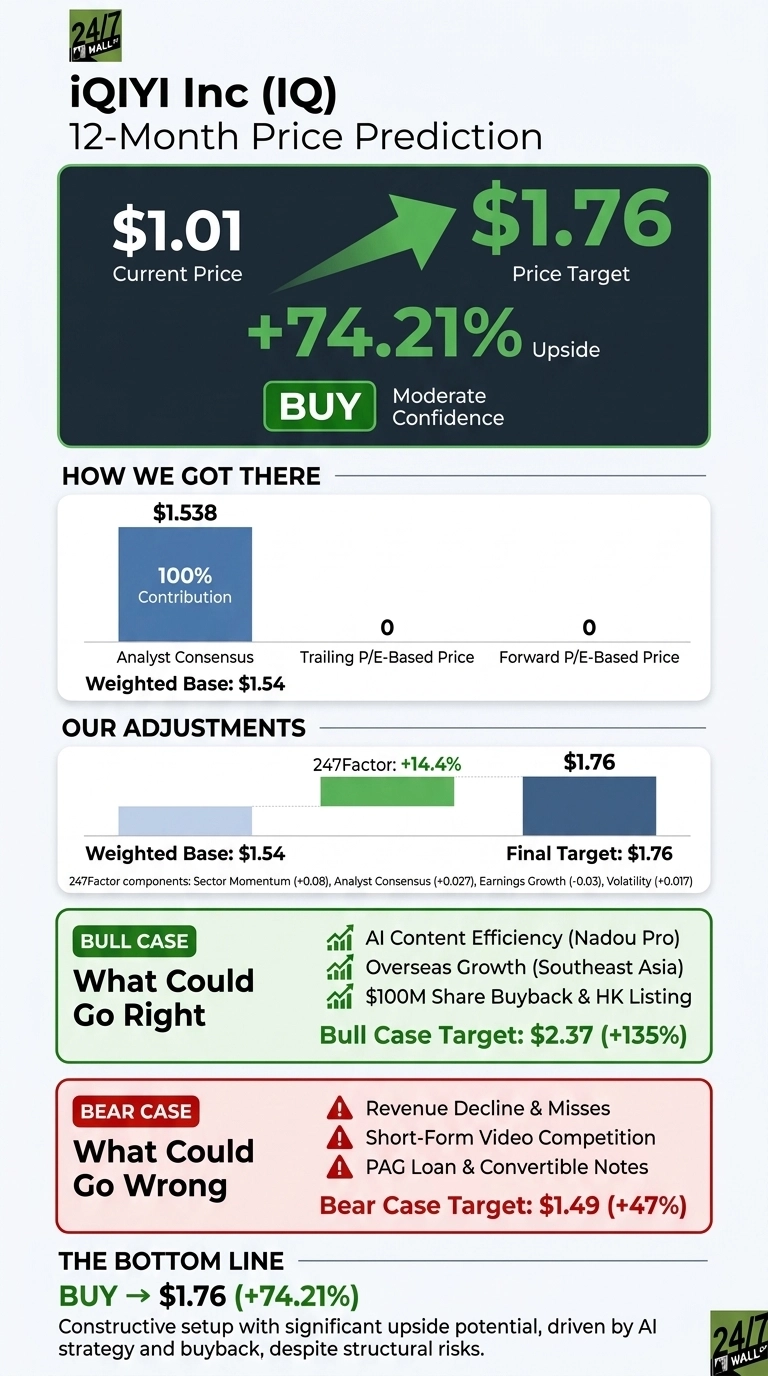

iQIYI’s (NASDAQ:IQ | IQ Price Prediction) NASDAQ-listed shares have been beaten down to penny-stock territory, but our proprietary model sees meaningful recovery potential over the next twelve months.

iQIYI trades at $1.01, down 47.4% year to date and 42.94% over the past year. Our 24/7 Wall St. price target for iQIYI is $1.76, implying 74.21% upside and a buy recommendation at moderate confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1.01 |

| 24/7 Wall St. Price Target | $1.76 |

| Upside | 74.21% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Stock That Has Lost the Room

iQIYI peaked near $2.57 in September 2025 and has slid to a 52-week low close to $0.95.

Q1 2026, filed May 18, 2026, missed on the top line with revenue of $913.32 million, down 13.37% YoY, while EPS of -$0.0352 beat estimates by 83.81%. Membership Services fell 5% and Content Distribution plunged 43%. Offsetting the gloom, iQIYI announced a proposed Hong Kong Stock Exchange listing and a $100 million buyback running through September 2027.

Why Bulls See a Breakout Ahead

The bull thesis rests on iQIYI’s AI pivot. Nadou Pro, the company’s AI production platform, surpassed 10,000 registered creators within one month of commercial launch and is now supporting 100+ iQIYI original productions, with the “None Shall Escape” project showing a 50% improvement in shot production efficiency. Overseas, Southeast Asia membership revenue is growing 40%+ annually, and a Viu bundle deal targets H2 2026.

CEO Yu Gong said the team is “leveraging AI to reduce content production costs, accelerate production cycles, and expand our content ecosystem.”

Across 23 analysts, the consensus is 12 Buys, 10 Holds, 1 Sell, with targets ranging up to $2.44. Our bull-case scenario reaches $2.37, a 135% total return, if AI efficiency gains translate into 2027 GAAP profitability.

What Could Go Wrong

The bear case is grounded in structural decline. Full-year 2025 revenue fell 6.62% and operating income collapsed 87.34%. Morningstar cut its valuation 50% to $0.50, citing user migration to short-form platforms like Douyin and Bilibili and rising content costs.

Benchmark kept a Hold, arguing the AI shift lacks a clear sustainable growth inflection. PAG loan exposure of $636.6 million and convertible notes remain overhangs.

That said, bulls would argue Q1 SG&A was cut 20% to $119.78 million and Q1 free cash flow of $16.10 million was positive despite the revenue miss. Our bear-case still lands at $1.49, a 47.38% return, reflecting the low absolute share price and buyback floor.

The Setup: Constructive, With Eyes Open

The 24/7 Wall St. price target of $1.76 supports a buy at moderate confidence. The decisive factor: even the bear-case scenario projects positive returns, thanks to a depressed starting price, a $100 million buyback, and a Hong Kong listing optionality.

The bull thesis strengthens if Q2 2026 confirms membership stabilization and AI-driven cost reductions widen gross margins back toward 25%. The thesis weakens if Membership Services declines accelerate beyond 10% or if convertible note refinancing terms harden.

Looking further ahead, here is where our model projects iQIYI could trade in the coming years, assuming current trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1.34 |

| 2027 | $2.13 |

| 2028 | $2.95 |

| 2029 | $3.66 |

| 2030 | $4.28 |

These projections assume iQIYI executes on its AI content strategy and reaches GAAP profitability by 2027. Significant upside could come from Nadou Pro monetization, while downside risk centers on China advertising weakness and short-form competition.

Contact [email protected] for any questions or corrections.