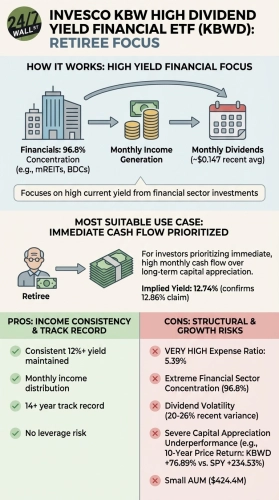

The Invesco KBW High Dividend Yield Financial ETF (NASDAQ:KBWD) is the income vehicle of choice for investors who want double-digit yields from financials without picking individual business development companies (BDCs) and mortgage REITs themselves. KBWD bundles the highest-yielding names in the sector, including BDCs, mortgage REITs, and asset managers, into one monthly-paying wrapper. With KBWD trading at $12.09 and down about 5% year to date, the question for holders is whether that headline yield actually compensates for what is happening underneath, or whether the distribution is masking real erosion.

How KBWD Manufactures Its Yield

KBWD tracks the KBW Nasdaq Financial Sector Dividend Yield Index, which screens for the highest-yielding U.S.-listed financial stocks. The fund’s distribution is simply a pass-through of dividends it collects from holdings like Ares Capital (NASDAQ:ARCC | ARCC Price Prediction), AGNC Investment (NASDAQ:AGNC), Main Street Capital (NYSE:MAIN), and Prospect Capital (NASDAQ:PSEC). That means KBWD’s distribution is only as durable as the weakest dividends inside it, and the dispersion among those names is enormous.

The Four Holdings That Tell the Story

Ares Capital, the largest BDC in the portfolio, looks solid. Q1 2026 net investment income of $0.55 per share comfortably covered the $0.48 quarterly dividend, which has now held steady for 12 consecutive quarters. Non-accruals ticked up to 2.1% at amortized cost and NAV slipped to $19.59, but with $6 billion in available liquidity and a yield of 10.7%, ARCC’s payout is well-supported and carries a cushion to absorb credit slippage.

Main Street Capital is the cleanest story in the bunch. Distributable net investment income of $1.00 per share in Q1 26 covered both the $0.78 regular quarterly dividend and the $0.30 supplemental, marking the 19th consecutive quarter MAIN has paid a supplemental. The base yield is a more modest 6.1%, but the dividend has never been cut in 16+ years of data. NAV ticked up to $33.46. This is the kind of holding that anchors KBWD’s credibility.

AGNC is where the story gets thinner. The agency mortgage REIT yields 13.7% on a $0.12 monthly distribution, but Q1 26 produced a net loss of $0.17 per share and tangible book value fell about 6% to $8.38. The company also issued 38 million shares via its ATM program, diluting existing holders. AGNC has cut before, slashing from $0.16 to $0.12 in March 2020, and the current payout sits uncomfortably close to earnings power. With the 10Y-2Y spread compressed to 0.31% from 0.74% in February, the spread environment is tightening.

Prospect Capital is the warning flare. PSEC cut its monthly distribution from $0.045 to $0.035 effective May 27, 2026, the second reduction in 16 months. NAV per share collapsed from $7.84 to $6.05 year over year, the portfolio shrank from 114 to 89 companies, and PSEC trades at 0.38x book, the market’s verdict on the income story.

Total Return and Macro Backdrop

KBWD’s five-year price return of about 2% tells you the high yield has largely been a return-of-capital experience for many holders. With the Fed Funds rate now 3.75%, floating-rate BDC income is compressing, while the 10-year Treasury at 4.41% keeps refinancing costs elevated.

Half the Portfolio Pays From Cash Flow, the Other Half Is One Shock From Cuts

KBWD’s distribution is sustainable in aggregate but structurally lumpy. Roughly half the portfolio (the ARCC- and MAIN-quality tier) pays from real cash flow with cushion. The other half (PSEC-style and AGNC-style names) is one credit cycle or one rate shock away from cuts that flow straight through to KBWD’s monthly payout. For income-focused portfolios, KBWD’s structure functions more like a satellite sleeve than a core holding, and pairing it with a lower-yield, dividend-growth vehicle is one way investors have historically balanced total return against headline yield.

Contact [email protected] for any questions or corrections.