Broadcom (NASDAQ: AVGO | AVGO Price Prediction) and NVIDIA (NASDAQ: NVDA) just delivered fresh AI semiconductor reports that point in similar directions but reveal very different business models.

NVIDIA closed Q1 FY2027 on May 20, 2026, and Broadcom followed with Q2 FY2026 on June 3, 2026. One sells branded GPUs to everyone. The other designs custom silicon for a handful of hyperscalers.

Custom Silicon Surges, Merchant GPUs Still Dwarf Everyone

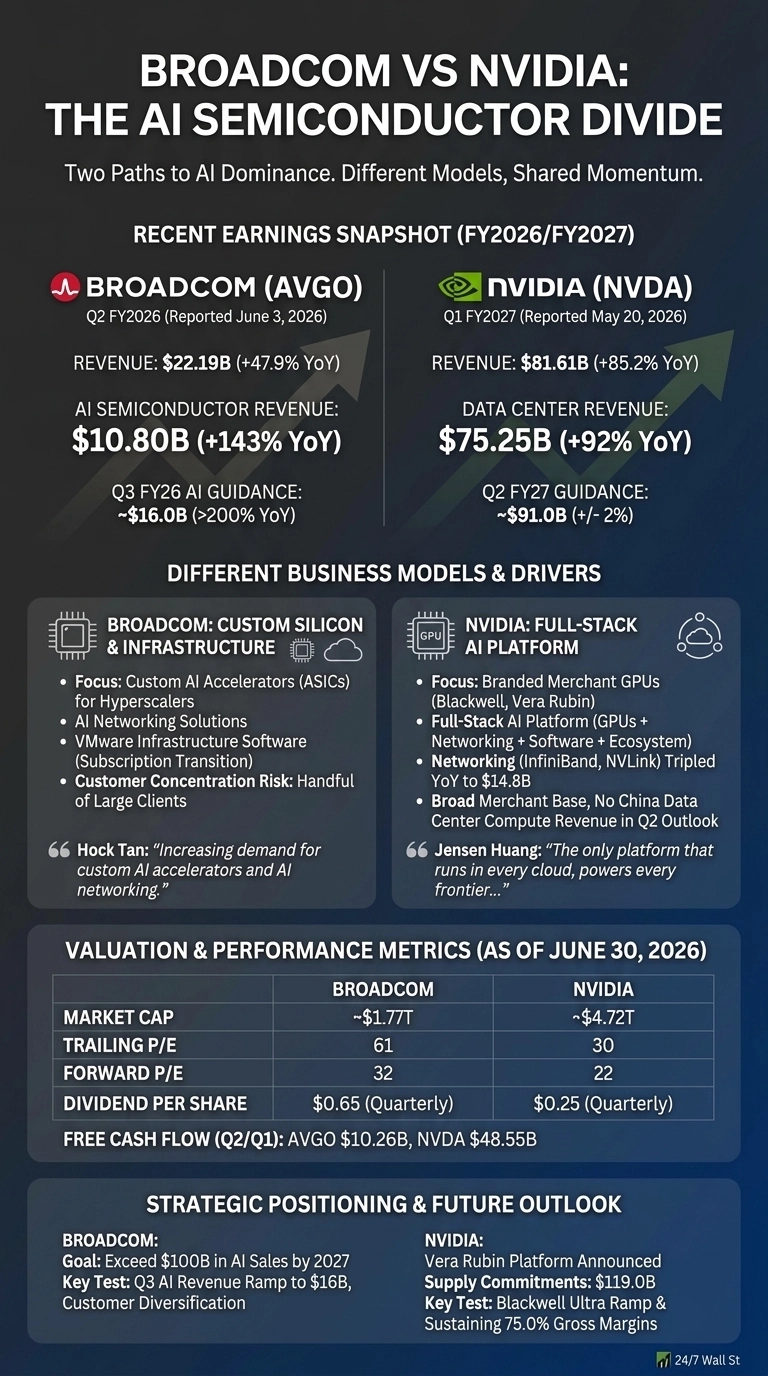

Broadcom posted $22.187 billion in revenue, up 47.9% YoY, with AI semiconductor revenue hitting $10.80 billion (+143% YoY). Hock Tan attributed the result to “increasing demand for custom AI accelerators and AI networking”, and guided Q3 AI semis to $16 billion, a triple-digit jump. The Infrastructure Software segment, anchored by VMware, added $7.178 billion at 9% growth, providing a steady subscription base.

NVIDIA operates at a different scale entirely. Data Center revenue alone reached $75.246 billion, up 92% YoY, with networking products tripling to $14.8 billion. Jensen Huang described the AI buildout as the largest infrastructure expansion in human history and pointed to Blackwell Ultra ramping at full speed. Q2 guidance landed at $91 billion, excluding any China Data Center compute.

| Business Driver | Broadcom | NVIDIA |

| AI Revenue (latest quarter) | $10.80B | $75.25B Data Center |

| Software Anchor | VMware subscriptions | CUDA ecosystem |

| Customer Pattern | Few large hyperscalers | Broad merchant base |

One Bets on Customization. One Owns the Platform.

Broadcom wins by becoming indispensable to specific customers. Designing custom ASICs alongside Google, Meta, and others gives Tan a path to his stated goal of exceeding $100 billion in AI sales by 2027. That model trades volume risk for concentration risk. Lose one mega-customer and the math gets ugly fast.

NVIDIA’s playbook looks broader. Huang called the company “the only platform that runs in every cloud, powers every frontier and open source model, and scales everywhere AI is produced”.

The Vera Rubin platform, Spectrum-X networking, and a deepening partner list (Google Cloud, Anthropic, Meta, Marvell) keep the moat wide. The cost: China revenue has effectively vanished from Data Center compute, and supply-related commitments now total $119.0 billion, a meaningful cash bet.

Valuation tells its own story. AVGO trades at 61 trailing earnings and 32 forward. NVDA sits at 30 trailing and 22 forward, with a far heavier profit base.

The Next Test Is Customer Concentration Versus China

I will be watching whether Broadcom’s Q3 AI ramp to $16 billion actually lands, and whether more than two or three hyperscalers contribute. For NVIDIA, the question is whether Blackwell Ultra and the Vera Rubin rollout can offset the China gap while sustaining 75% gross margins.

AVGO is down 16.5% over the past month and NVDA 7.55%, so the AI trade is clearly cooling. Hyperscaler capex commentary in July is the next data point worth tracking for both names.

How The Setup Frames Up From Here

On scale, NVIDIA leads decisively, with a software moat that keeps compounding and a forward multiple that looks reasonable relative to 85.2% revenue growth.

Broadcom’s profile looks more like a complement. The custom ASIC story is real, and Tan’s execution has been clean across 8 consecutive quarters of EPS beats, though the concentration risk and richer multiple are worth weighing.

For income-oriented investors, Broadcom’s $0.65 quarterly dividend stands out. Hyperscaler capex commentary this summer will be the key swing factor for both names.

Contact [email protected] for any questions or corrections.