Apple (NASDAQ:AAPL | AAPL Price Prediction) just hit a fresh all-time high, and the question on every shareholder’s mind is whether the run has legs into year-end. Our model says yes, with some moderation.

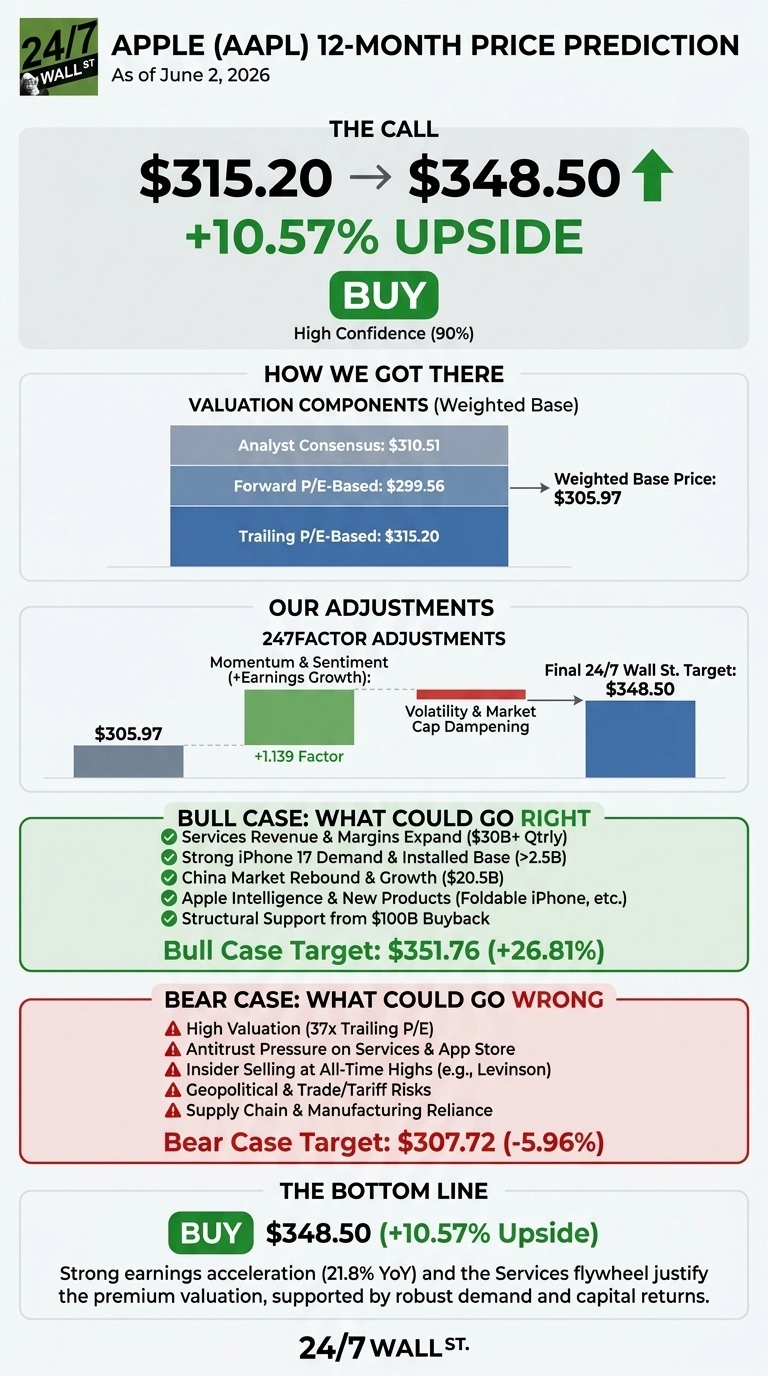

The stock closed at $315.20 on June 2, 2026, up 2.9% on the day and 16.16% year to date. Our 24/7 Wall St. price target for Apple is $348.50, implying 10.57% upside over the next 12 months. Our model assigns Apple a buy rating with high conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $315.20 |

| 24/7 Wall St. Price Target | $348.50 |

| Upside | 10.57% |

| Recommendation | BUY |

| Confidence Level | 90% |

How Apple Got Back to Record Territory

Apple has rallied 56.89% over the past year and 12.62% in the past month alone, brushing right up against its 52-week high of $315.45. The driver: a phenomenal Q2 FY26 earnings report. Revenue hit $111.18 billion, up 16.6% year over year, and EPS of $2.01 beat the $1.94 consensus, marking 8 consecutive quarters of beats.

iPhone revenue set a March quarter record at $56.99 billion on iPhone 17 demand, Services hit an all-time high of $30.98 billion, and Greater China rebounded to $20.50 billion. The board raised the dividend 4% and authorized a fresh $100 billion buyback.

Why Bulls See a Breakout Above $350

Our bull case lands at $351.76, a 26.81% total return. The path is clear: Services is now a $30 billion-plus quarterly business with software-like margins, the installed base crossed 2.5 billion active devices, and Apple Intelligence is finally moving from feature to driver.

Polymarket traders assign a 96.1% probability to an iPhone 18 launch in 2026 and 84.5% odds on a foldable before 2027, both of which could re-rate the multiple. Q1 FY26 already showed China reaccelerating to $25.53 billion, a category killer for the bear thesis. Bulls also point to the $100 billion buyback as structural EPS support.

The Risks Worth Watching

The bear case takes Apple to $307.72, a 5.96% drawdown. At 37x trailing and 32x forward earnings, Apple is no longer cheap on any historical lens. Tariff exposure, antitrust pressure on Services, and manufacturing concentration remain real overhangs.

Insider activity has skewed heavily to selling, with director Arthur Levinson unloading 50,000 shares at $311.02 on May 27 and another 255,000 shares on May 6. That said, much of the Tim Cook and executive April activity coincided with routine RSU vesting settlements, so the signal is softer than the raw share count suggests. Analyst consensus of $310.51 sitting just below the current price also reflects valuation caution.

Apple Price Prediction 2026-2030

I’m sticking with the 24/7 Wall St. price target of $348.50 and a buy rating at 90% confidence. The tipping factor is the combination of accelerating earnings growth (21.8% YoY) and the Services flywheel, which justifies the premium multiple in a way it could not three years ago.

The thesis would strengthen if Apple Intelligence drives a Services growth re-acceleration above 15%. The thesis would weaken if the next earnings report shows iPhone deceleration or China weakness re-emerging.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $348.50 |

| 2027 | N/A |

| 2028 | N/A |

| 2029 | N/A |

| 2030 | $453.61 |

These projections assume Apple continues compounding Services revenue and successfully monetizes Apple Intelligence. A breakthrough foldable or new product category could push the 2030 figure toward our bull case of $567.26, while sustained regulatory pressure could pull it back toward the bear case of $322.33.

Contact [email protected] for any questions or corrections.