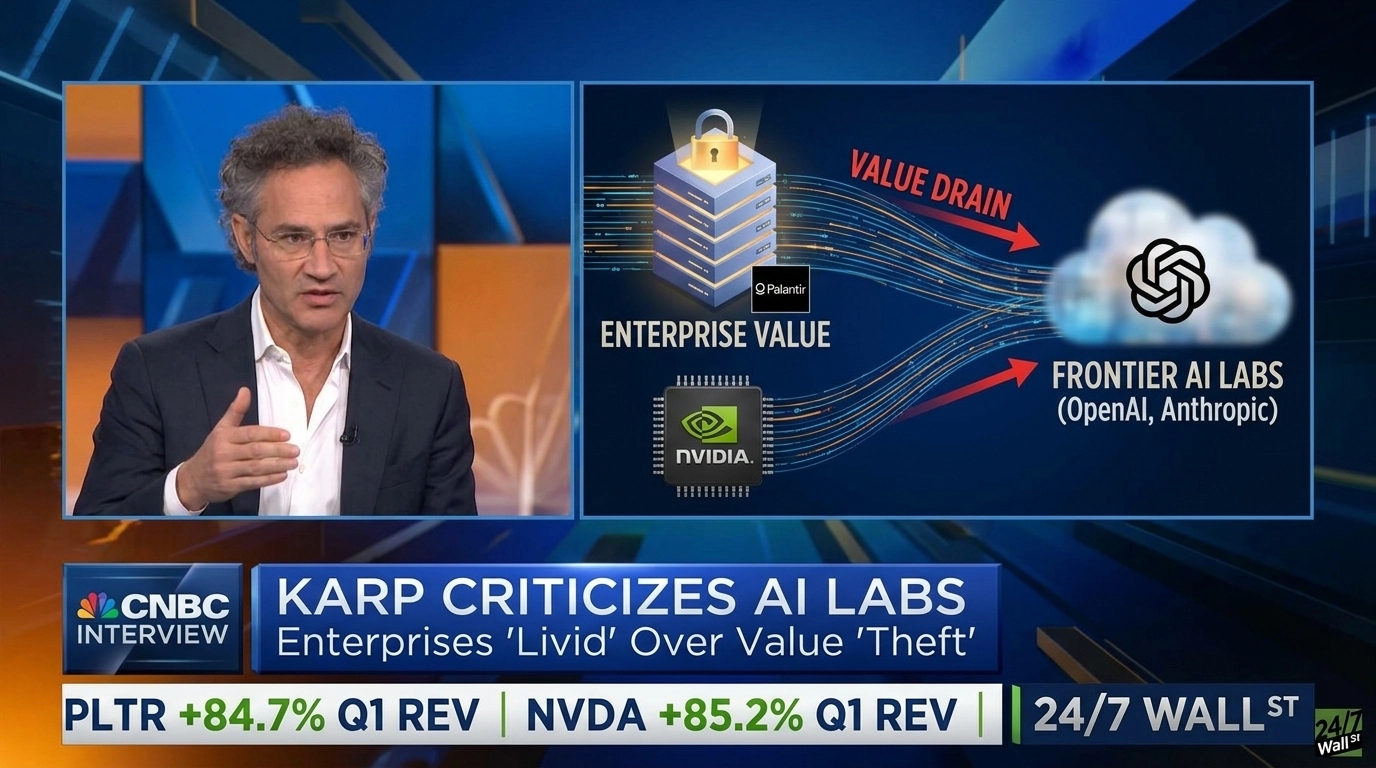

Palantir CEO Alex Karp recently appeared on CNBC to sharpen his critique of frontier AI labs, arguing that enterprises deploying models from OpenAI and Anthropic are “livid” about how much proprietary value flows to model providers. Karp framed the new Palantir partnership with NVIDIA as a direct response, positioning the two companies as the operational stack that lets enterprises control their own data, weights, and business logic.

Karp Says Enterprises Have A Trust Problem

Karp claimed enterprises using frontier models feel they are “paying for tokens that create no value” while handing over proprietary IP and “alpha” to third parties. He described that dynamic as “stealing” business value and a “wealth tax” on companies using AI to generate operational returns.

That framing extends what Karp has previously called “commodity cognition,” the view that model quality is converging while operational leverage accrues to whoever owns the deployment layer. He positioned Palantir’s ontology and application layer, combined with NVIDIA infrastructure, as giving enterprises ownership of “the means of production” for AI, especially in critical-infrastructure settings where data control is non-negotiable. He asserted Palantir has more demand than it can supply and pointed to roughly $15-$18 billion in free cash flow two years out as validation of the model-plus-application-layer approach despite market skepticism.

Palantir’s Growth Story Backing CEO Karp’s Claims

Palantir (NASDAQ:PLTR | PLTR Price Prediction) reported Q1 2026 revenue of $1.63 billion, up 84.7% year over year, with adjusted EPS of $0.33 against a $0.28 estimate. U.S. commercial revenue reached $595 million, up 133% year over year, and the company closed 206 deals of at least $1 million, with a total contract value of $2.41 billion. Management raised full-year 2026 revenue guidance to a range of $7.65 billion to $7.66 billion, implying 71% growth.

On the earnings call, Karp said, “Palantir’s Rule of 40 score has soared to 145%. We have shattered the metric, a feat matched only by other fellow AI infrastructure companies: NVIDIA, Micron and SK Hynix.”

PLTR trades at $126.87, down 34.36% year to date and 25.47% over the past month. On a five-year view, shares are still up 371.97%. The valuation remains stretched at a forward P/E near 74x, which explains why Karp keeps invoking demand and cash-flow projections as counterweights.

Why NVIDIA Is Central To The Strategy

NVIDIA (NASDAQ:NVDA) is the infrastructure half of Karp’s pitch. In Q1 fiscal 2027, NVIDIA reported revenue of $81.6 billion, up 85.2% year over year, with non-GAAP EPS of $1.87. Data Center revenue was $75.25 billion, up 92%, and the company guided Q2 revenue to $91.0 billion plus or minus 2%. CEO Jensen Huang said “Agentic AI has arrived, doing productive work, generating real value and scaling rapidly across companies and industries.”

NVDA trades at $196.24, up 7.42% year to date and 26.81% over the past year. The Palantir tie-up gives NVIDIA a direct route into regulated enterprise and government workloads where customers want to run models on their own ontology rather than through a third-party API.

What To Watch Next

Karp’s criticism of OpenAI and Anthropic reflects his view of how enterprise AI should be deployed. For investors, the key metrics to watch are whether Palantir’s $4.92 billion U.S. commercial remaining deal value continues to grow, whether NVIDIA’s Data Center business can sustain growth near 90% as hyperscaler AI spending matures, and whether the companies’ joint AI platform begins driving meaningful customer wins.

If Karp’s vision of enterprises owning the AI “means of production” is resonating with commercial buyers, it will likely show up in commercial TCV, deal count, and customer adoption through 2026.

Contact [email protected] for any questions or corrections.