome

None of this requires a crystal ball, just a few structural changes made before conditions force them.

- Lock in fixed rates on liabilities, float on assets. If long-end yields keep drifting higher as debt piles on, variable-rate borrowers get hurt first. Refinancing a mortgage or consolidating credit card balances at 2.92% delinquency rates is easier now than during a bond market wobble. Cash and short Treasuries still yield 3.84% to 4.02% on the front end.

- Rebuild the savings buffer. A 3.9% household savings rate leaves almost no cushion for a job loss during fiscal stress. Getting three to six months of expenses in a money market fund earning close to 4% is the highest-leverage move most households can make this year.

- Consider inflation hedges inside retirement accounts. If Washington’s exit ramp ends up being higher inflation, real assets and TIPS behave differently than nominal bonds. M2 money supply has climbed from $22.02 trillion to $23.05 trillion in 12 months, sitting in the 90.9th percentile of history.

For readers thinking about how the fiscal picture reshapes retirement math, our Retiree’s Tax Trap Map walks through how rising deficits typically get resolved through the tax code.

The Takeaway Worth Acting On

Most households treat national debt as political theater and adjust nothing in their own finances. That is the mistake. The debt curve is not slowing, the interest cost is rising, and the market is already pricing it in through a 5.08% 30-year yield. Fix your borrowing costs while you can, hold more cash than seemed necessary in 2021, and stop assuming the low-rate world of the last decade is coming back. The rate at which debt refinances is what ultimately tightens the vise.

Contact [email protected] for any questions or corrections.